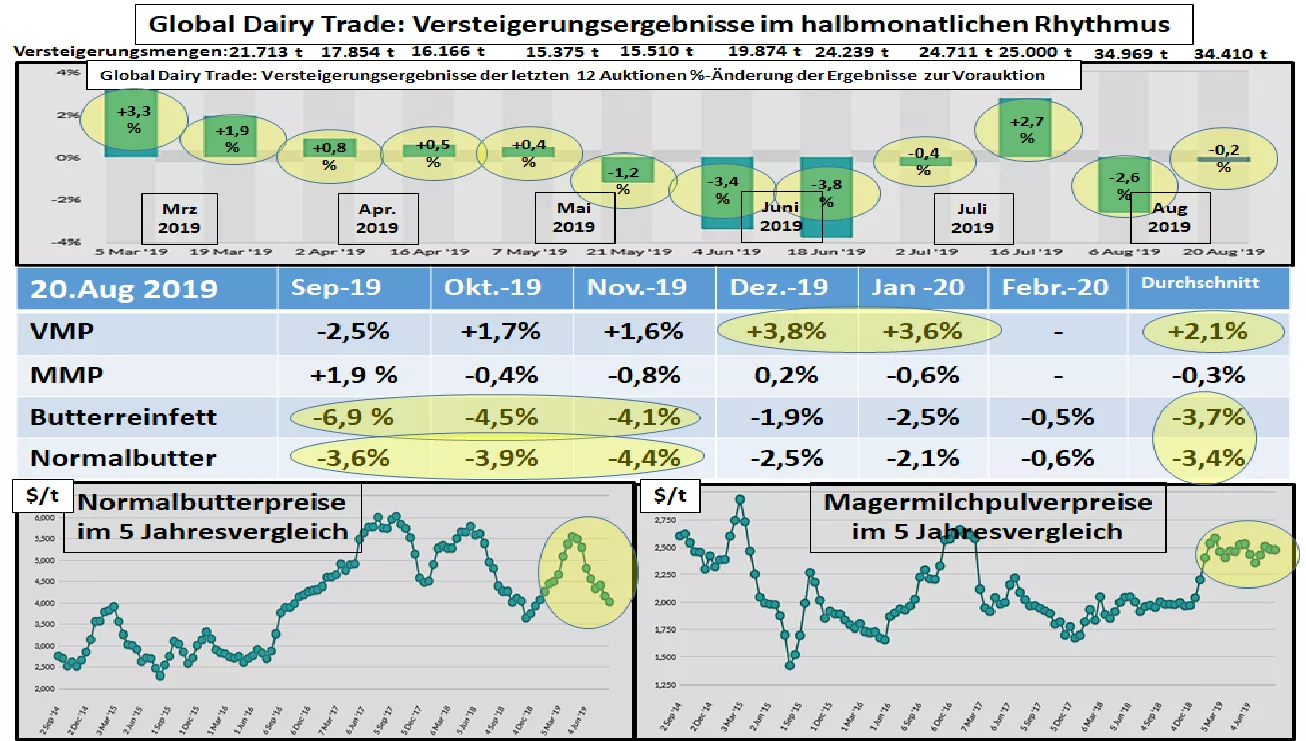

GDT Auction Results Aug 20, 2019: Average -0.2% The recent Aug-19 Auction of the Global Dairy Trade (GDT) has not yet made the decisive step out of the seasonal summer low with an average score of -0.2 , Revenue has meanwhile established itself again at an unusually high 34,410 t compared to the previous months. The results for the two butterfats are repeatedly weak, while whole milk powder offers a positive result. Whole milk powder (VMP) reached a clear increase of +2.1% on average in all delivery months for the first time. In particular, the back delivery dates Dec 19 and Jan 20 have risen sharply. New Zealand, as the main supplier for China, is currently at the low point of milk deliveries. Notable replenishment comes only in Sep.-19. In October, the highlight of the milk delivery is expected. Skimmed milk powder (MMP) can only once again keep the pre-auction result close at -0.3%.Outstanding is the Sept with an extra charge of +1.9%, with obvious pent-up demand had to be satisfied. The remaining delivery months were only just able to hold their own. The price fixing remains well above the EU intervention line consist butterfat has suffered price cuts averaging 3.7% for the second year in a row. In particular, the forward days Aug to Nov.19 caused with -6.9 to -4.2% for a hefty price reduction. The above-average price level of the past time can no longer be maintained. Nevertheless, the courses are still in the upper midfield. Normal butter also remains unusually weak in the front appointments with price discounts -4.4 to -3.6% to Vorauktion repeatedly. The early months have lost nearly 10% in value. The following months remain in negative territory. Nevertheless, the butter price is still in the upper midfield of the last 5 years. The auction results clearly indicate the end of a high price phase for the butterfats, while milk powder stabilizes with slight signs of recovery.Increased handling volumes are only absorbed by the market at lower prices. While milk deliveries in the northern hemisphere are declining significantly, New Zealand is headed for the seasonal peak. Overall, however, a decline in milk production can be observed in the major world exporting countries. That could speak for a closer market supply. China has a high import potential, but also a weakened purchasing power. Another price decline is unlikely.