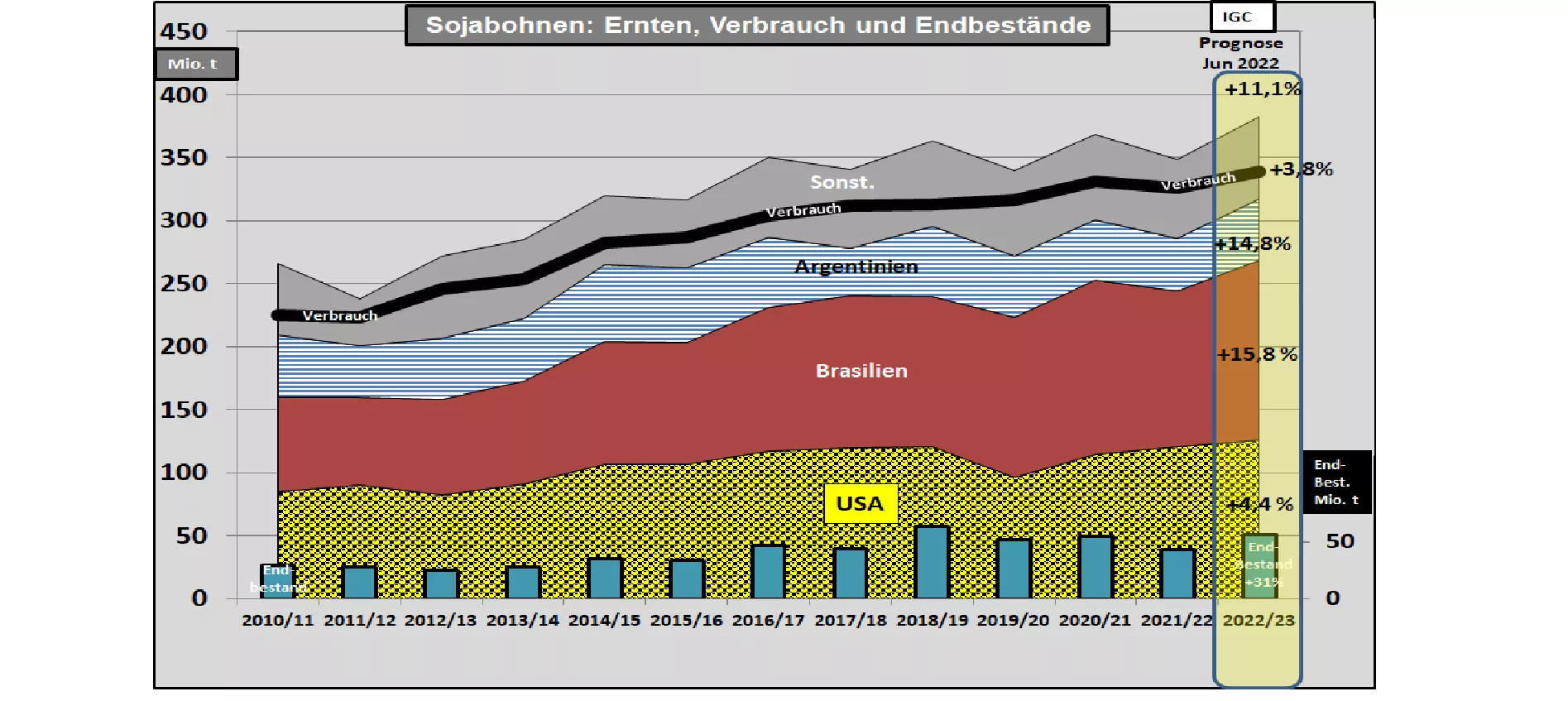

IGC estimates 2022/23 soybean harvest to be 11.1% higher In its June 2022 issue, the International Grains Council (IGC) estimated the global 2022/23 soybean harvest to be 11.1% higher at around 390 million tonnes compared to the previous year . Global consumption is also estimated to be higher at 376.5 million t . The ending stocks (EB) rise to 56.5 million t or 15% EB to consumption . In the previous year, the coverage figure was just under 12%. The supply figures without China are currently 9.4% ending stock to consumption (previous year 5.2%). On the production side, the increased harvests in Brazil (+17 million t), in the USA (+6 million t) and Argentina (+6 million t) are making a significant contribution to the increase in supply. In Paraquay , after last year's bad harvest of 4.3 million t, this year's result should end up at 10 million t .The South American harvests will not take place until spring 2023. In contrast, the Ukrainian harvest has been downgraded from last year's 3.4 to 2.8 million tons this year. On the demand side , China's imports dominate with 98 million t (previous year 92 million t). This corresponds to around 60% of world trade. Soy imports in the EU remain at 15 million tons . Despite China's increasing purchases, inventories have risen from 43 million t to an arithmetical 56.5 million t. For Brazil , the IGC estimates that ending stocks will double to 6.0 million t. For the 3 largest exporters , ending stocks are back to where they were two years ago. Measured against the outstanding harvest risks, the reserves are still limited. Soybeans for May-2022 have fallen back to €560/t on the Chicago Stock Exchange .Only 495 €/t are traded for Nov 2022 . US soybean meal (48%RP) falls to the equivalent of € 415/t for Sep delivery. Soybean oil prices are heading in the same direction. German soybean meal (44/5) for August delivery is quoted at €495/t on the Hamburg Stock Exchange.