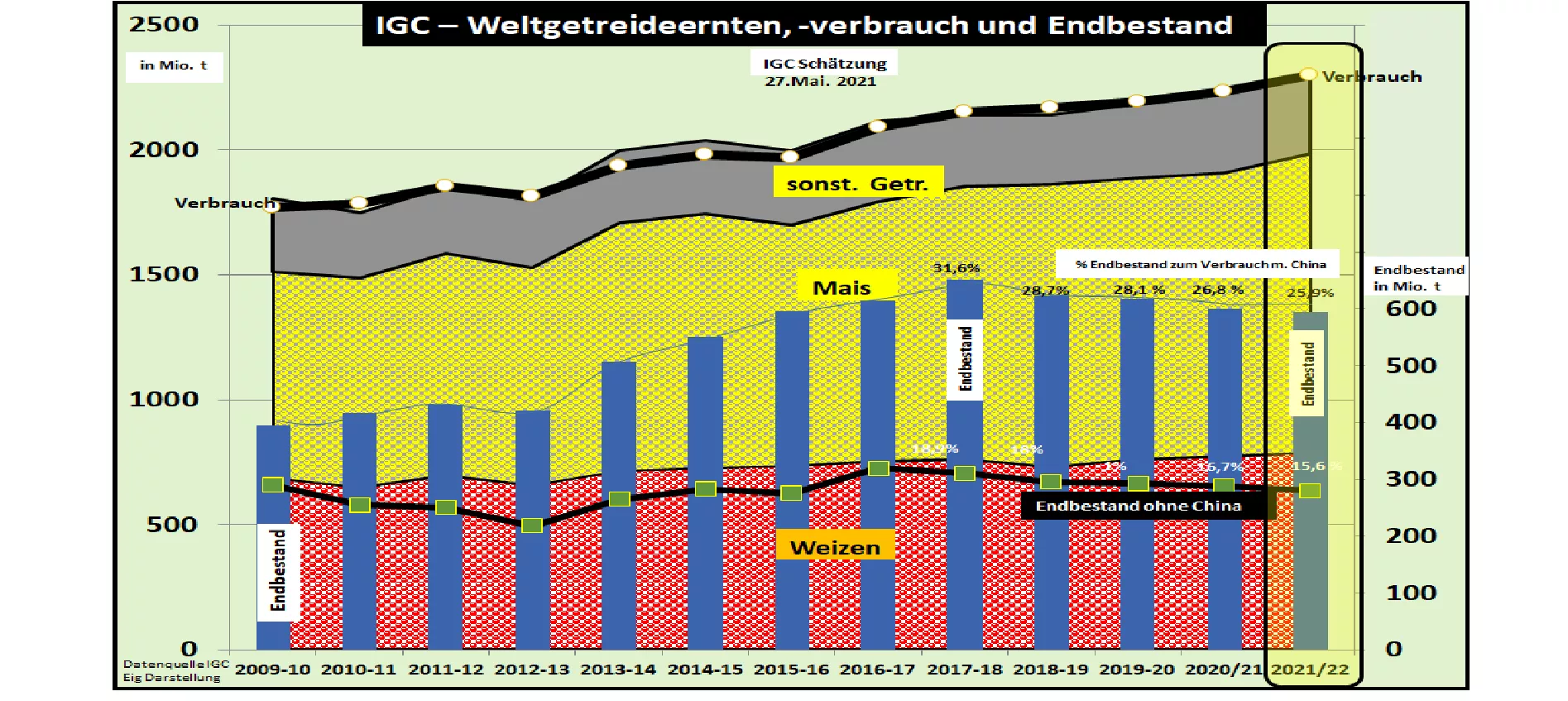

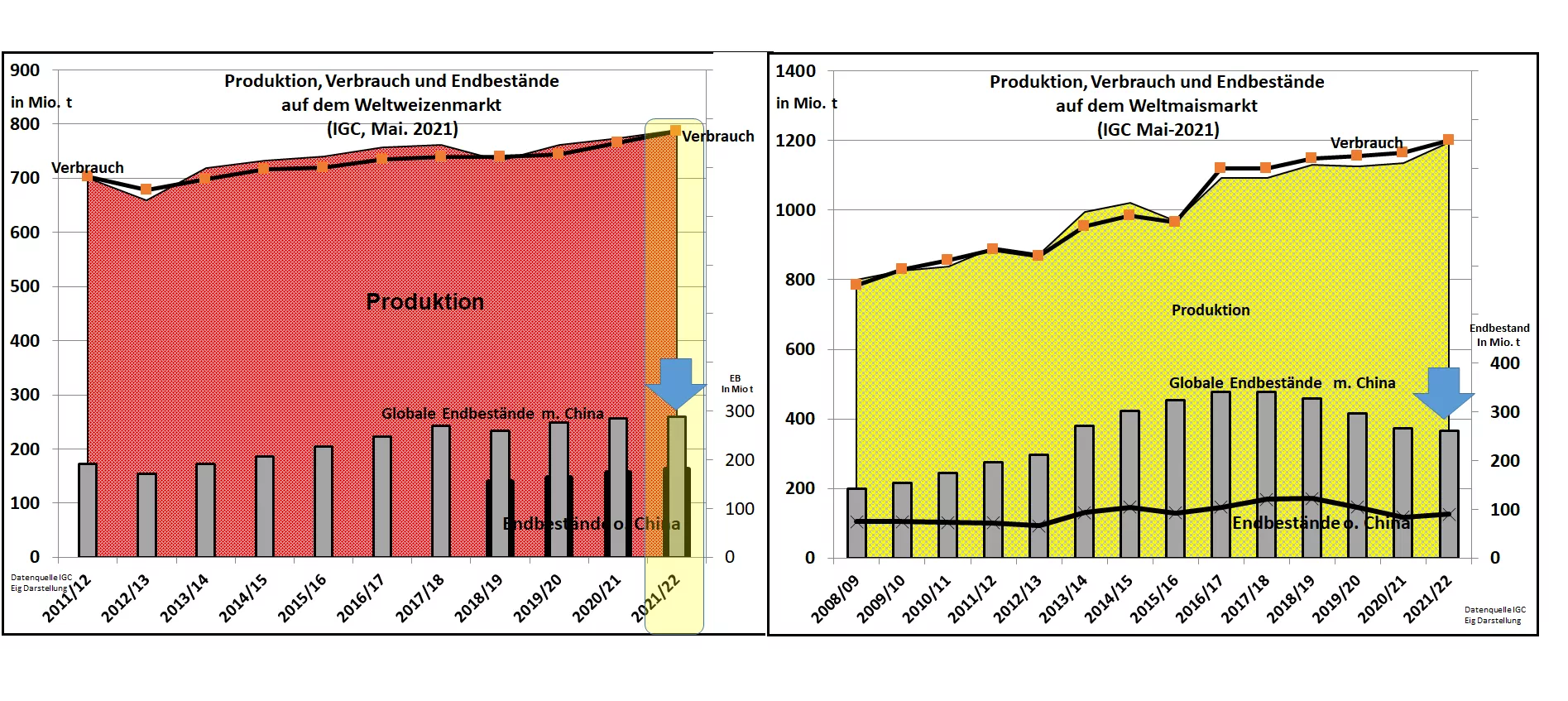

IGC May 2021: World grain harvest 2021/22 up 3.2% on the previous year - supply remains tight In its May 2021 edition, the International Grain Council (IGC) estimates the global grain harvest to increase slightly compared to the previous month to 2,292 million t or 3, 2% higher compared to the previous year. Consumption is estimated to be 2.7% higher to 2,297 million t . This means that the overhang stocks continue to decline to 595 million t. The supply figure falls for the fifth time in a row to 25.9% of the final level of consumption, but remains at the good average of recent years. In the wheat sector , a record harvest of 790 million t or +2.1% compared to the previous year is still forecast. Consumption is estimated at 787 million t in the previous year (766 million t), however, higher than in April. This results in an insignificant inventory build-up from 285 to 288 million t.The supply figure is calculated on a slightly reduced 36.5% final inventory for consumption. This means that the wheat market in and of itself remains relatively well supplied. The seed stands in the USA have improved significantly. In Russia, too, there is talk of well-average stocks. Despite outstanding risks in the grain formation and harvesting phase, the estimates are stabilizing. The soaring price of wheat on the stock exchanges is over. The Paris prices drop significantly towards 200 € / t. The IGC estimates the global corn harvest at 1,194 million t or +5.3 % higher than in the previous year. The US, the world's largest producer and exporter of corn, has made rapid progress this year after initial difficulties. On the other hand, there are considerable cuts to be made in the Brazilian second corn harvest. Global consumption is expected to increase by 3% over the previous year to 1,200 million t. Chinese imports in particular contribute to this. The inventories are in the course of the maize marketing year 2021/22 by approx. 6 milliont will be reduced to 261 million t . The supply figure drops by 1 percentage point to a low 21.8% final inventory for consumption. 4 years ago, the excess stocks were up to 30% based on consumption. Overall , it can be stated that despite the forecast increases in production, no fundamental improvement in the supply situation is foreseen. The background to this is increasing consumption. Above all, the unusually strong increase in imports from China plays a decisive role here. The scarce supply in the corn sector has rubbed off on the well-supplied wheat market. The above-average corn prices due to the scarcity also keep wheat prices at a high level, because inexpensive wheat replaces the missing corn in the feed sector.