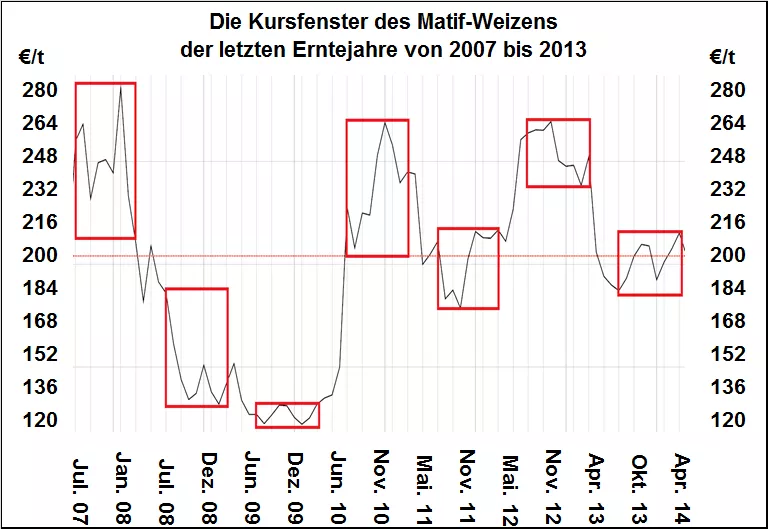

except in years with strong price changes the courses such as the following price window is moving after the harvest of August until April Max to 20 to 30 Euro / t the big price jumps are always in the period may to July instead. So, now applies to watch's.

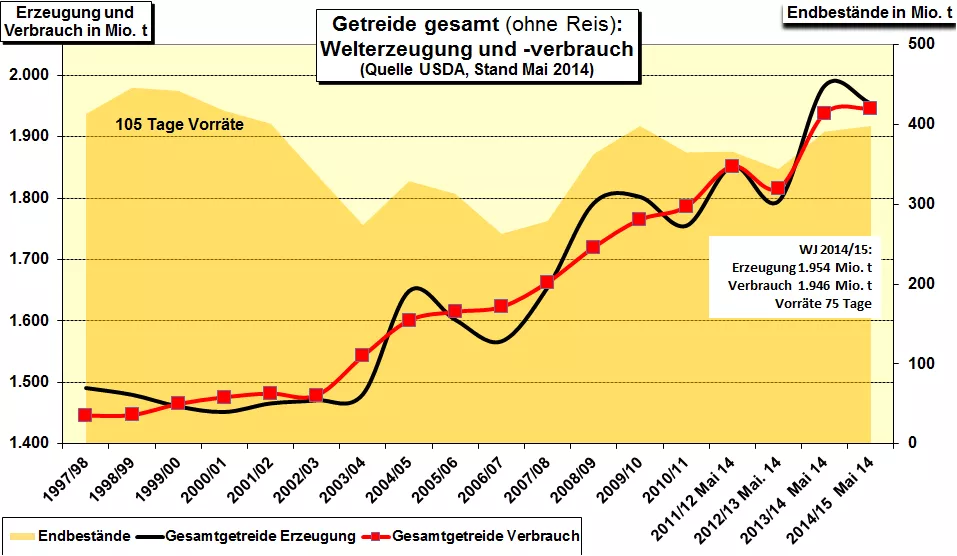

the first USDA report last Friday with the numbers of the WJ 2014/15, the figures of the WJ corrected 2013/14. Therefore the Getreideendbestände rise in the WJ 2013/14 to 47 million tons, for the WJ 2014/15 of closing stock increased by 7 million tonnes is expected to increase at this initial estimate. Thus the final stocks regain the relatively high level of the WJ 2009/10 and what happened with the prices is us still bad memory. There would have to think the crisis in the Ukraine and the still very uncertain earnings forecasts in the US corn more insurance subsets. Important: In case of barley to the world crop to 12.6 million tonnes to 132.5 million tonnes (VJ: 145.1 million tonnes) sink, of which 4 million tons of less in the EU (55.6 instead of 59.6 million tonnes). Consumption only by 3 million tons to fall, shrink inventories to a quarter. This prediction is true, will be a sought-after product on the world market German barley.

also in the oilseeds there in terms of the current USDA estimate and the significant inventory build-up - all over the world, plus 15 million tonnes to 95 million tonnes in the marketing year 2014/15 - in the moment no good arguments for a trend reversal. It is expected that the spending spree of speculators in Chicago wears off and continue the courses under pressure.