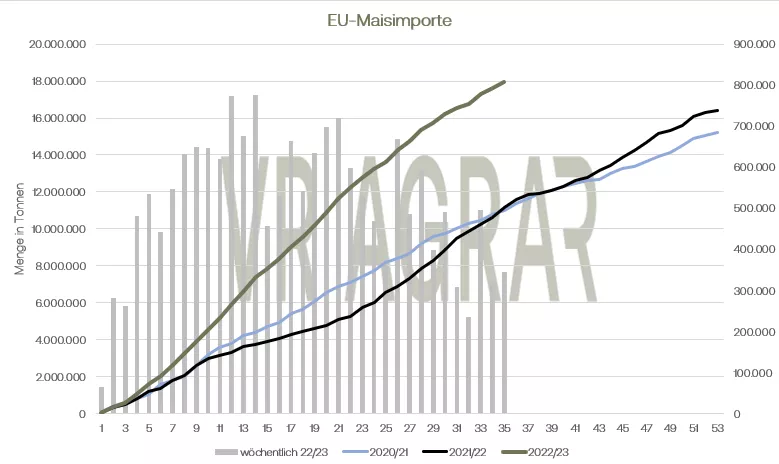

The grain markets went south again yesterday, Thursday, but there is a plus on a weekly basis. The May date on the Euronext/Matif closed yesterday with a closing price of EUR 268.50 per tonne. Last Thursday, 263.50 euros were still on the scoreboard at the closing bell. In the same period, corn improved by EUR 4 per tonne to EUR 264.00 per ton closing price on Thursday. The extension of the grain agreement for Ukraine had already been priced in by the market. After the extension became known for the time being, prices in Paris and Chicago recovered slightly. The agreement has not yet been signed. But the main issue is whether the agreement will be extended by 60 days or 120 days. Ukraine, Turkey and the United Nations want to achieve this period of time, but Russia still insists on the 60-day deadline. Almost no one believes that the agreement could still fail. In Europe, export demand continued to calm down. While a median of 592,637 tons of common wheat was shipped per week on average for all weeks of this marketing year, the reports for the last three weeks were significantly lower. In the last week 208.475 tons, of which 226,3126 tons were sold for export during the week. The total counter currently stands at 21.54 million tons compared to 19.84 million tons at the same time last year. France remains Europe's largest supplier, followed by Romania and Germany. France's Ministry of Agriculture left its forecast for soft wheat exports outside the EU at 10.45 million tons. However, the ministry expects fewer exports to EU countries, since the suppliers are confronted with cheap offers from Germany and the Netherlands. If the forecast is correct, that would be an increase of 19 percent compared to the previous year. The German Raiffeisen Association made its first assessment of the new grain and rapeseed harvest this week. According to the association's analysis, the total grain harvest is said to be 42.67 million tons, around 1.8 percent less than in the previous year. The area under cultivation has fallen from 6.09 million hectares to 5.95 million hectares. Significant declines can be felt in durum wheat and spring wheat in particular. The area reduction for winter wheat is 1.9 percent. However, despite an increase in winter barley acreage, barley also recorded an overall decline in acreage.According to DRV estimates, the total wheat harvest next summer will be 222.01 million tons, 2.3 percent less than in 2022. The German Raiffeisen Association attributes the decline in area to, among other things, higher areas under cultivation for rapeseed and silo maize, but also to stronger competition for land from PV systems and settlement construction. Grain corn is to be cultivated on an area of 4.06 million hectares and bring a harvest of 3.84 million tons. The area under cultivation here is 11 percent, the harvest volume would be around the same as last year, according to the DRV. Wheat was also up on the CBoT this week. Export sales were better this week than in previous weeks. In addition, poor assessments of the condition of winter crops support prices from below. Turbulence on the American financial markets only had a short-term effect on the grain markets. In the case of corn in particular, market participants are still looking at the situation in Argentina, in addition to the extension of the grain agreement. The production forecasts are repeatedly corrected downwards. Most recently, the Buenos Aires Grains Exchange revised its forecast by a further 1.5 million yesterday.Tons adjusted down to 36 million tons. That would be the smallest harvest since the 2000/2001 marketing year. Local precipitation of up to 100 mm has been announced for the coming week, but a lasting relaxation is not expected. American exporters are currently placing large quantities in China. For three days in a row, the USDA reported large individual deals with buyers in China. Market participants expect further sales to China in the coming days. There is little news on the local cash markets. Bread grain is currently still only being traded in manageable quantities due to subdued demand for flour. Buyers and sellers are also usually far apart in terms of price.

ZMP Live Expert Opinion

The extension of the grain agreement is not yet in the dry cloths. But hardly anyone expects failure. The EU's export momentum has slowed and competition from Russia remains. Neither the price development of the past few days nor the consideration of all fundamental factors currently indicate a very clear direction.