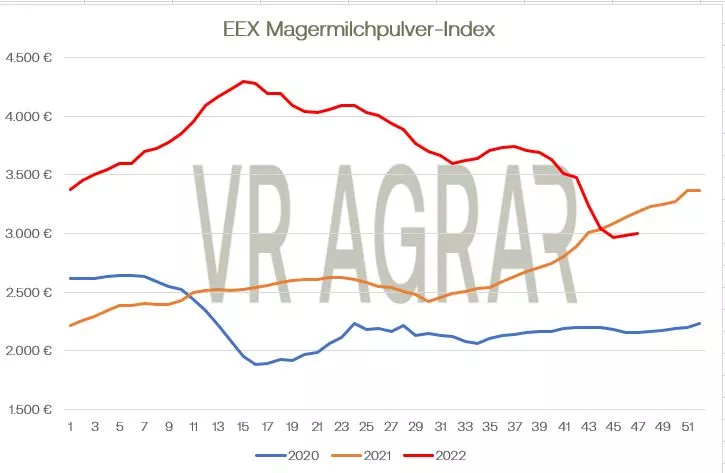

Although a little less raw milk was delivered in the last full week of November than in the previous week, the previous year's line is again clearly exceeded. Compared to the last week of November 2021, 3.1 percent more raw milk was collected from the dairies. The total annual backlog has thus reduced to 0.5 percent. Spot market milk has recently given way very significantly. For the current week, the ife Institute in Kiel determined a spot market price of 52.3 cents/kg (-3.6 cents/kg) as a national average. A similarly strong decline can also be seen in the Netherlands, while the price declines in Italy are more moderate. Both industrial cream and skimmed milk concentrate have recently given way over the course of the week. The processors have already completed most of the Christmas production and the increasing milk volume means that more raw materials are available, which puts pressure on prices. The butter market continues to be divided. Molded butter is also in high demand in the food retail sector from the beginning of December. The calls by the food retailer from the manufacturers are still quite extensive. The price quotations in Kempten remain unchanged due to the contract.Consumer prices have also remained unchanged for several months at EUR 2.29 for the 250 gram pack. The block butter traders, on the other hand, are hesitant. Buyers are still reluctant to buy large amounts of goods and are waiting for prices to continue to fall. At the same time, however, the manufacturers are less willing to respond to the falling price demands of the buyers. The production costs are still high and have recently risen again slightly, which is why there is hardly any trading and supply on the part of the suppliers. In terms of exports, trade in block butter is still very sporadic. Yesterday, the butter and cheese exchange in Kempten reduced its listing at the top end by 31 cents per kilogram, at the bottom end there were 23 cents less on the trading slip. Contract prices also fell significantly on the EEX. Trading activities on the Kempten stock exchange have picked up again recently. International butter prices have also fallen. In the Global Dairy Trade Tender in New Zealand, butter lost 1.9% compared to the last auction. Cheese prices are also under pressure.In Hanover, the trading margins and average quotations for Gouda were significantly reduced for both block and bread products. The calls by the food retail trade have recently been somewhat weaker. Nevertheless, there are higher call-off quantities than at the beginning of November. Bulk consumers and industry called off their goods to the usual seasonal extent, but are waiting for new contracts to be concluded. Occasionally there are also inquiries from exports again, the declining prices make this possible. The ripening warehouses are full on average, but the cheese products are still tending to be delivered young. Cheddar was priced higher in New Zealand's Global Dairy Trade Tender on Tuesday, gaining 1.8%. Food- grade skimmed milk powder is still available in sufficient quantities. As a result of the increased volume of milk, the factories are also increasingly producing butter and skimmed milk powder. The weak price trends continued this week. Demand is lacking momentum, business transactions are limited to a few volumes for the first quarter of 2023.Internationally, however, skimmed milk powder was able to increase again in the Global Dairy Trade Tender. The dairies concentrate on the processing of existing contracts in the production of whole milk powder. Here, too, demand is calm and lacking in impetus, but isolated inquiries and orders from third countries were received by German manufacturers. Nevertheless, EU goods are still very limited competitive. The butter and cheese exchange in Kempten also lowered the price for whole milk powder yesterday. The quotations for whey powder are declining. Feed grades are now more in demand again, but food-grade whey powder is more than sufficiently available. At the same time, demand is relatively low.

ZMP Live Expert Opinion

The pressure on the submarkets remains. The market as a whole expects prices to continue falling, which is why buyers are likely to exercise restraint beyond the turn of the year.