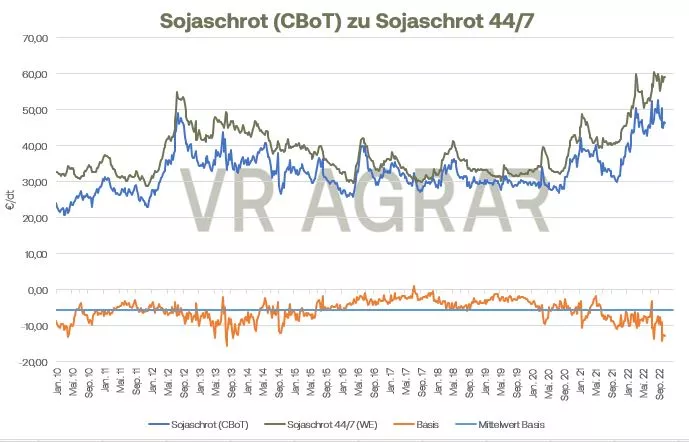

The past week was characterized by the news situation about agricultural exports from Ukraine, especially in the case of rapeseed. After Russia withdrew from the grain agreement last Saturday, rapeseed and other vegetable oils went up sharply. Moscow then backtracked on Wednesday after Ukraine pledged not to use the secure corridor for military purposes. This in turn led to declining prices. On a weekly basis, however, rapeseed increased in Paris. The new front month of February closed last Friday at a closing price of EUR 637/t. Yesterday, Thursday, the settlement was EUR 660.00/t, a weekly gain of EUR 23 per tonne. The May date on the Euronext/Maitf is also firmer and is above the EUR 650 per ton mark, the August contract for 2023 was below this mark yesterday at EUR 648.50. The International Grains Council (IGC) expects an even higher rapeseed harvest compared to its previous forecast. On Thursday, the panel of experts in London raised the forecast by 2.2 million tons to 84.5 million tons. If the forecast is correct, last year's harvest would be exceeded by 15.6 percent and 11.5 million tons more rapeseed would be harvested.The harvest forecasts for Russia and Europe in particular were raised. For the EU, the committee expects a harvest of 19.3 million tons. The EU Commission last estimated the rapeseed harvest at the end of October at 19.5 million tons. Only a small amount of rapeseed is traded on the spot markets. But as a result of the higher stock market prices, prices for rapeseed also rose accordingly. Franko Ölmühle Hamburg is currently quoted at 652 euros/t, in Straubingen it is 647.00 euros/t and thus 20 euros more than a week ago. The rapeseed meal prices are inconsistent. According to a report by the Canadian Grains Commission, the North American country exported 201,400 tons of canola in September. The main destinations are Mexico and China. Looking at the season as a whole, exports are currently 41 percent behind last year's figure. Even if the momentum has slowed down a little, high rapeseed imports are still evident in the EU-27. Until 30.10. 2.28 million tons of rapeseed will be imported in the current marketing year, compared to 1.70 million tons at the same time last year at the end of October. Imports of rapeseed meal and rapeseed oil, like soybean meal and soybean meal, are slightly below the levels of the previous year.Despite the sometimes significant losses on Thursday, soybeans on the CBoT were able to gain on a weekly basis. The most traded January contract closed yesterday at a closing price of 1,437.00 US cents/bu, which corresponds to a converted price of 541.60 euros per ton. Soybean meal also increased significantly on a weekly basis. The December contract on the CBoT closed yesterday at US$ 424.50/short ton (EUR 478.97/t). From the middle of the week in particular, trading trends in oilseed become more volatile. The news situation can be described as thoroughly mixed. For one thing, growing conditions in Argentina are bleak. The country continues to be plagued by a drought. The soy processing figures have also risen, in September 2022 around 2.9 percent of the beans were processed in the USA compared to September 2021. However, declining export bookings in the USA and the US dollar, which has strengthened again, cloud the picture. According to various reports, Brazilian farmers are currently making good progress in cultivating their acreage, and the US soybean harvest is also going well and will continue to run at high speed for the time being due to favorable weather conditions. In Germany, soybean meal prices on the spot markets increased significantly on a weekly basis.The current exchange rate against the US dollar tends to make exports more expensive.

ZMP Live Expert Opinion

The oilseed markets have lost none of their volatility. On a weekly basis, both soya and rapeseed have increased significantly. The general geoplotic situation is supportive, the better supply situation with rapeseed and the prospect of a record harvest in Brazil are depressing on the other hand.