Oilseeds in the background of the cereal price rally - still not entirely uninvolved

The strong price increases for wheat was in the middle of the focus of agricultural exchanges. Russia's future export policy fully took the attention of the brokers claim. After the first excitement, the first backlash will return again. The effect of Russia is so great but again not to not by other exporting countries this year to compensate to be brought back.

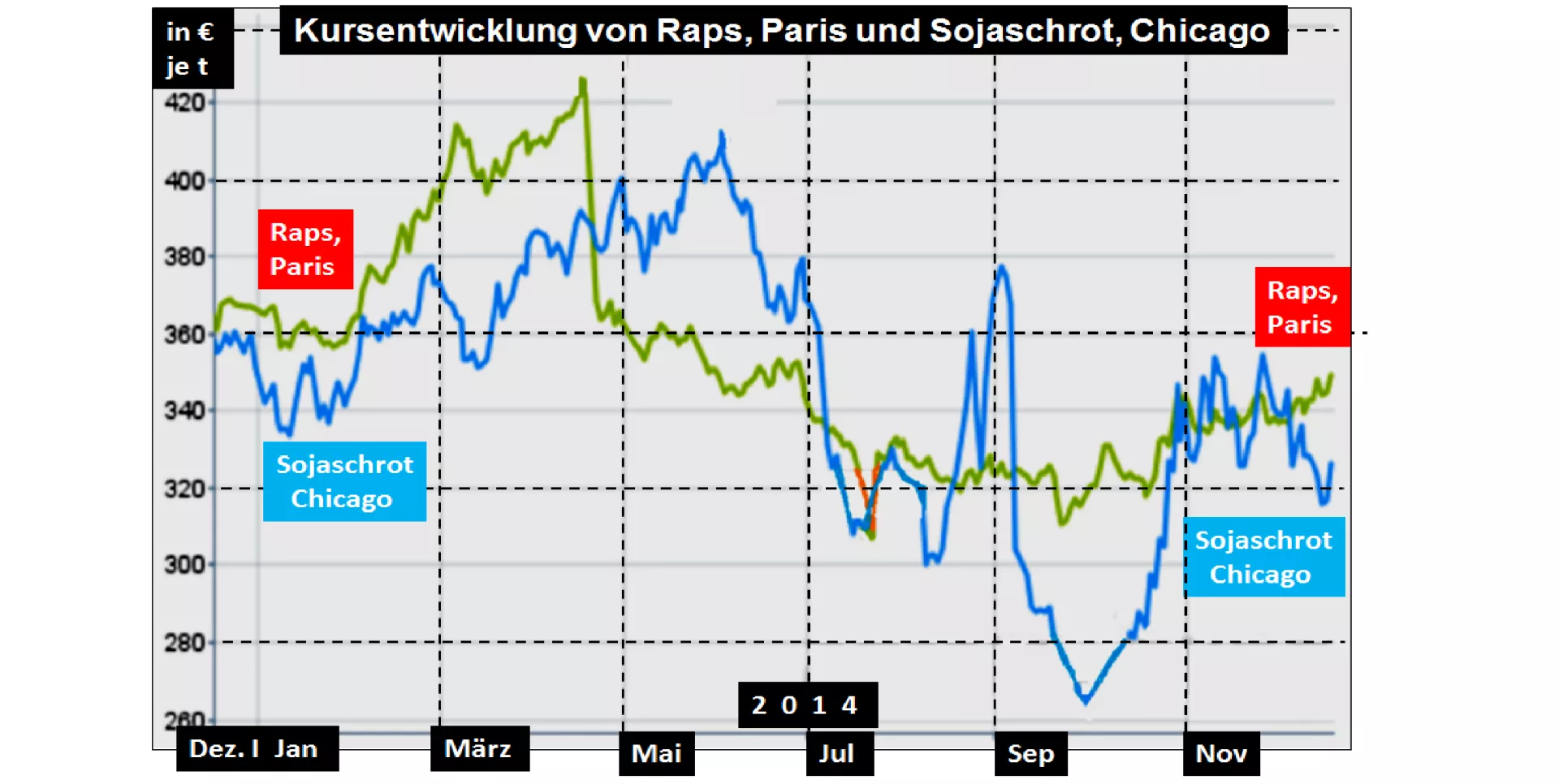

The courses for the oilseed rape and soya stood in the background, if not quite on the sidelines. The rape rates did well on the Paris stock exchange despite weak specifications from Chicago on a level of €340 per t. The low palm oil prices as a result of the decline in crude oil have to develop not the full effect of a price reduction. The expectation of a tight supply situation could stand behind it in the coming year. Applies to mills, in time to back up the raw materials in the own country.

Rising grain prices but also regularly develop an traction effect on oilseeds, finally, they are also a food supplier to a lesser extent.

In the case of the soy complex produces an strong effect of pressure due to the record soy crop in the United States, slowly but surely filling up the consumption channels for the umpteenth time. Logistical supply bottlenecks are more in the background.

Increasingly high expectations for a large crop of South America in the field of vision of the future pricing move. The Outlook for Brazil and Argentina are quite promising, though is wary of any rain break, whether and to what extent they justify sacrificing the high harvest expectations or not.

On the demand side is the approval of some types of GMO corn a certain role. The Chinese interest in DDGS (dried corn Stillage) seems to have grown. DDGS is perfectly able to replace on a noticeable scale soybean meal as protein carriers. Several estimates assume that China will hold back significantly in terms of soybean imports compared to the previous year.

The multiple accounts of soybean supply and demand promise rising end stocks at unprecedented scale. A build-up of inventories will push prices down. Einschlähgigen experience, the competition for the sale of soy, expected to reach a certain peak in the March 2015 at the latest.

The fundamentally established downward trend in soya prices is hard to stop. Possible interference from weather conditions and logistical difficulties such as dock workers strikes, etc. offer only temporary uncertainty.

ZMP Live Expert Opinion

She brought immediately rally the cereals market little movement to end for the oilseeds. Actually the fallen crude oil prices would need to make a greater impact. But oilseeds are to a certain extent to be considered as feed. May the up - and the output factors have neutralized largely himself.

For soybean meal price decline will prevail in the komemnden time increasingly due to the tangible becoming a global bumper harvest. In spite of Störfdaktoren such as weather and logistical problems involves rather the question, how far the price drop will fall if the supplied risk premia.