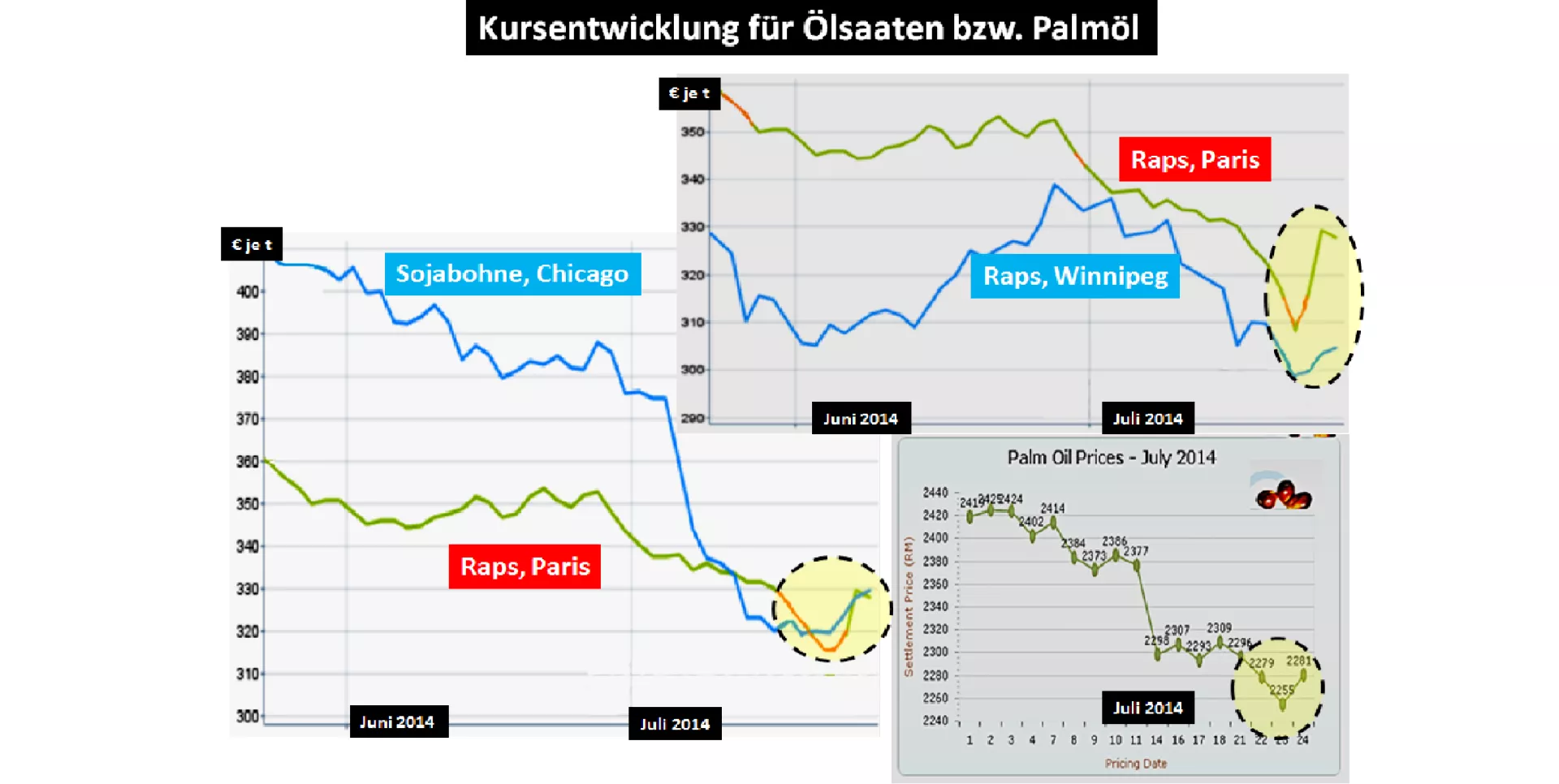

Rate turbulences in the quotes for rapeseed, soybean and palm oil - end a preliminary or final descent flight?

The off and on movements in the oilseed sector of the last 2 weeks raises the question, whether and to what extent the rate adjustments at the coming economic period of a plentiful supply situation in the oilseed sector are already achieved or substantially completed.

Trigger for the recovery were essentially the soy prices and palm oil prices. The still-scarce supply situation until the new harvest in the US soybean market ensures high sensitivity. Fears of less favourable weather in the United States during Blüh - and pod formation and high purchases for export have provided ample U.S. soy supply in question the expectation of an imminent. At least the front courses have knocked out violently to fall upwards, while the rear dates have shown moderate reactions.

The palm oil prices upwards again slightly longer. Background the serious impairment of the current production in the next few months, actually Oct reached its climax in the month should rainfall lack of as a result of the El Nino effect brakes already the generation. The storage warehouses are filled but still good, but not the high quantities of the year 2013 be reached.

A high rape harvesting doubts are expressed in Europe at some sites. Disappointment is spreading already in the UK, where the earnings expectations have not been met. Continued unfavorable harvest weather slows down even the Eurphorien of top income in other EU Member States. Deliveries for the EU import demand from the Ukrainian rape harvesting be considered with care. Engagement shows China for Ukrainian oilseeds.

Estimates of future demand for biodiesel to be mixed due to declining fuel consumption have raised for confusion, initially contributed to a drop in prices.

The high Canadian range from ancient harvest has capped the prices first. The current assessments of the Canadian harvest results significantly more fail in the face of the reduced acreage and less favourable weather.

the oilseed market is still in a transition phase scarce supply of aging Tiger goods and the expectation of bumper harvests in the coming months. Signs and notices on upcoming earnings and harvest risks keep the performance up to the harvest date in breath.

ZMP Live Expert Opinion

Is the orientation of the courses for oilseeds and torn between the still prevailing tight supply situation - especially in the United States - and the expected record harvests in the coming year Sept-Aug-2014 / 15 signs of earnings and harvest risks become an occasion for considerable fluctuations. it remains uncertain whether and to what extent already a soil formation is achieved. The later dates to the turn of the year provide more fragile than the current rates. The course expectations are bearish. But the unpredictable weather development in the central regions of production ensures sufficient uncertainties in fall 2014.