USDA Oct estimate to the oilseed market - above-average supply situation

The entire oilseed market is appreciated largely unchanged. There are no significant adjustments in production, consumption and final data. The supply situation is much higher than long-term averages.

The stock exchanges have reacted but on the estimation results in a wide range. The on and ranged downward - especially in the front October dates - from a Nettoplus to a net minus. The rear dates from Dec. 2014 the old is just stabilizing prices level again.

U.S. soybeans have fallen back on a broad front and have fully offset recovery since Oct. 14. This also applies to soybean oil. The strong upward drive for the Oct-delivery has prevailed in the case of soybean meal straight again. For the following dates the previous upward trend has been settled continuously again. As a reason, one can assume that October is achieved with the harvest month still no thorough coverage of supply.

The U.S. soybean crop was easy to nearly 107 million tonnes (previous year 91.4 Mio.t) corrected upwards. High exports and high domestic processing let fivefold the tight initial inventories far above-average 12 million tonnes.

Unchanged high soy crops the USDA for South America estimates. For Brazil it remains at 94 million tonnes, although in the countryside itself estimates between 90 and 98 million are in circulation. Also for Argentina is held at the 55 million tonnes, although voices are loud, that Argentine farmers increasingly rely on the soybean because cheaper fails in the face of high rates of inflation and of national bankruptcy the production of this fruit. Also the soy / corn price ratio in favour of the Sojaanabau. However, sowing in South America has started and have the weather development in recent times to be something desired.

China, with about two-thirds of world soybean trade the decisive factor on the demand side. This year's import is estimated at 74 million tonnes. The increase compared to the previous year is only half as large as in the previous year with an increase of 10 million tons. Sufficient inventories and a weaker economy slowing imports.

In the second leader in the oilseed complex palm oil it remains Malaysia and Indonesia in the previous assessment of a somewhat subdued increase in production due to the insufficient rainfall in the main production areas. Palm oil prices have again something rd. $650 t recovered, stay but far behind earlier values of $850 je u.m. back. In terms of production volume ranks palm oil ahead of soybean oil.

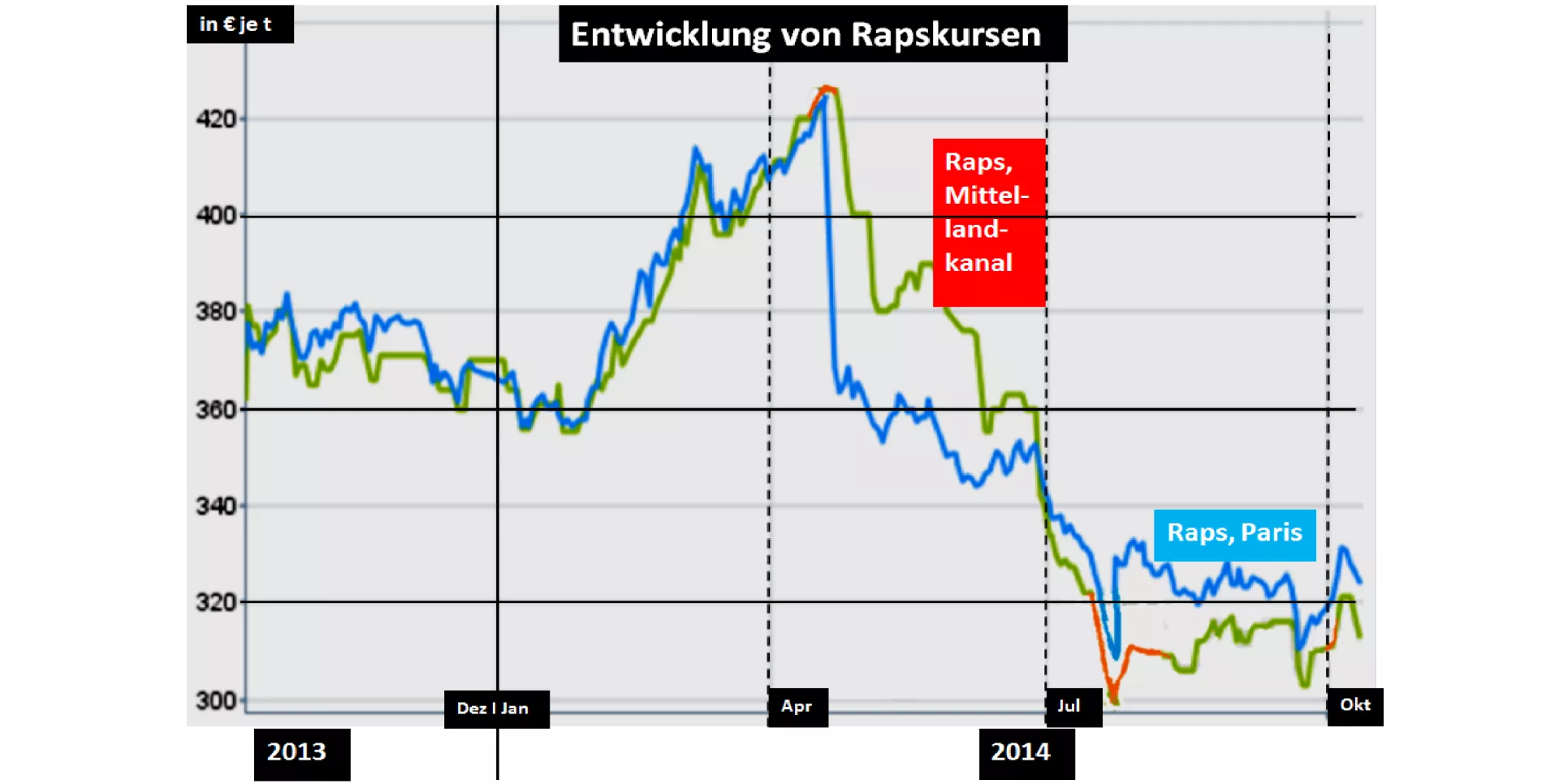

With approximately 70 million t takes rape accounted for rd a 13% of the global oilseed market. Regional other plays a role rape but with above-average 23.5 million tonnes and in Canada the European Union with weak 14, 7 million t. Rape rates based on Palm oil and soybean oil prices due to its strong Ölwert share. Both products provide the level where rape prices can move.

Traded on the Paris Stock Exchange will rape again at approximately €32 each dt. The courses have been exposed to strong fluctuations lately. The future rape price level is little promising given the supply situation in the global oilseed market.

ZMP Live Expert Opinion

The oilseed market 2014/15 is still unchanged overflowing according to recent estimates of the USDA. Well, high end stocks hedge the risk of unforeseen market failures. Nevertheless remains a not inconsiderable risk into the spring months 2015 into the South American soybean crop. The palm oil production run at average speed. There are sufficient stocks. The canola harvest went well in Europe, so that the import requirements can be significantly reduced. The weak Canadian canola crop changed the prices only insubstantial.

Palm oil and soy remain market leader. The price development emanating from these two products determine the global Olsaatenmarkt. The price level remains low and contains still downside potential.