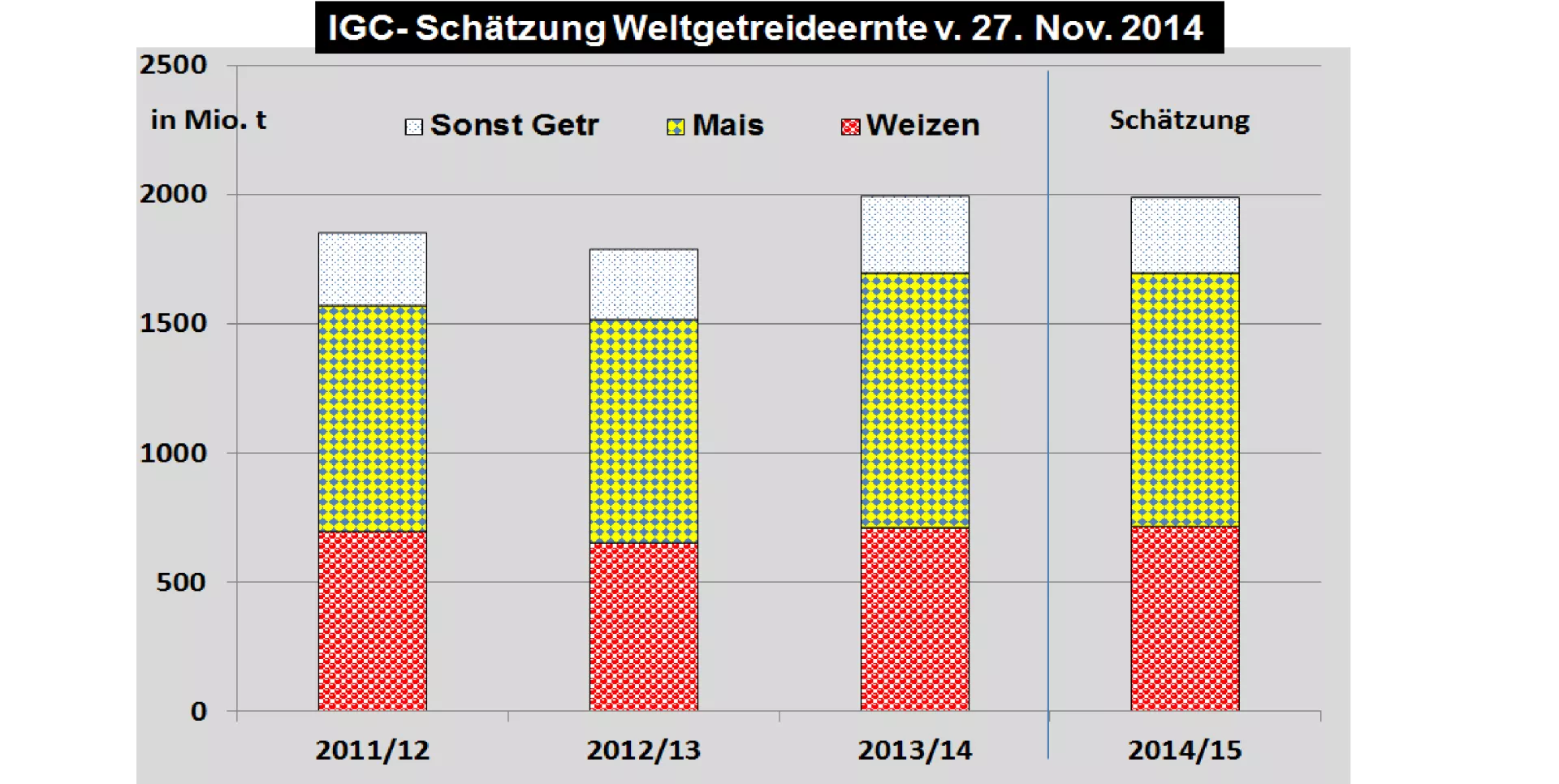

IGC-Nov-2014 market report estimated grain production and consumption slightly higher than in the previous month 2014/15 of the International Grains Council has set 2014/15 again the production and level of consumption in its most recent monthly estimates in the years upwards. The grain harvest at world level is now at 1.99 billion tons (previous year 1.994 billion t) classified.

Due to fallen prices of the IGC by higher goes consumption values in the magnitude of 1,965 billion tons (previous year 1,961 billion t) from. Rising consumption is expected in emerging markets.

The expected closing stock to around 26 million tons to 429 million t rise. In the leading export countries, the increase in stock is even less than 30 million tonnes. The IGC figures calculated from a stock to use ratio of 21.8%. The IGC typical average is 20.6%.

The wheat crop was 717 million. t cut. Poor harvests in Australia and Argentina have helped. On the demand side it is a rising consumption, so that the ratio of final inventory to consumption only 27% lands. The multi-year average can be quoted at 26.5%.

The global corn harvest was 982 million tonnes just below last year's level assessed. Weak harvests in China have been part compensated by good results in the United States. The prospects in South America remain uncertain. The supply situation at world level remains however above average with a stock to use ratio of 20.2%. The multi-annual mean less 3 percentage points.

On the exchanges, no movement in the exchange rates can be expected due to the US Thanksgiving . Even after the long weekend in the United States is expected to barely significant changes can be expected will be, because the new USDA report on Friday the 5th Dec. will wait.

Should the focus then the completed US corn - and soy crops are available. On the stock markets, but the first key figures from the new harvest back 2015/16 into the spotlight.

ZMP Live Expert Opinion

The supply numbers in the cereals sector are better than average. However, is the price level increased considerably in recent years. Obviously was per t wheat in Paris for the expected development of the supply too low the strongly fallen Nurslevel in September with nearly $150. On the other hand, you would expect no big flights of fancy. Because of the crops in the southern hemisphere with no improvement in the global supply situation is expected to be still considerable risks associated with the development of new crops by 2015. Some dark shadows seem to be already priced.