IGC estimates higher wheat and maize harvests.

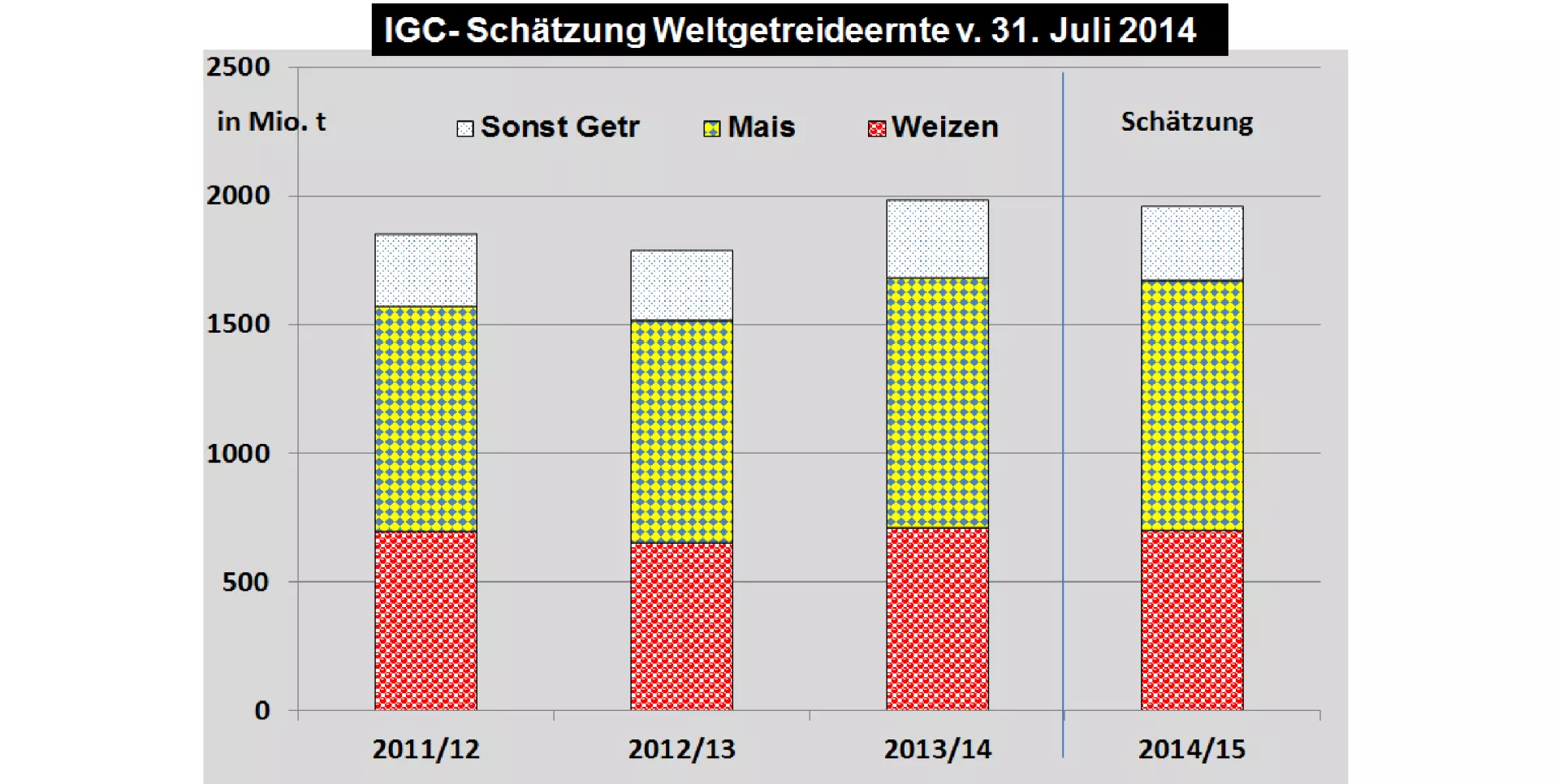

In the monthly July Edition, the International Grains Council (IGC) estimates the world grain harvest to approximately 1.959 million tonnes (previous year 1,982 million tonnes). The latest result is around 10 million tonnes higher compared to the previous month's estimate. Expected higher corn harvests in the United States are responsible.

The global wheat harvest prized the IGC now to 702 million tonnes (previous year 710 million t.) The higher classification is attributed primarily to better harvests in Russia and the Ukraine. The EU crop remains large, but with concerns about the quality. On the consumption side is assumed in the food sector by higher consumption in South Asia and Africa. In Europe, is expected to a stronger food consumption. The global supply situation in the wheat sector closing stock price can be calculated comfortable 27.6% for consumption. The multi-annual average is 26%.

The global corn harvest 2014/15 estimates the IGC at 969 million tonnes (previous year 974 million tonnes) a again to 6 million tonnes higher than in the previous month. The high US crop expectations are crucial. Despite smaller acreage, the prospects for high Flächenerträge in the American corn belt are favorable to compensate for the decline of areas for the most part. Corn consumption is expected to increase worldwide to 951 million tonnes (previous year 937 million tonnes). The final inventories grow to 187 million tonnes (previous year 169 million tonnes). An exceptionally favourable supply key figure of 19.7% can be calculate the consumption end stock. The multi-year average is about 16%.

The remaining "small" grains such as barley, rye, Triticale, oats, and sorghum are estimated around 10 million higher to nearly 290 million tonnes. It is expected a balanced supply / consumption balance.

The grain supply in 2014/15 provides a supply of 2.371 million tons with an initial population of 401 million tonnes plus a harvest of 1,956 million tonnes. A total consumption of 1941 Mt faces the, so that a rising closing stock of 419 million metric tons comes out. The supply ratio is calculated on average 21.6%. The multi-year average is located slightly above 20%.

The surplus stocks of the leading eight exporting countries improved from 122 to 137 million tons and offer a sufficient cushion for any additional need for importing countries.

Bottom line: The IGC with his most recent estimate underlines the above-average supply situation on the world grain market 2014/15.

ZMP Live Expert Opinion

Rather conservatively guessing International Grains Council (IGC) underlines the high expectations of an above-average global supply situation on the world grain market 2014/15 with his recent July issue. The wheat market cuts slightly less well off than the international corn market. The supply consumption accounting provides a distinctive building of inventories. Even unvorhergesehe risks could be sufficiently cushioned with this reserve stock. Production and harvest risks until spring 2015 are yet to be overcome. Under these perspectives are the prices are below the long-term averages. Variations are however cannot be ruled out.