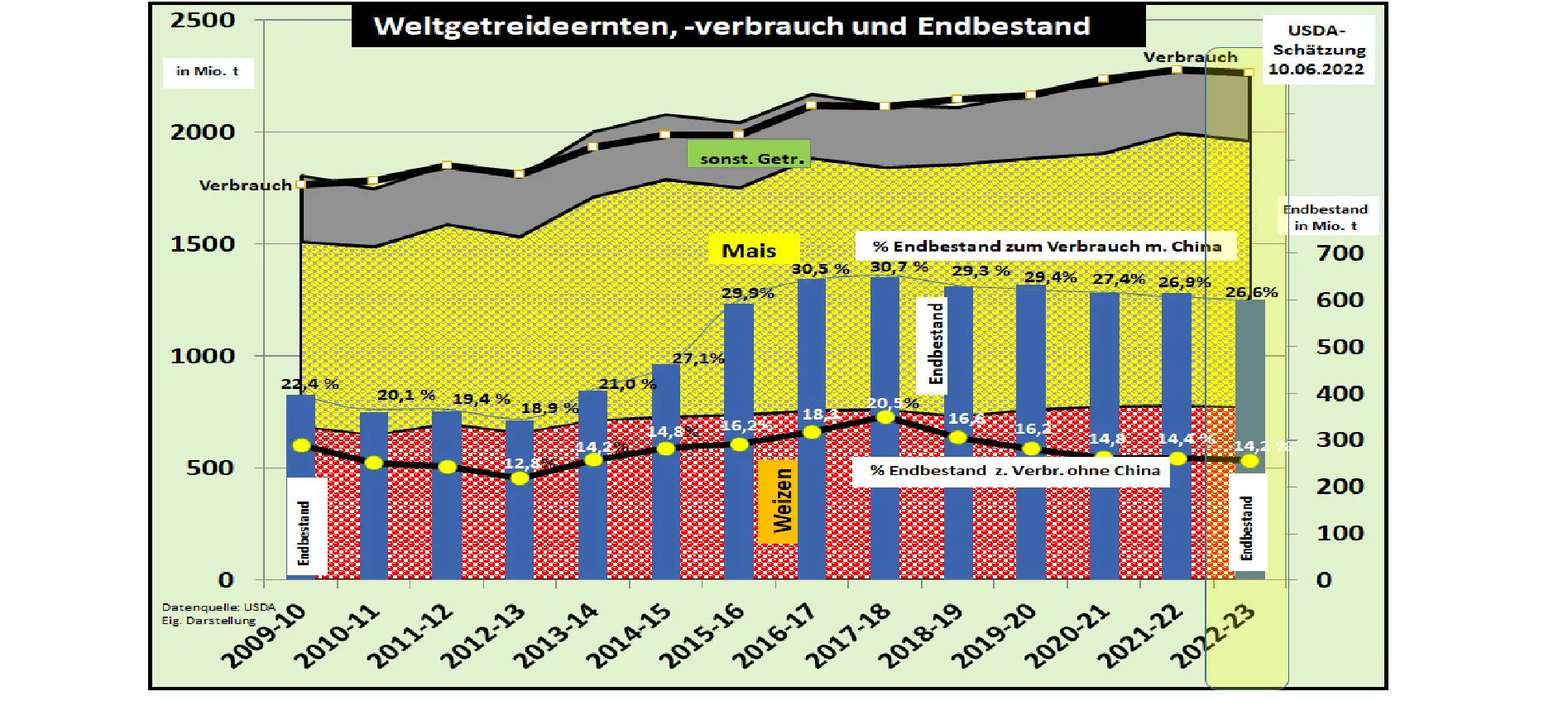

USDA estimates global grain supply for FY 2022/23 below previous year In its June 2022 issue, the US Department of Agriculture (USDA) has estimated the world grain harvest for 2022/23 for the second time. Global production is estimated at 2,252 million t (previous year 2,280 million t). The decisive factor is the poor harvest in Ukraine due to the war. Global consumption is also classified as lower at 2,266 million t (previous year 2,287 million t). The ending stocks were calculated at around 602 million t (previous year 608 million t). The supply figure falls to 26.6% at the end of the year (26.9% in the previous year); reserves last for 97 days, but excluding China's ending stocks, stocks only last for 52 days. In global world trade , the quantities rose to 432 million t (previous year 465 milliont) shortened. In the case of the Ukraine , the USDA assumes an export volume of around 21 million t (previous year 60 million t); exports of 50 million tons of grain (previous year 42.5 million tons ) are expected for Russia . Export increases are forecast for Canada, USA, Australia and the EU. Despite the drought , India is expected to export a reduced 6.5 million tonnes of wheat. On the import side , the critical supply situation in the North African and Middle Eastern countries is confirmed with reduced import quantities. China is to reduce its grain imports by around 10% . The figures for Ukraine are to be viewed subject to political and military developments. The USDA estimates the harvest at $53.3 million.t (previous year 86.5 million t), exports should reach 21 million t (previous year 60 million t). Compared to previous years, around 40 million tons of exports or around 10% of world trade are missing and the rest is still uncertain. The global grain supply continues the decline that has been observed for years. Against the background of the war in Ukraine, the assessment of security of supply is considerably more critical. Fear of supply has become a price-determining factor. The USDA estimates the wheat harvest at around 773 million tons , slightly below the previous year's figure of 779 million tons. The world's largest producer, the EU-27 , will harvest only slightly less at 136 million tons and export an increasing 36 million tons. China's wheat harvest is estimated at 135 million tons with an import volume of 9.5 million tons. For India , the USDA expects a wheat harvest of 106 milliont , of which 6 million t are to be exported while stocks are reduced. For Russia , the USDA is forecasting a 7% increase in wheat production of around 81 million tons; Russian exports are estimated at 40 million t (previous year 33 million t). The US harvest is expected to reach 47 million tons , of which 21 million tons will be exported. After last year's disastrous result, a wheat harvest of 33 million t (previous year 21 million t) is expected in Canada , of which 24 million t (previous year 15 million t) will be exported. On the import side there are 28 countries that are existentially dependent on wheat imports . These include most countries in North Africa, with Egypt at the forefront, many countries in the Middle East and Southeast Asia.The USDA estimates the import volume to be slightly higher than in previous years, but the high prices may still curb the import volume. The USDA estimates the global corn harvest at 1,186 million t (previous year 1,216 million t). This is compared with an equally high consumption (previous year 1,198 million t). As in the previous year, the calculated final stock remains at 310 million t and lasts for 95 days, but only 43 days without China. The US corn harvest is estimated at 367 million t (previous year 384 million t). The decline is mainly area-related, because more soybean (without need for N fertilization) is cultivated. The USA is expected to export 61 million tons of corn. The Brazilian corn crop is expected to deliver 126 million tons, of which 47 million tons are to be exported. A corn yield of 68 million tonnes is expected in the EU-27 ; 15 million are required to cover requirementst imports required. A good harvest of 55 million tons is expected in Argentina , of which 41 million tons will be exported. Overall, global corn trade will be 7% lower than last year. In addition to the EU, other large import regions, each with around 15 million tons, are Mexico, Southeast Asia and Japan . China is reducing its previous imports of over 23 million tons to this year's 18 million tons. The USDA report initially caused mixed developments on the stock exchanges . In Paris, wheat is currently trading a little higher at €385/t, while the Chicago prices have eased somewhat. In the case of corn , prices have risen at both stock exchange locations .The Paris Stock Exchange is currently trading rising €335/t corn . However, the later dates until autumn/winter 2022 indicate lower prices. The assessment of the price development cannot be explained primarily on the basis of previous empirical values, but mainly from the point of view of tension-laden fears of supply as a result of outstanding weather-related harvest risks, high energy costs, uncertain supply chains and, last but not least, unforeseeable political and military developments.