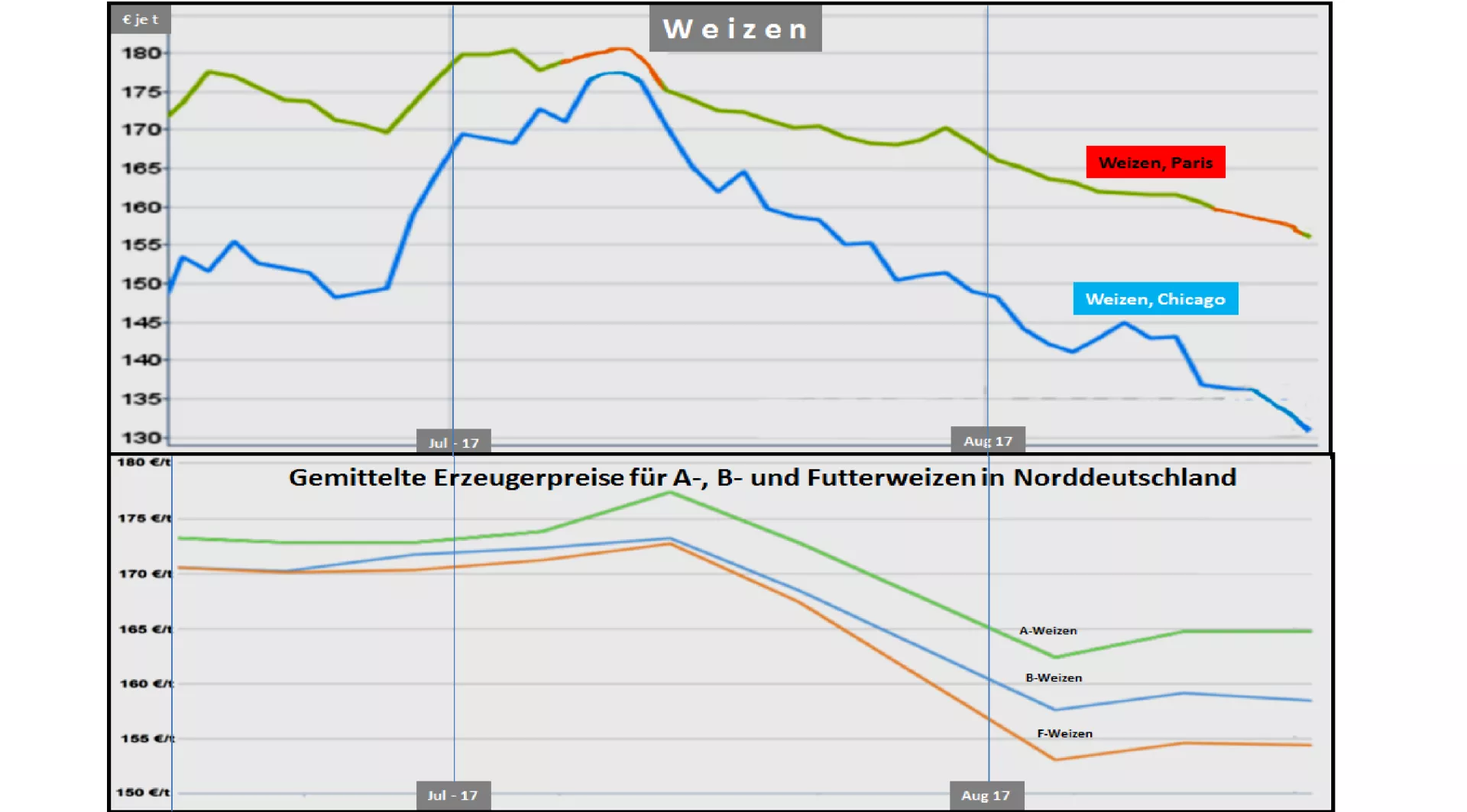

Declining wheat prices - but with considerable regional differences High wheat harvest with an emphasis on the Black Sea countries lead to yielding wheat courses on the exchanges. High export volumes are expected at reasonable prices in this area. This means strong competition for EU exports . The comparatively high European price makes EU wheat exports even less competitive. The wheat courses in Paris are taxing at € 155 / t. Despite a weak US crop, the unusually high overhang stocks are sufficient to provide sufficient quantities for domestic supply and export. The exception are high-quality protein-rich wheat varieties. The US wheat indices are controlling Converted to 130 € / t. The drop in prices in the US is significantly stronger. This is because of the limited export opportunities, because the eligible large wheat feed countries in the North Africa and the Middle East are supplied by the Black Sea countries and the EU. In the South-East Asian region, Australia is able to provide its own recruits from the previous year. In addition, the US maize harvest creates pressure on the quotation level.Although local producer prices have been on the decline in prices at the end of July to beginning of August-2017, they are clearly in the middle of August in the northern German processing areas . The available goods are limited by the delayed and reduced harvest. Duty to deliver Of producers remains cautious in the face of low prices. Last but not least, goods are exported for export in the vicinity of the harbor. What is striking is the increasingly recognizable spreading between the wheat qualities , a visible expression that this year will again be missing due to weather conditions due to higher quality goods. Breadmills are in France in search of replacement.In the remaining German production areas , persistently weaker bread wheat pots are observed. In the German average, the prices fell to € 149 / t and are still lower in the eastern federal states. Feed wheat is located in the federal state at 141 € / t. The range extends from just 160 € / t in western Lower Saxony to 127 € / t in Thuringia. With the end of the harvest, the usual calm post- harvesting phase will begin. It is possible that the pause in this year is less pronounced because it has often been impossible to satisfy the supply requirements.

ZMP Live Expert Opinion

Wheat prices are driven by limited supply areas in the USA and the EU and the above-average harvest and export offer from the Black Sea countries. The coming weak harvest of Australia could be in the connection supply in Nov. / Dec. 2017 still play a decisive role. In addition, the fluctuating exchange rates must be taken into account. If necessary. Trade policy decisions still play a role.