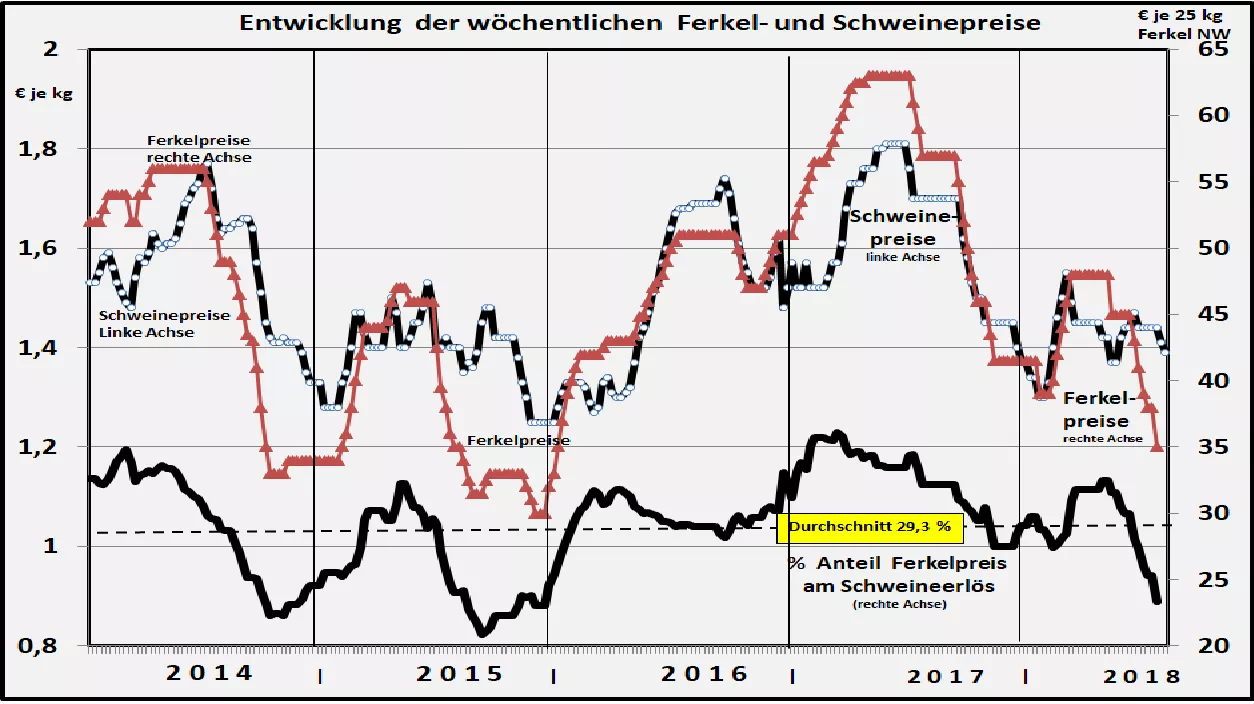

Relationships between piglets and piglets There are basically close but also peculiar relationships between piglet and pig prices. First of all, the predominantly simultaneous upward and downward trend is noticeable, of which deviations are more or less pronounced only in a few cases. Actually, a time course offset by the fattening period would take place. But obviously the piglet demand of the males plays the more decisive role in the piglet price finding compared to the limited assertiveness of the piglet supply.The high penetration power of piglet demand can be observed especially in times of weak pig prices . Low revenues in the mast regularly lead to a declining willingness to stabling with unchanged average piglet supply. The resulting supply overhang leads to disproportionately low pig prices. Distinctly typical periods were observed in the autumn months of 2014 and 2015. Recently, such a development will take place again from the summer of 2018 . The fact that the price decline is not an increase in the piglet supply can be seen in the below-average trading volumes of the piglets.In return, a market dominance of the piglet supply is to be proven on the prices in the short periods of high pig prices. This happened in mid-2014 and even more pronounced in 2017 with disproportionately high pig prices. With high sales proceeds, the demand for piglets increases and the available piglet supply becomes the limiting factor. The season-typical piglet price trend with a high in the spring months and a low in the autumn months does not always come into its own, because other factors overlap.The typical spring high is caused by a short supply of piglets due to the below-average fertility of the sows in the hot summer months with high Umrauscherquoten. The autumn depression arises from the opposite effect. The share of piglet prices in pig prices has increased significantly in the last 10 years. The decisive background is the increasing German piglet deficit of approx. 20%. Sufficient piglets numbers are only about the import of approx. 12 million animals per year. Suppliers are in 1st line Denmark with 6.5 million and Holland with 4.5 million.The continuing heat wave and the current low piglet prices should help to ensure that piglet availability will be significantly lower next spring.