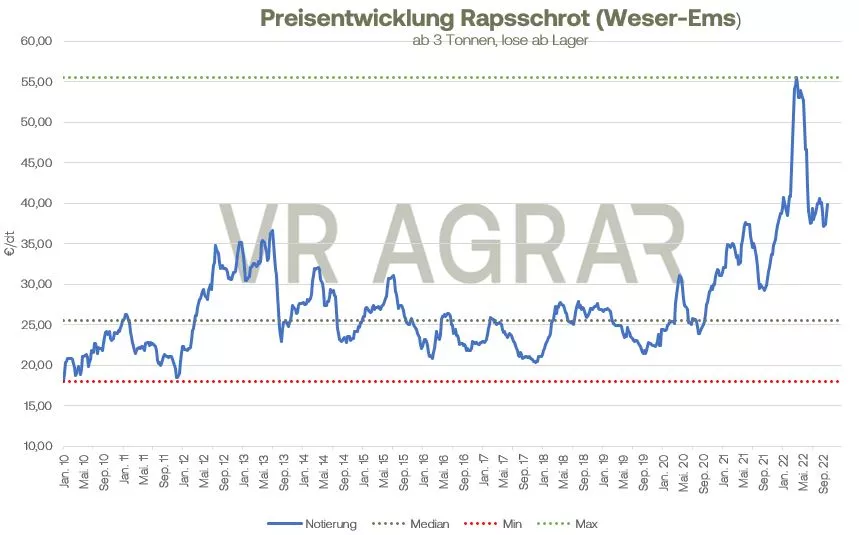

Even if rapeseed prices started towards EUR 650 per ton at the beginning of the week, they have been weaker overall since the beginning of the week. However, the rapeseed contracts on the Euronext/Matif have not lost any of their volatility this week either. On individual days, there were clear gains and double-digit losses. The better supply of rapeseed on the European market due to the good harvest conditions in Canada repeatedly dampened the mood. On the other hand, however, the firmer crude oil and price gains in the soy complex continue to support the prices on the Euronext/Matif. With the back and forth of the stock exchange prices, the spot market listings in Germany were also changeable. Overall, however, it remains the case that only a small amount of rap is currently being implemented. This is due to both the demand and the producers' willingness to sell. In the updated harvest forecast of the EU Commission, a rapeseed production of 19.2 million tons is currently assumed. In the previous year, 16.9 million tons were harvested. The harvest volume is thus 11.8% larger than the average for the past five years. In its September WASDE, the USDA had already predicted a better global rapeseed supply of 10 millionTons spoken over last year. The EU Commission has adjusted its forecast for Germany to 4.29 million tons, which corresponds to an increase of 20.2 percent compared to the five-year average. Trading in the soybean complex was also volatile this week, but soybean prices fell significantly on a weekly basis. The soybean complex was repeatedly supported and pushed up by the rising price of crude oil. However, the current harvest and the recent good harvest conditions, together with fears of a global recession, repeatedly weighed on the mood. Although the USDA was able to announce isolated export sales, overall yesterday's export sales disappointed market participants. Giese were again significantly lower compared to the previous week, but the total annual volume so far has been exceeded by 4.5 percent. The dealers are already positioning themselves for the coming October WADE. This coming Wednesday will be released by the USDA. According to the first surveys, market participants are expecting a slight upward adjustment in the harvest volume. The extensive acreage in Brazil is also depressing the mood.New records are expected for Brazil, both in terms of acreage and production. Competition also continues to come from Argentina. However, the stocks that have been ordered have had a difficult time here recently due to a severe drought.

ZMP Live Expert Opinion

The harvest pressure is reflected in soybeans, while in the case of rapeseed the better supply keeps putting pressure on prices. But the situation remains as it is: without a very clear direction. The geopolitical tensions, the economic outlook, central bank policy - everything has an impact