USDA estimates oilseed market 2014/15 continue at record levels

The entire oilseed crop of soybeans over canola, sunflower, peanut, and palm oil the U.S. Department of Agriculture estimates good last year compared to continue on just 529 million t. the increase again less than 5%. On the consumption side, 3.5% is projected to increase rd. Stock inventories, which for the first time exceed 102 million tonnes arising in connection with the high initial levels. The inventory build-up reached values of + 20%. The result is a pure ample supply of oilseeds total.

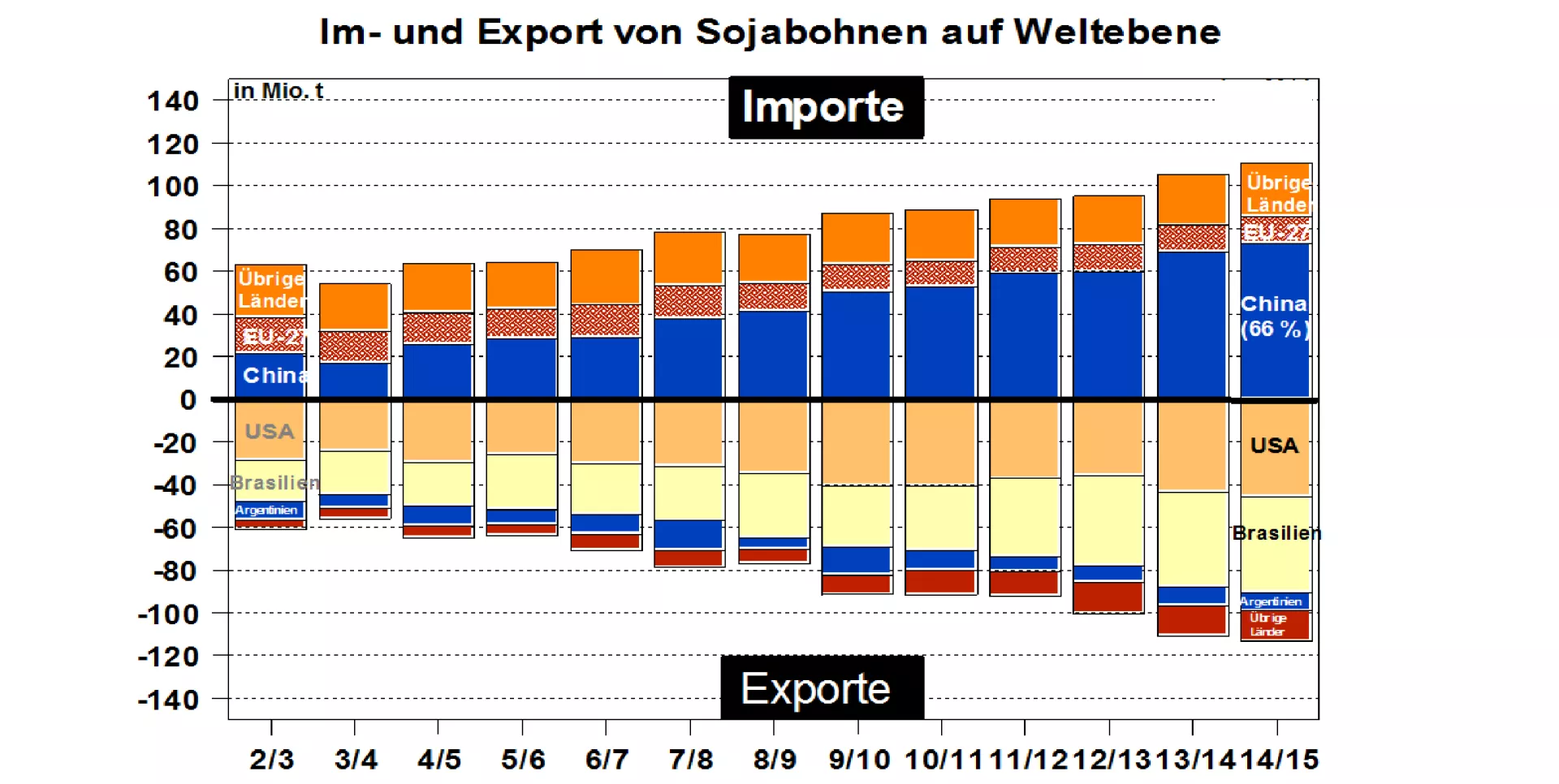

However, the large average isn't all about the market situation still says. With a share of approximately 60% of soybean seed sector dominates the market, while in the vegetable oils along with soybean oil, especially palm oil considered market leader. The other oilseeds adhere to their previous level. Which are problems of logistics in the United States and in South America the export policy soy harvests should according to estimates to 2014/15 + 9.5% grow. The largest increase is expected in the end U.S. crop with an increase of 15%. Despite delayed planting, the USDA continues to be of a high Brazilian harvest of 94 million tonnes (previous year 86.7 million tonnes) from the spring 2015, while Argentina is predicted a good average harvest of 55 million tonnes. Total is to rake from the supply side, with a significant increase. However there is still a significant production and crop risk still is located in South America only in sowing the first-fruit? Possibly second fruit cultivation is even riskier.

Calculated on the consumption side will be an increase of about 5% for the soy sector. The Chinese Importzuwachse of approximately 4 million tonnes while plays a significant role. Last year, the Chinese had increased their import volumes and approximately 10 million tonnes.

The calculated soya stocks grow to over 90 million. t at the end of the year 2014/15. This is an increase of more than 35% from year to year. A such favorable supply situation has not yet been there.

The soybean prices gave while already vigorously since the summer, but in recent times, bottlenecks in the U.S. market have occurred, have again driven prices upwards. The reasons are quickly uncovered: extremely low end stocks, a delayed soybean harvest, strong export activity and insufficient transport capacity were stronger than the coming of the field quantities of soy. In many parts of the country, especially the soybean meal was missing, while in soybean oil was not short. Hamster effects seem also to have played a role. Given the large supply of the U.S. crop of nationwide need satisfied soon will be, so that a price stabilisation phase with rate reduction potential in the next few months is expected.

However, even high risk premia in the courses remain priced, because both the weather than the sales behavior in South America will talk to still the one or the other Word.

ZMP Live Expert Opinion

The most recent estimate of USD confirmed the expectations of highest harvest results in the oilseed sector. Focus is the completed record crop with soybeans in the United States and the large harvests in the South American countries. Sowing half is done in Brazil. Argentina has lagged behind a bit. After several risks into the business to the market.

On the demand side, China developed brisk import activities. But the estimates so large import growth compared to the previous year by a half.

With the foreseeable removal of technical supply problems in the U.S. soy sector, soy prices of above-average supply situation should take into account and give. This basic tenor by unforeseen Störungen.unterbrochen can be at any time.