USDA: ample supply of the oilseed market 2014/15

The latest estimate of the U.S. Department of agriculture to the oilseed market confirms the already known observation an another record harvest in the Sept./Aug 2014/15 marketing year

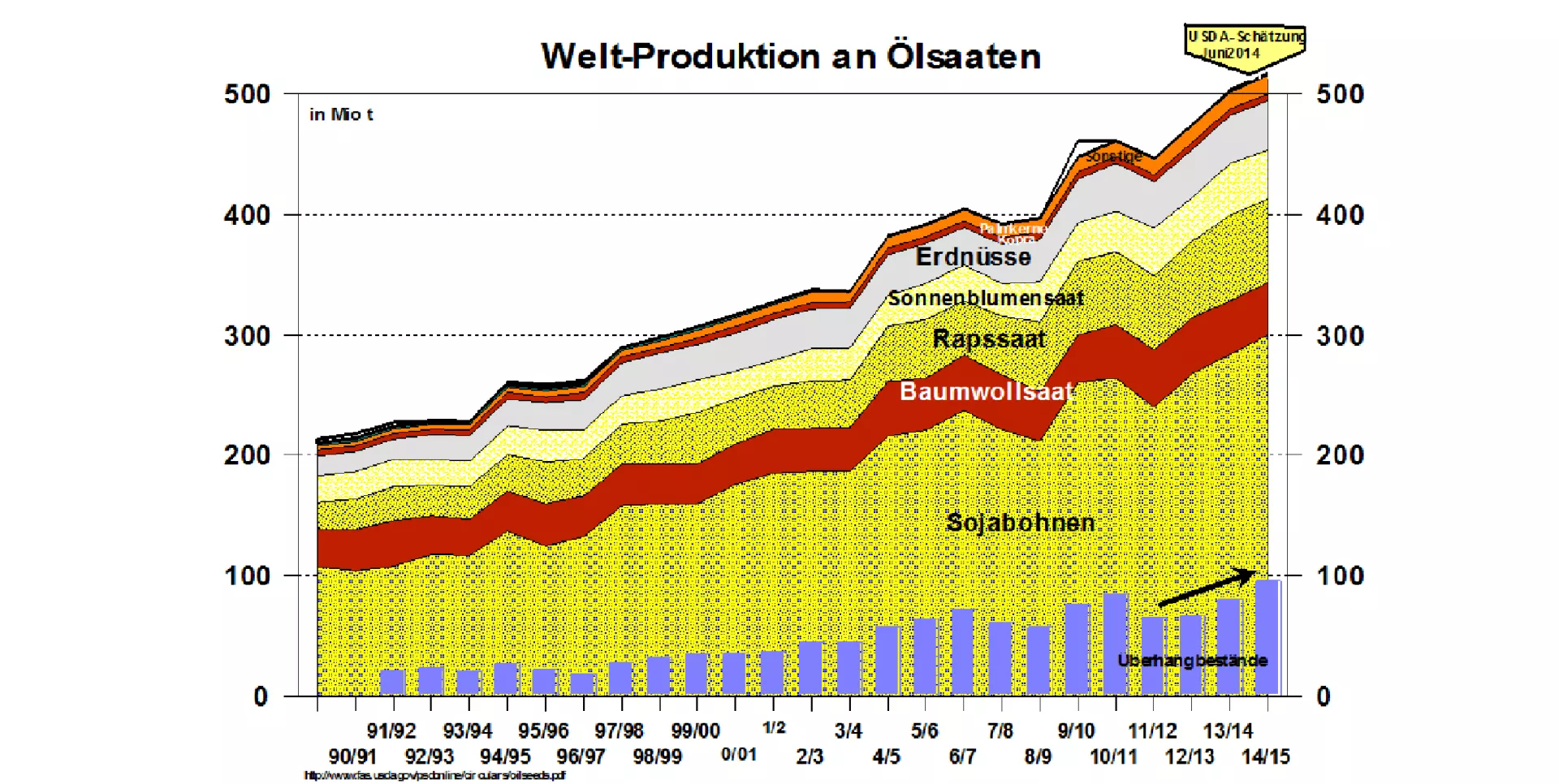

2 striking targets are exceeded equal for the first time: there are 500 million tonnes for all oilseeds together and for soybeans the 300 million tons mark. It is already clear that the decisive growth spurt comes from the soy complex and other oilseeds of rape (14%), of cottonseed, sunflower seeds, peanuts, palm kernel and copra only slight changes are to be expected.

When measured by the market of vegetable oils , even palm oil with a market share of 30% added ahead of soybean oil and rapeseed oil as the second leader , which has significant role in the price formation. The palm oil market is concentrated to 90% on the tropical conditions in Malaysia and Indonesia. The rise of the new Produktionssaison, which reaches its climax in the Sept/Oct starting March/April. The inventories are already at least 10% higher than the current crop. At the same time exports due to the pressure of competition goes back including soybean oil, so that will be further strengthened when increasing yield stocks. The result is considerable price pressure. Palm oil prices are once again at a low level of $750 fallen je after almost a month on buw above the $800 depending on the brand had been t. The strong pressure of competition affects especially rape the entire rest of the oilseed market.

If you offset production and consumption of oilseeds total for the year 2014/15 is calculated a sharply rising closing stock of approximately 96 million tonnes compared to the previous year with 80 million tonnes. This one is above average good until ample supply in the oilseed market, the up to date not yet been has.

The consequences of the plentiful supply situation are falling prices, which now already vigorously have used in rape. In the soybean meal market perspective as a result of the bottleneck situation in the United States looks even slightly more critical until the new harvest in September 2014. Meal prices give initially reluctant and until the price node should burst with increasing security of the expected bumper crop in the United States by almost 100 million tonnes.

Also the Frühjahrsernten2015 in South America belong to the marketing year 2014/15 . The expectations are high here, too. However there are still a number of risks. The biggest uncertainty provides the weather phenomenon El Nino, which can provide with drought in Pacific region for earnings. Depending on the year-specific expression, the possible damage can fail in the second half of 2014 different sizes. This may slightly raise the depth of rapeseed prices and slow the fall in soya prices.

ZMP Live Expert Opinion

The expected bumper crop in the oilseeds exceed the foreseeable evolution of consumption. Rising end stocks lead to the assessment of a plentiful supply situation in the marketing year 2014/15.

There are still a purity of growth and harvest risks to overcome until the actual harvest. The biggest challenge is the weather anomaly El Nino, whose shaping each time will vary in the second half of 2014.

The forward rate on the stock markets show a significant descent of the oilseed market prices, whose Reichweite will go in the next year of 2015. The direction is clear, the extent remains open.