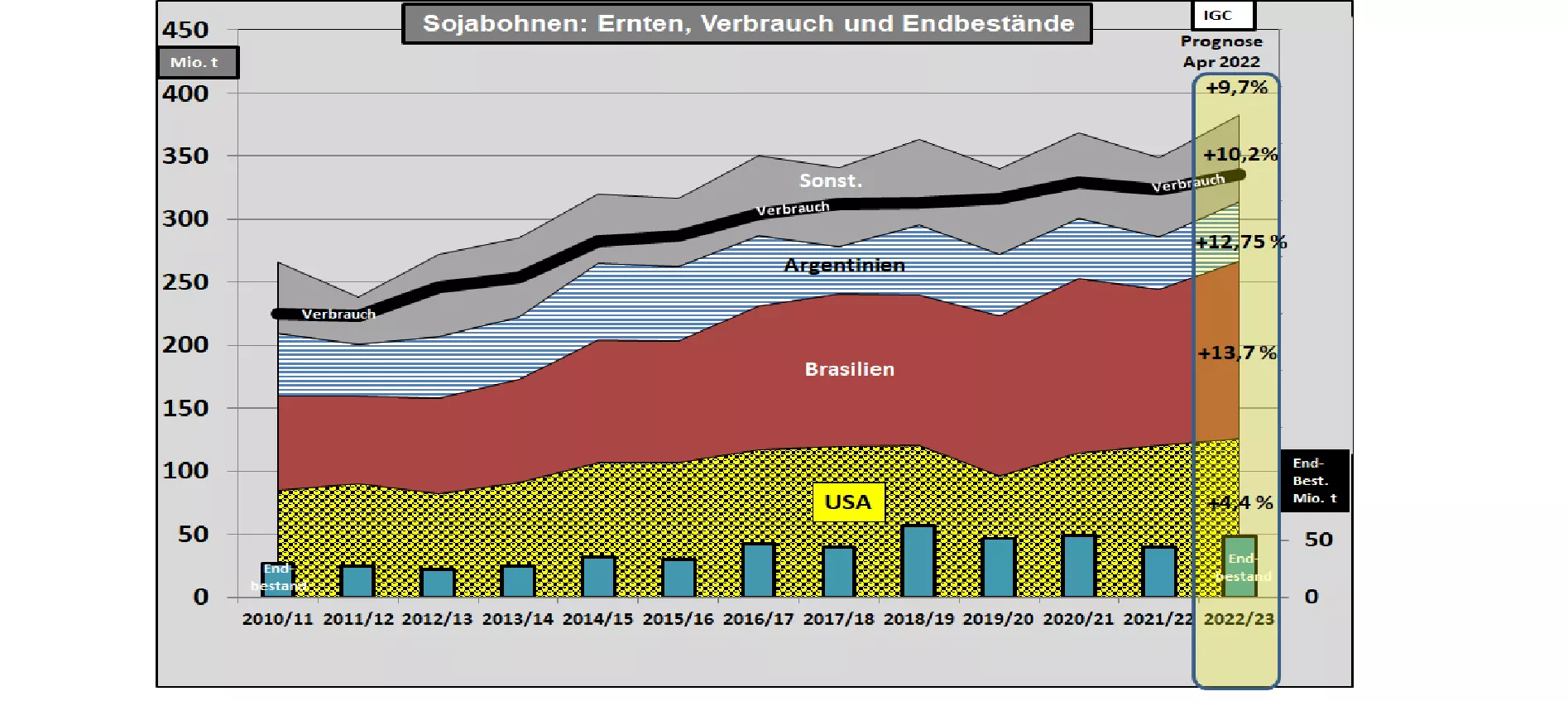

IGC estimates 2022/23 soybean harvest 9.7% higher In its April 2022 issue, the International Grains Council (IGC) estimated the global 2022/23 soybean harvest to be +9.7 % to around 383 million tonnes compared to the previous year . Global consumption is also estimated to be higher at 373 million t . The ending stocks (EB) rise to 54 million t or 14.5% EB to consumption . In the previous year, the coverage figure was 12.3%. The supply figures without China are at the current 9.7% ending stock to consumption (previous year: 6.4%). On the production side, the increased harvests in Brazil (+17 million t), in the USA (+6 million t) and Argentina (+5 million t) are making a significant contribution to the increase in supply. In Paraquay , after last year's bad harvest of 4.3 million t, this year's result should end up at 10 million t .In contrast, the Ukrainian harvest is downgraded from 3.4 to 2.2 million tons . On the demand side , China's imports dominate with 98 million t (previous year 93 million t). This corresponds to around 60% of world trade. Soy imports in the EU remain at 15 million tons . Despite China's increasing purchases, inventories are increasing from 44 million t to an arithmetical 54 million t. For Brazil , the IGC estimates that ending stocks will double to 6.5 million t. For the 3 largest exporters , ending stocks are back to where they were two years ago. Measured against the outstanding harvest risks, the reserves are still limited. Soybeans for May-2022 have fallen back to €590/t on the Chicago Stock Exchange . Only 518 €/t are traded for Nov 2022 .US soybean meal (48%RP) falls to the equivalent of € 475/t for May delivery and is trading at €432/t for the Dec 22 deadline . Soybean oil prices are taking the same direction. On the Hamburg Stock Exchange, German soybean meal (44/5) is quoted at €521.50/t for May delivery and will fall to €517/t by the end of 2022.