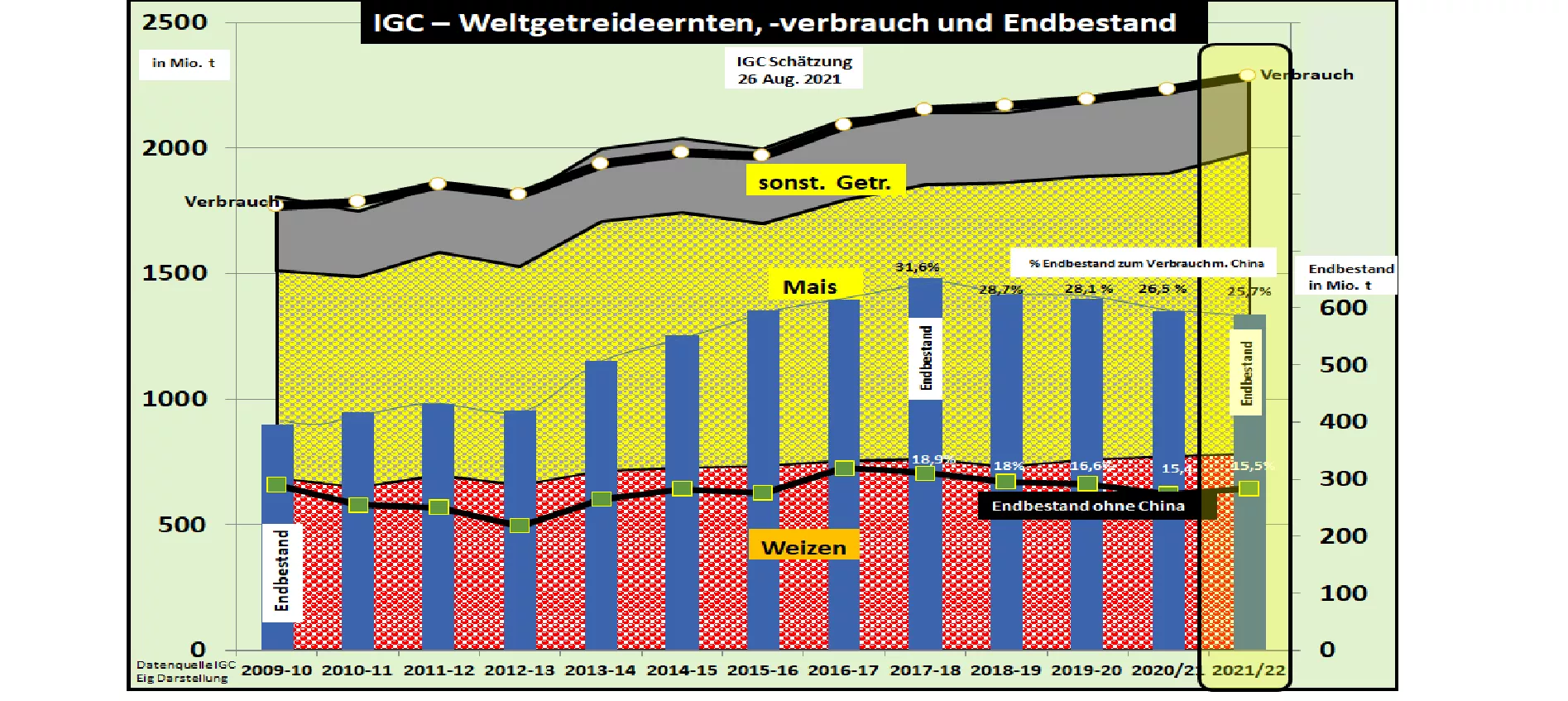

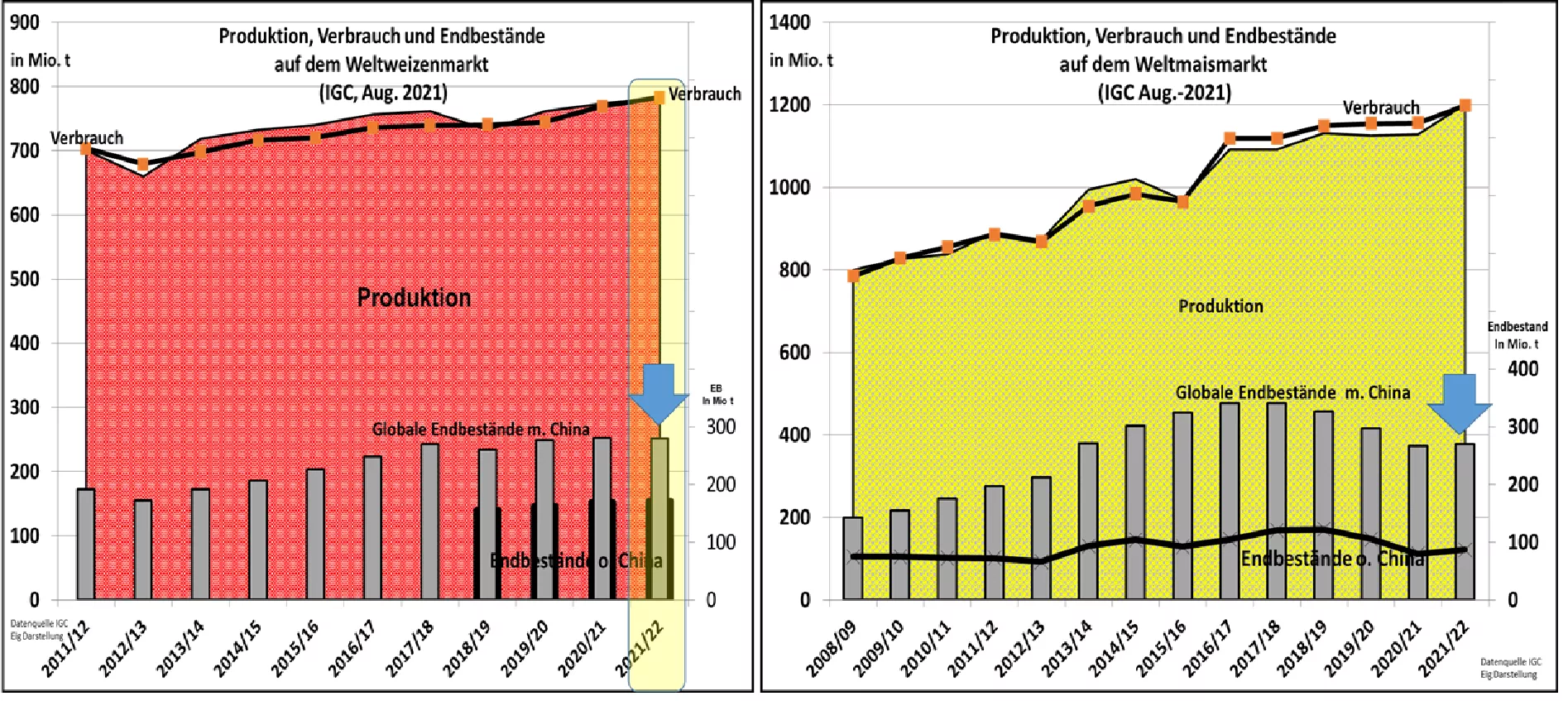

Aug. 2021: IGC shortens world grain harvest 2021/22 with the previous month - supply close The International Grains Council (IGC) estimates in its Aug.-2021 edition of the global grain harvest to 2,283 million tonnes, or 12 million t small it than the previous month . Compared to the previous year, however, the result remains + 3.2% higher. Consumption is estimated to be 7 million t lower than the previous month to 2,288 million t . This means that the excess stocks have dropped to 589 million t . The global supply figure declines to 25.7% final inventory to consumption. In the previous years the figure was between 28 and 26.5%. The supplies last for around 94 days, 3 years ago it was 105 days. If one examines the market situation without China , one comes to a supply figure of 15.2% final stock of consumption compared to the two previous years with 15.4% and 16.5% respectively. The supplies last for 56 days, unchanged from the previous year.The global wheat harvest remains at a record level with a cut of 782 million t. Compared to the previous year, the increase is only +1.9%. Consumption will be reduced slightly to 783 million t (previous year 770 million t) compared to the previous month. This results in a slight stock reduction from 281 to 278 million t. The supply figure falls from 36.5% to 35.5% final inventory for consumption. This means that the wheat market in and of itself is still relatively well supplied. The expected high wheat production in Russia, Canada and the USA was revised downwards, while the high harvests in Ukraine and Australia were confirmed. The IGC estimates the global corn harvest unchanged at 1,202 million t or +6.6 % higher than in the previous year. The US, the world's largest producer and exporter of corn, has made rapid progress this year after initial difficulties.On the other hand, significant cuts have been made in the Brazilian second corn harvest. Global corn consumption is expected to increase by 3.9% year-on-year to 1,201 million t. The increasing development in China is particularly contributing to this. Global inventories are marginally to 270 million tonnes rise in the course of the maize marketing year 2021/22. The supply figure remains at around 22.5% final inventory for consumption. 4 years ago, the excess stocks were up to 30% based on consumption. Global supplies last for 82 days (34 days without China; 44 days ago 2 years ago). Overall , it can be stated that despite increases in production, the supply situation is estimated to be somewhat tighter again. The increased generation is more than offset by increased consumption. The supply situation is tighter in the corn sector than in the wheat market. An increased amount of feed wheat has a balancing effect. The temporary decline in grain prices on the stock exchanges has stopped for the time being. The Paris prices rise again to around € 250 / t. The corn prices stabilize on the achievedLevel.