New Zealand's declining performance of grazing leads to lower milk production – Europe's weak euro favours exports of dairy products with lowest rates

Three auction results the global dairy trade in a row provided a stabilization of average prices to a total of + 7.2% in 1.5 months. In addition to influences from the demand side, in particular the declining supply volume by more than 11% in the weight falls.

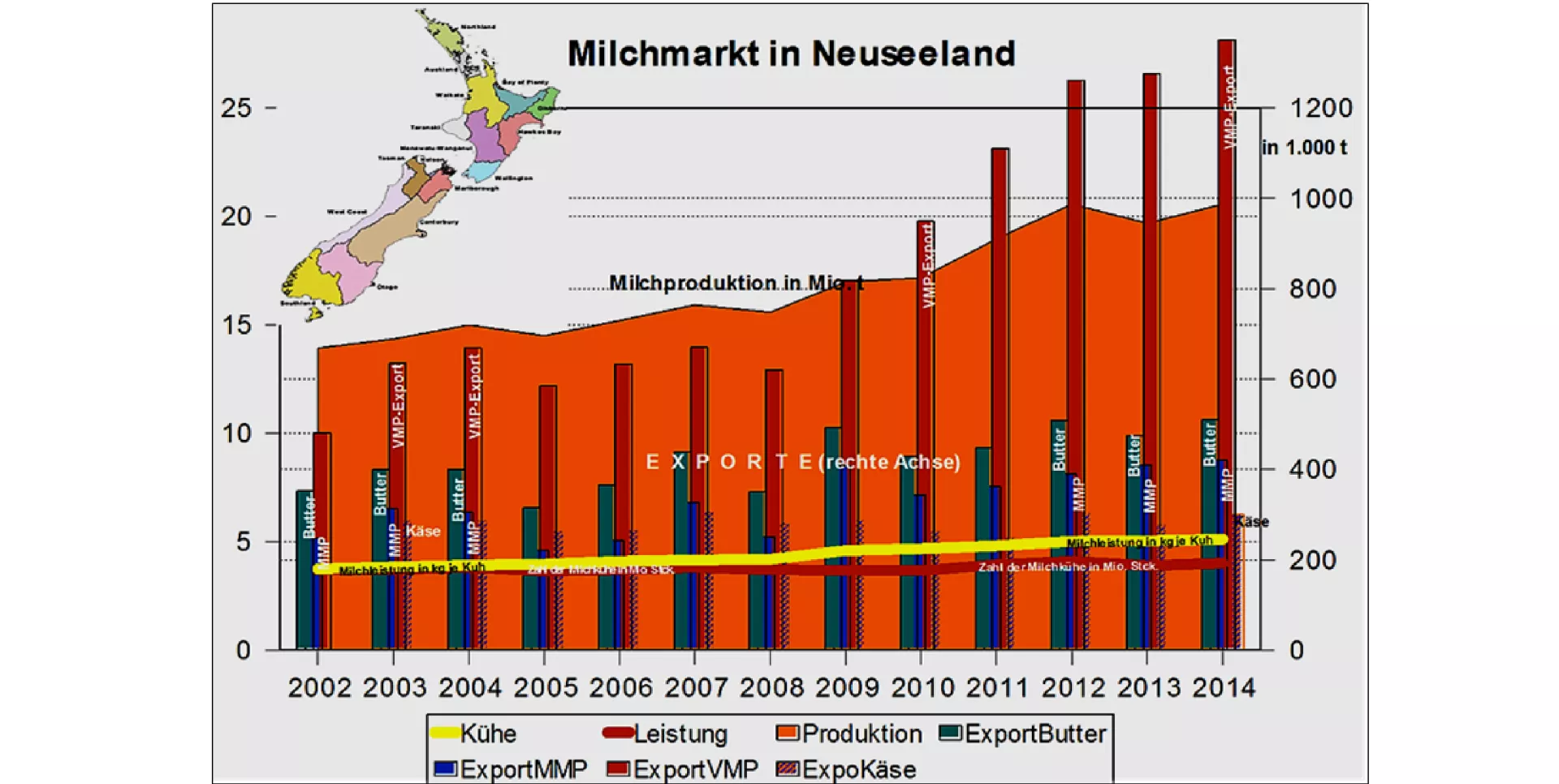

Background is the declining growth of grass on the New Zealand pastures due to insufficient rainfall. The available ground water is becoming scarcer. The prospect of future higher rainfall not very good look. There is talk of a drought. The New Zealand dairy industry will be immediately affected, because canned feed, or concentrated feed are virtually unknown.

With an export share of 95% of New Zealand dairy each change is reflected immediately in the amount of exports. That in turn affects international trade and to read the prices for dairy products, such as the last 3 auction results.

The other major exporters of dairy products such as the EU and the United States feel the relief in the market as a result of rising international prices. However, the different exchange rates in the game come.

Strong dollar exchange rate prevented as a result of booming U.S. economy, that the American milk provider can hardly benefit. In international competition, their price demands are due to the exchange rate too expensive.

The EU and the euro zone , however, are at once in the rare situation that their milk products in international trade so cheap are like rarely before. The weak euro exchange rate makes it possible. The sale of milk powder to Algeria and the Middle East takes ride. Also in the Asian region sales opportunities beckon. These are also urgently needed, the loss of export to Russia, to intercept the stocks jammed on and the still increasing quantity of milk in the EU.

This perspective opens up opportunities of further price stabilization in this country. To what extent already rate increases are possible, the further course of the market will show only. In particular, the future Chinese import behavior will play a crucial role. There is still no return to old import increases of China's to recognize.