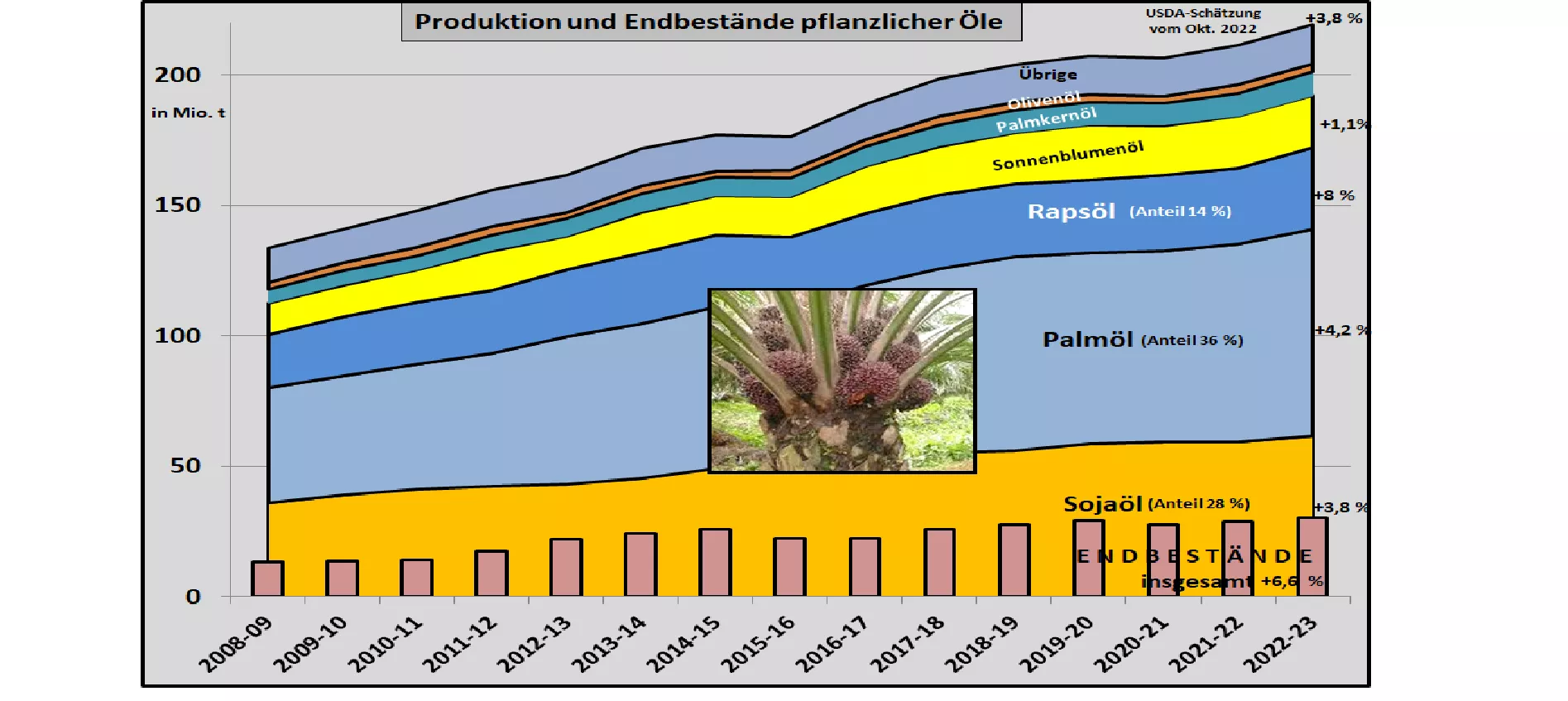

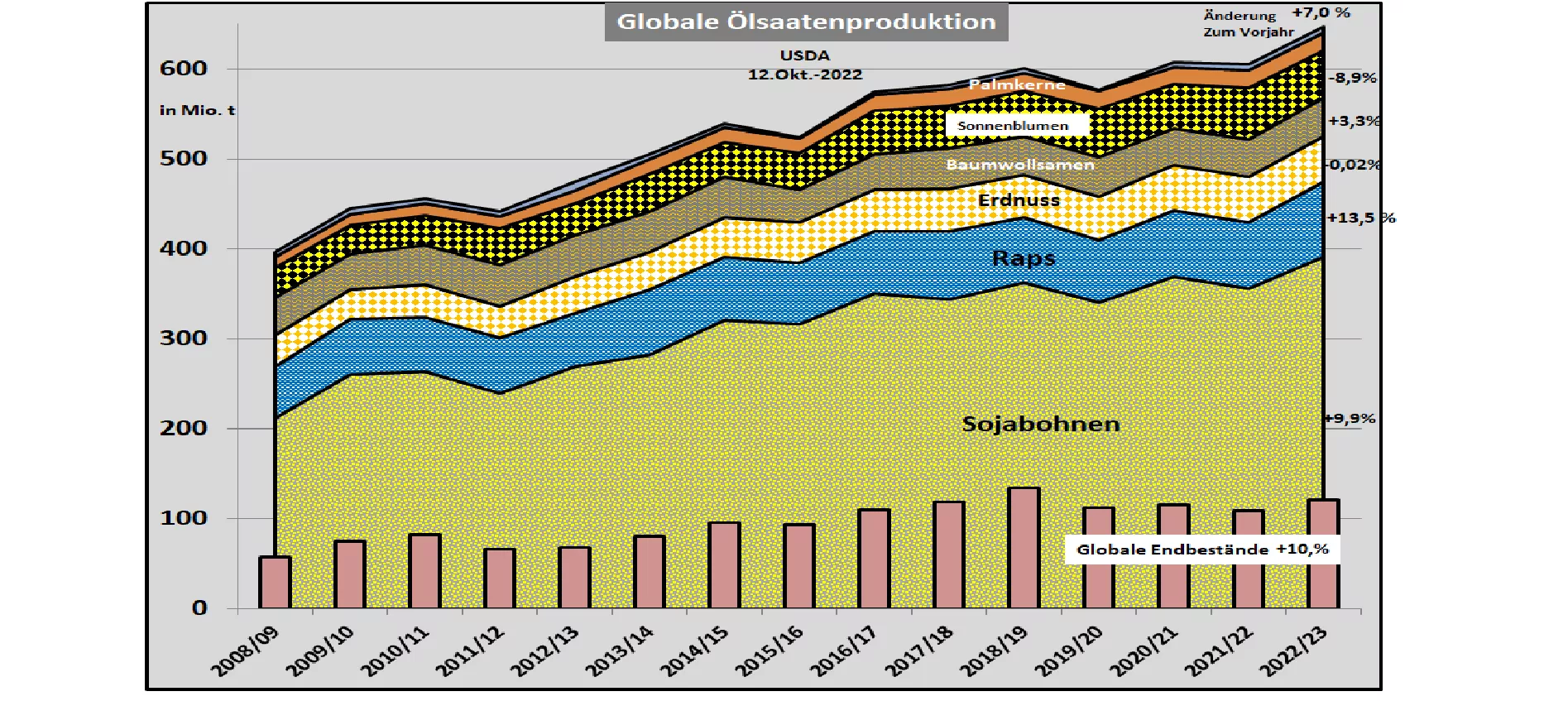

USDA: Global Oilseed Production 2022-23 estimated higher again. In its latest Oct. 22 estimate, the US Department of Agriculture (USDA) once again increased global oilseed production compared to the previous month. The overall result amounts to 646.6 million t (previous year 604.5 million t). Soybean has a significant share with around 391 million tons. Oil seed consumption is estimated at 637.5 million tons. Closing stocks are expected to grow to 120 million tons. This means that the supply situation has improved by almost 8.5% compared to the previous year. The high increase in soya of almost 10% is primarily due to the expected Brazilian harvest of 152 million t (previous year 127 million t). An increase in production of 7 million t to 51 million t is also expected for Argentina . In both cases, the harvest is scheduled for spring 2023. In contrast, production in the USA falls from 121.5 to 117 million.t back; The background is insufficient precipitation in the main production regions. The US harvest is 44% complete. The threshing results have been very disappointing in some regions. Global soy consumption increases to 383 million tons. The world's largest consumer is China with a volume of 118 million tons; of which 98 million tons are mostly imported from Brazil. 14.8 million tons of soybeans and 16.8 million tons of soy meal are imported into the EU. Overall, EU soy imports account for around 7% of world production. The EU figures have been largely constant for more than 10 years, with a slight downward trend recently. A higher increase in production than consumption leads to an inventory build-up of around 8% at the end of the year. The supply situation is improving compared to previous years. The global rapeseed production increases from last year's 73.8 to the current 83.8 million tons. The strong increase is a consequence of the normalization of Canadian production to 19.5 million t compared to the catastrophic result of the previous year with 13.7 million t.In addition, there was an increase in the EU to 19.2 million t as a result of the increased cultivation area. Worldwide rapeseed consumption is estimated at 80.3 million tons. The EU is the largest consumer with 24.2 million t, followed by China with 16.6 million t. India and Canada are at 11 and 10 million tons respectively. The ending stock increases from 4.8 to 7.2 million t and thus improves the stock reserves. The more favorable supply situation is a key reason for the fall in rapeseed prices. Palm oil production , the most important market leader alongside soya, is estimated at 79 million t (previous year 75.9 million t). The supply situation is also improving in this sub-market. Due to the extensive use of vegetable oils for biofuels , the price of crude oil is one of the decisive factors in pricing. After soaring in May/June 2022 at over $110/barrel, prices for the Brent variety have fallen back to around $90/barrel .This development has contributed significantly to the reduction in oilseed prices.