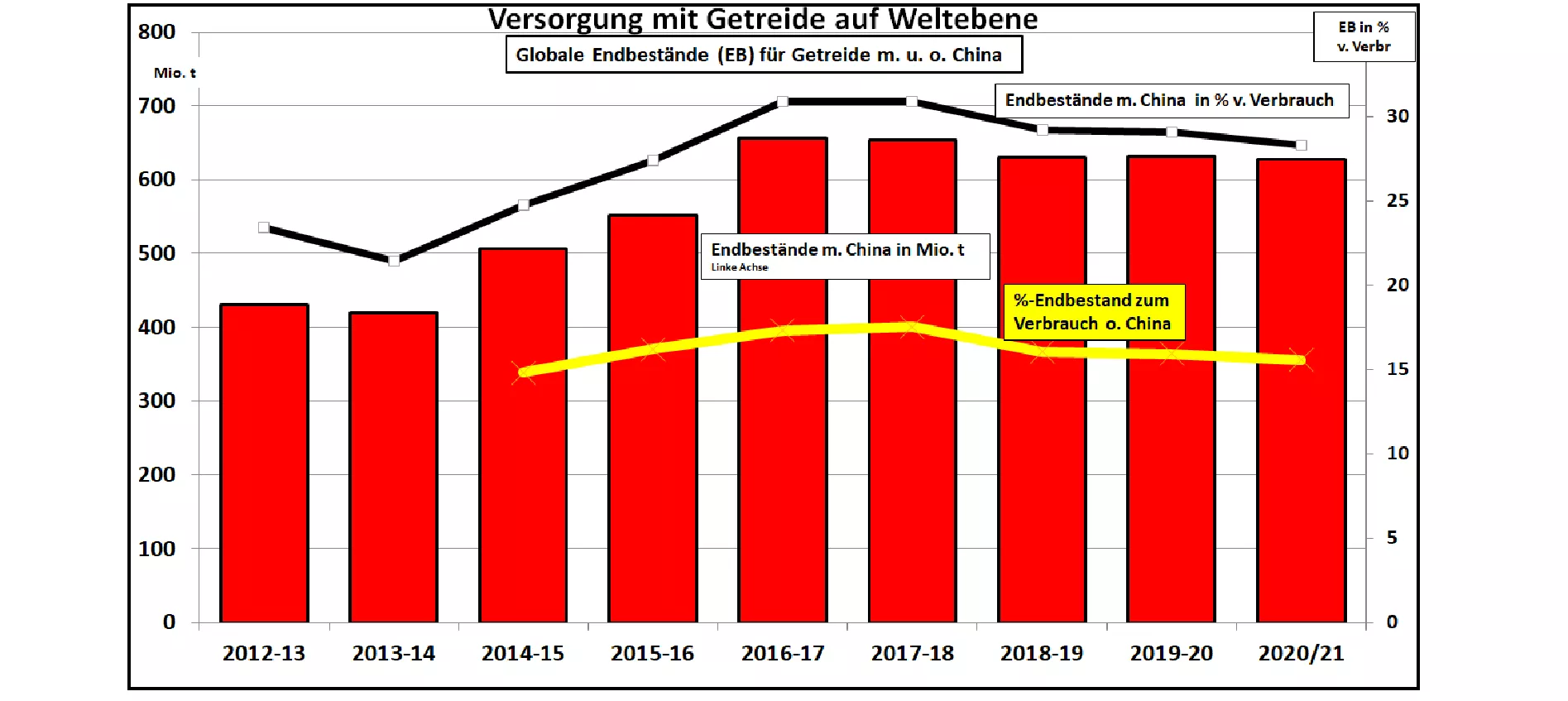

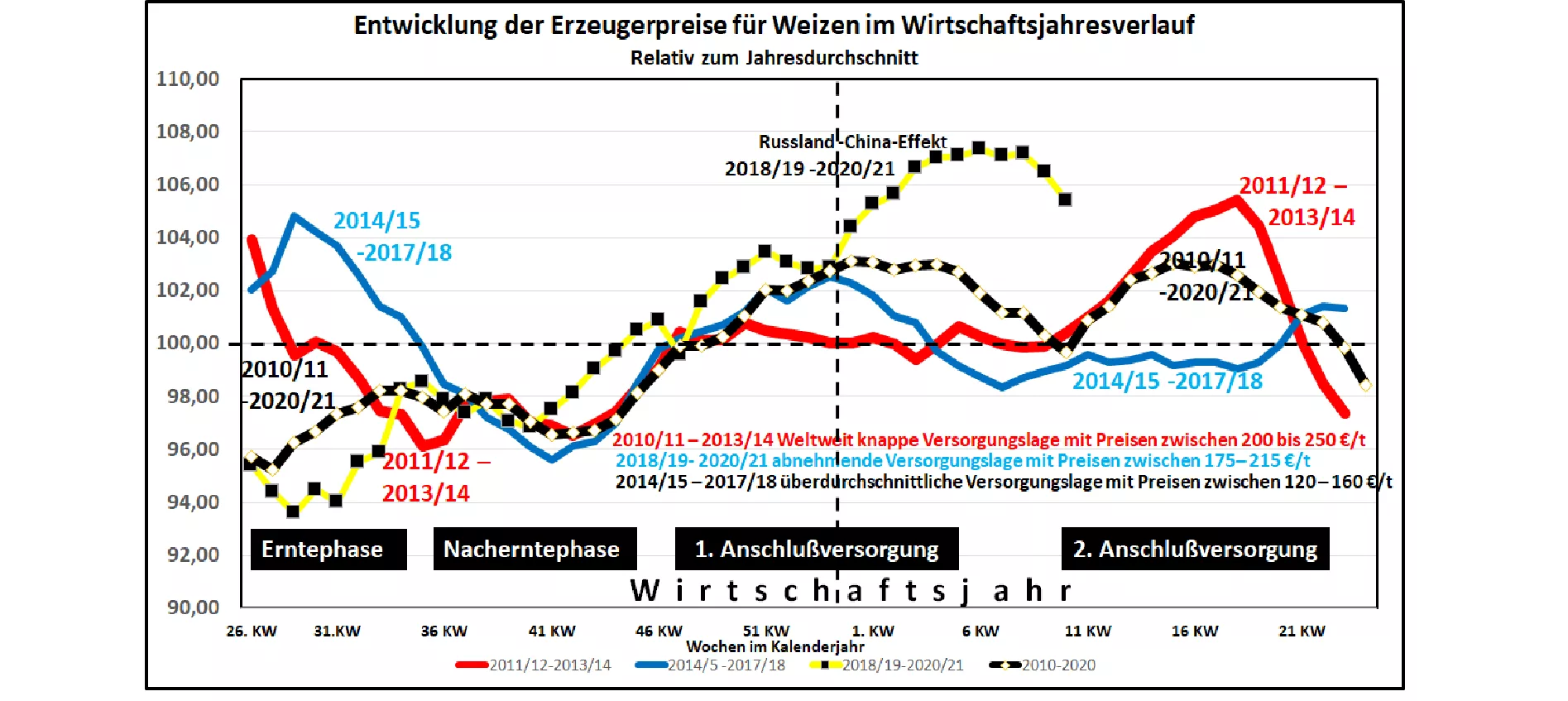

Optimal sales dates for wheat in the course of the fiscal year. The wheat price development so far this year 2020/21 has caused a few surprises. The prices initially rose significantly from the harvest, but remained within the usual developments in a post-harvest period. With the start of the first The follow-up supply phase in November 2020 began an unusually steep period of price increases , which was initially associated with the falling supply situation at world level. Significant support also came from China's sustained high grain imports. After the turn of the year, a second wave of price increases could be observed. The trigger was duty-export in amounts become nearly the decision of the world's largest suppliers of Russia, the export volumes of wheat in the second half of the year economic kontingentiere n and high to provide.On the import side, on the other hand, there was a pronounced precautionary behavior to ensure sufficient stocks under the Covid-19 conditions. If one follows the experience of previous years with similar market and price conditions, then after a spring break, tense price conditions in connection with the second follow-up supply phase until the new harvest cannot be ruled out. It depends essentially on the actually still necessary connection requirement in relation to the available offer . In addition, the ongoing, supplemented knowledge of the expectations of the new harvest plays a decisive role. Experience from the worldwide scarce supply situation in the years 2011/12 to 2013/14 with a high price level of 200 to 250 € / t wheat indicates that another price surge cannot be ruled out at the end of the marketing year.A significant drop in prices as in the well-supplied years 2014/15 to 2017/18, on the other hand, is unlikely . The previous forecasts for the EU harvest results in 2021 can only be compared to the forecasts by COCERAL in the range of the average of 300 million t . According to the previous climate data, MARS estimates somewhat higher yields per area, but a lot can still change. Due to the acreage, the DRV assumes that the German grain harvest will remain below 45 million t. Earlier peak harvests of 50 million tons are out of reach. At the international level , the FAO expects a worldwide wheat harvest of 780 million tons. However, the results in the USA and Russia are estimated to be significantly below the previous year's level due to the weather. The unusually high Australian harvest will not be repeated either. In China , results are expected to be below average.In the case of maize , on the other hand, a large area expansion is expected in the world's largest cultivation area, the USA . How the income will turn out remains to be seen for the time being.