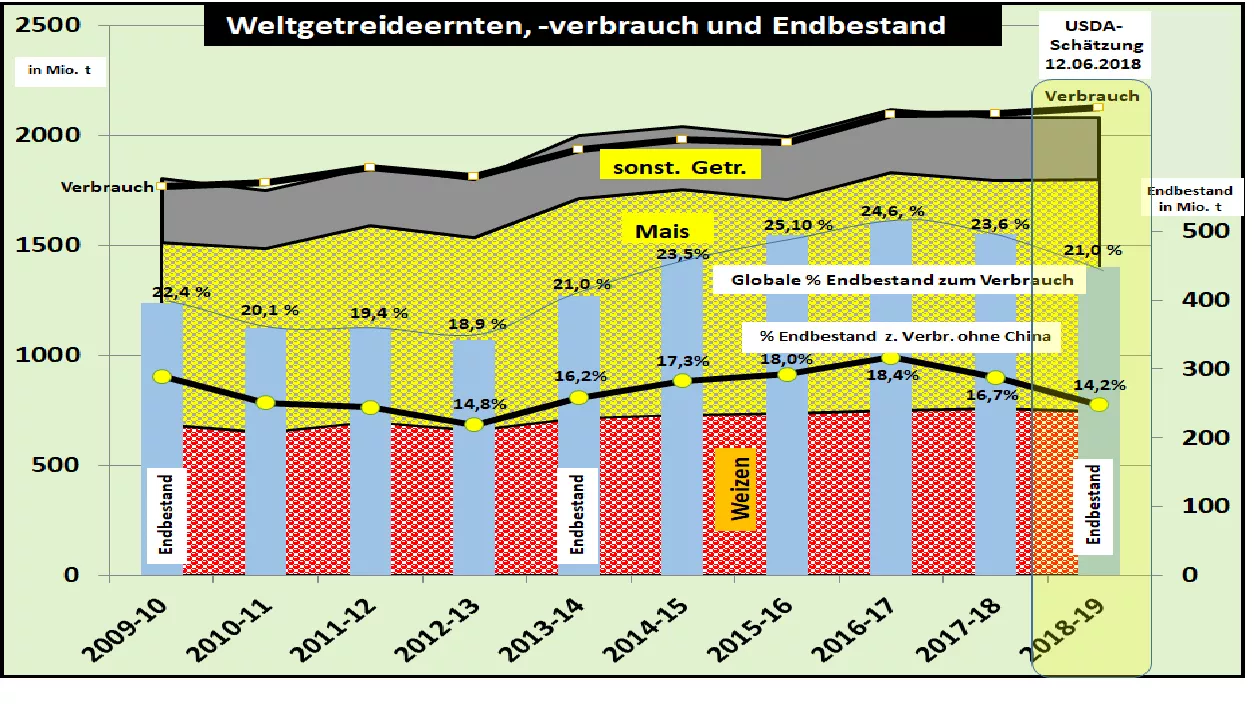

USDA estimates global grain supply as low as 2013/14 in 2018/19 The USA's second estimate of the global grain harvest in 2018/19 is slightly higher by + 0.4% yoy, but rising consumption by +1 , 34% leads to a significant reduction in inventories . According to the calculations of the USDA, only a 21% final stock will remain for consumption . This price-determining supply number is below the multi-year average of 22%. Experience has shown that rising international grain prices can be expected.If one dares a first preliminary comparison to the similar situation in 2013/14, the stock market prices in Paris would have to rise on an annual average of 195 € / t. Compared to the previous month's estimate, substantial cuts were made to the Russian wheat harvest , which reduced the USDA from 85 million t in the previous year to 68.50 million t . This rating is even lower than the latest estimates of the Russian market experts above the 70 million t mark. Comparatively low are the reductions for the EU wheat harvest with only 149 million t . The European Federation of Agricultural Cooperatives only a few days ago the EU wheat harvest estimated at 147.5 million t.In the case of global feed grain , the lower USDA month-on-month estimate is almost entirely due to the 9% lower harvest expectation in Russia. The global grain trade should go back only slightly. Exports and imports remain at the high level of the previous year of over 380 million t. Despite notable harvest losses, exports from Russia are expected to remain low. In return, the high Russian overlay stocks will be more than halved. There is hope for more export opportunities for EU exports if Russian export pressure at low prices is not quite as high.

Auffallend sind die wenigen Korrekturfälle der USDA-Schätzung zum Vormonat. Der Monat Juni ist allerdings noch ein frühes Stadium, um gesicherte Ergebnisse über die Ernte 2018/19 zu veröffentlichen. Bis auf nachweisbare Einzelfälle bleiben daher die Ertragsschätzungen im Bereich durchschnittlicher Trendentwicklungen. Die Juni-Schätzung des USDA ist daher als tendenzielle Orientierung zu verstehen. Im Vorliegenden Falle allerdings mit einer deutlichen Ansage einer knapper werdenden Weltgetreideversorgung mit der üblichen Folge anziehender Preise.

Bis zum tatsächlichen Ernteergebnis sind noch einige Risiken zu überstehen.

ZMP Live Expert Opinion

Despite all the reservations of an early estimate date, the tendency of a tighter global supply situation in the grain sector in 2018/19 can not be denied. The rear market prices show clear upward trends. But there are still some uncertainties and uncertainties to survive to sufficiently secured knowledge. The risks are distributed on both sides.