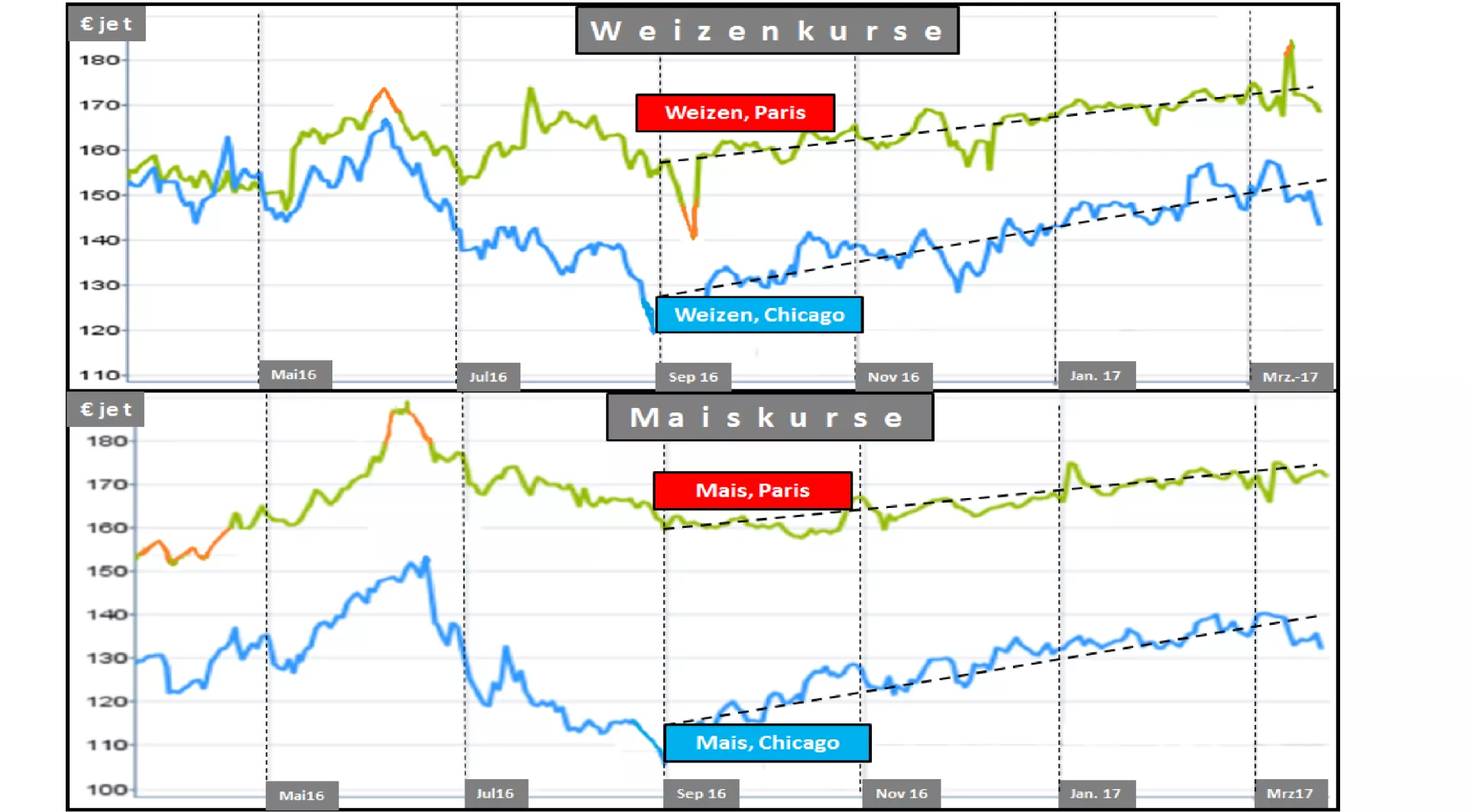

Cereals market: end of price increases for goods alterntige? After the harvest weakness showed from the start of the month September 2016 grain prices a tough average inflation. Of course there were up and down movements, but the basic orientation showed so far clearly upwards. You can search the grounds even in the pay of the storage costs, but the price upwellings must be supported also by the relative scarcity of supply / demand ratios here. For the EU market is 2016 with emphasis on wheat and corn to justify such scarcity due to the weak harvest. The inventories have been significantly scaled back despite significant reduction of exports, so that the supply situation is clearly more tense at the end of the year. The significantly larger compared to previous years difference between the stock prices on the Chicago Stock Exchange is typical of the development on the EU market . The cause is worldwide better able to supply that are expressed in the Chicago quotes. It is evident also that the Chicago price increases have become far more as quotations in Paris. The background is in the initially to highly-valued power layers which were considerably more closely evaluated with progressive course of the year as it under the unilateral impression of high crops was the case. Also the Aspect of China with the high proportion of global supplies but no availability for the other world market supply might have been noticeable. The adolescent upcoming harvests in the northern hemisphere have well survived the winter and thus dismantled part of the production risk. The forecasts go from good average results from and above-average power layers for the coming term. With the positive prospects for the new crop of inflation is clearly steamed. In the case of wheat , the new crops in the early threshing areas already pending in manageable 2 to 3 months. In the case of maize , high South American harvests on the course development press in the near future. It is therefore understandable that the Chicago show significantly more weakness as the Paris quotes quotes. As a course correction to be strong and long lasting is, will prove in the next few weeks and months. From today's perspective are the movement not very big to estimate, because still risk premium at the rate determination develop a stabilizing function. The experiences from previous years show that significant price changes can occur in the months of May to July , because this period is significantly important for yield. The amount of Flächenerträge per hectare is more important than the amount of acreage for the crop results

ZMP Live Expert Opinion

Possibly the year's previous price upturn at the end of the month March comes to an end. The new good average expectations of harvests are tours priced in the courses. However, the income decisive periods still ahead. Risks to price changes are therefore cannot be ruled out, even if much is assure stable rates from today's level of knowledge.