IGC forecast: best supply situation on the cereals market 2014/15 years

The International Grains Council (IGC) in London has again strongly increased its monthly June estimate of 2014/15 grain harvest over the previous month. The favorable weather conditions in most areas and the further prospects have led to this result. However, Nino weather anomaly to have noted, but without recognizable taking into account in the statistics found will be at the risk of an El.

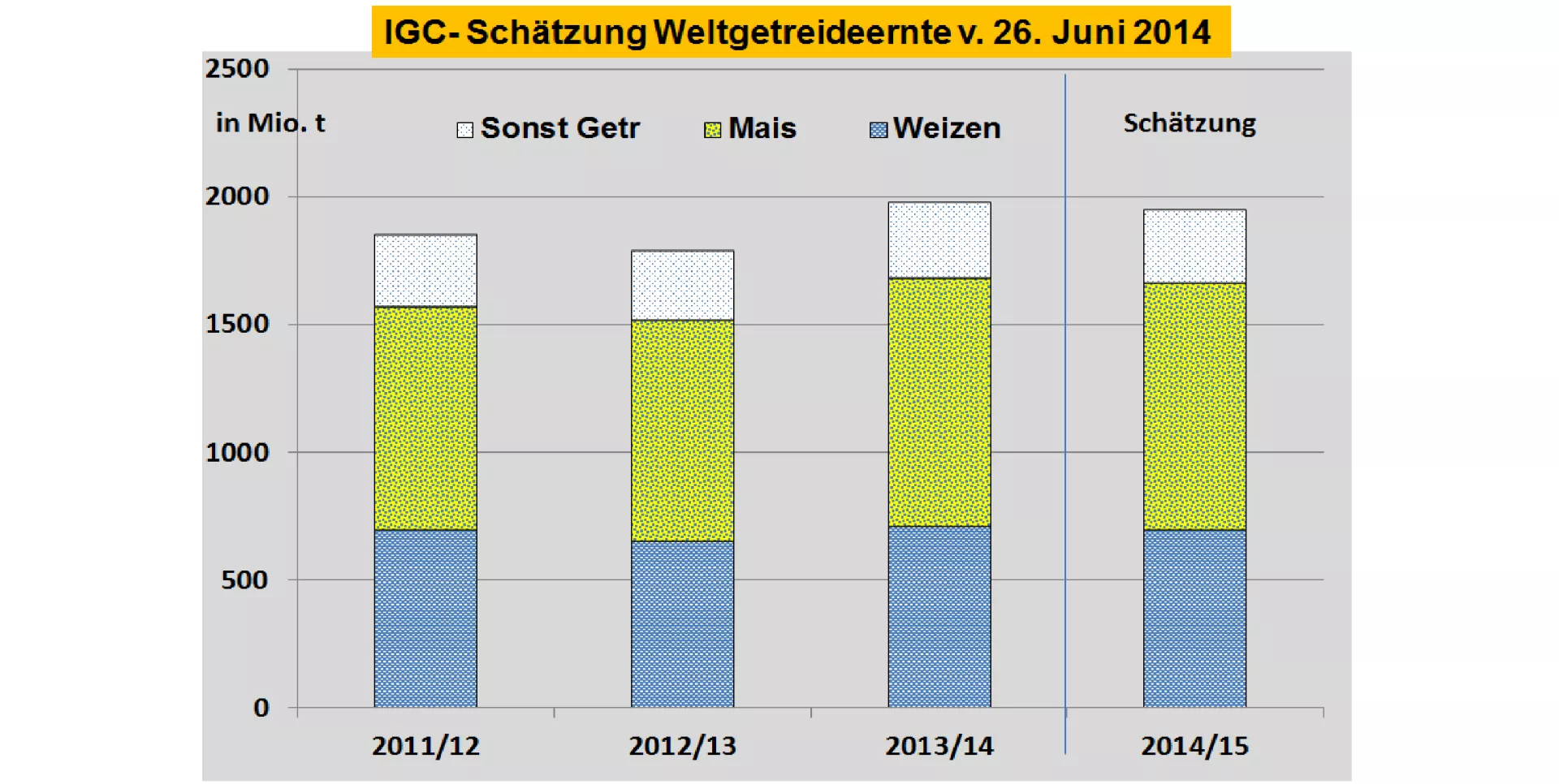

The world's grain harvest is to 1.95 billion. t (previous year 1.98 billion t) estimated. The consumption is expected to increase from 1.92 billion to 1.94 billion tons compared to the previous year. The accounting of care delivers a final inventory of 412 million tonnes and a "stock to use ratio" of above-average 21.3% (previous year 20.8%). A such high end stock gave it last in the year 2000/01.

The wheat harvest in 2014/15 increases the IGC to 699 million tonnes (previous year: 710) compared to the previous month estimate to about 5 million tonnes. The consumption is rated only slightly lower 697 million tonnes, so that a small restocking out.

The maize harvest in 2014/15 is considered lower than the record harvest of last year to 9 million tons, but 8 million tonnes higher than in the previous month's estimate. The closing stock no longer climb so to 180 million tonnes seen for years.

Good harvests are appreciated especially in the EU, China, India and Argentina. The IGC for Canada has made significant reductions after last year's bumper crop. The Australian harvest was already lower by the local Department of agriculture due to drought. The crop forecast by the IGC in Russia with 85 million tonnes differs significantly down compared to the other institutions of the treasure. The other Russia estimates are on 90 to 100 million tonnes.

The IGC because the necessary lead time for reporting has can not take into account the recent developments of the floods in the United States and first harvest results in the areas of early threshing.

On the stock market , publishing the IGC estimates raised little resonance. The prices move sideways level. Attention is focused on the USDA publications on next June 30 to the inventories and the official estimates of cultivation in the United States.

ZMP Live Expert Opinion

All diversity of crop estimates by various institutions, the expectation of a second crop emerged 2014/15 after the record results of the previous year. For the supply situation limits are calculated as a result of high initial stocks currently. However, half of the cereal stocks is in China, which will import 2014/15 much less grain this year. For the assessment of the supply, therefore the mobile end stocks of export-oriented States come in 1. Line into account. Mobile end stocks are significantly lower, but still in the good average range. On the stock markets move the grain prices on the Seitwärtslinie after a significant price downturn is preceded