Wheat continued to trend south on the Euronext/Matif in the last few trading days. The March date, which was quoted at EUR 300 last Friday, closed yesterday at EUR 291.25 per ton. The downward trend is thus continuing this week, only on one trading day, on Wednesday, were the wheat contracts in Paris able to end trading with a positive sign. CBoT wheat was only slightly weaker in the same period, with the start of today's premarket trading, wheat on the CBoT has even gained. In Europe and Germany, international competition in particular plays a role in price development. Lower prices in the Ukraine and Russia are still depressing the mood of local exporters. The momentum of European export volumes has also slowed down significantly. Although more quantities have been shipped to third countries over the past marketing year, the weekly quantities have recently fallen significantly. The euro is also regaining strength against the US dollar. At $1.0850, the common currency has recovered significantly since early December. On the local cash markets, prices for bread wheat and fodder wheat continued to fall.Trade has picked up speed again over the course of the week, more and more producers are showing their willingness to sell due to the falling prices and the feed mixers are also increasingly looking for grain again - although with regional differences. In southern Germany, buyers from Switzerland are also showing interest in wheat lots. The publication of the WASDE report by the US Department of Agriculture (USDA) triggered only minor price movements. Key points in the report were the increased winter wheat acreage in the US, up 11 percent year over year. In addition, global wheat production increased slightly compared to the December WASDE. The International Grains Council (IGC) in London comes to a similar conclusion. The experts there also slightly increased wheat production. What was particularly surprising here was the significantly better expectations for the Ukrainian grain harvest. There are significant differences in the WASDE report on the Russian harvest, which the USDA draws at 91 million tons, if their own Russian data had assumed a harvest of over 102 million tons.The fact that wheat prices were still able to increase yesterday and today on the CBoT is mainly due to the market's opinion of the growth conditions in the Great Plains. After the dry autumn and the snowstorms with a cold snap around Christmas, the stocks are currently lacking in soil moisture, it is said. In the slipstream of the falling wheat prices, corn also fell on the Euronext/Matif on a weekly basis. Due to the small EU harvest last summer/autumn, EU imports remain at a very high level and have not lost any momentum. Looking at the low turnover on the cash markets, the market supply seems to be sufficient at the moment. The fact that a good corn harvest is expected for Brazil is also putting pressure on the price structure. Agroconsult had recently increased the prospects for the first corn harvest that is now beginning there and, according to current estimates, the second corn harvest could also be better than in the previous year. In contrast to the local corn prices, the contracts on the CBoT increased significantly on a weekly basis. Even after the WASDE report was published yesterday evening, contracts were up in double digits.Both the USDA and the International Grains Council lowered their forecasts for global corn production. The USDA cut last fall's US harvest in particular because the yields per hectare were weaker. For Argentina, the ministry also cut costs and expects a corn harvest of 52 million tons (- 5.5 percent compared to the December WASDE). However, the USDA is more optimistic than the Argentine grain exchange in Rosario, which forecast a corn harvest of 45 million tons yesterday. The IGC cut its forecast for the global corn harvest to 1.161 billion tons and has thus revised the previous estimate downwards by 5 million tons.

ZMP Live Expert Opinion

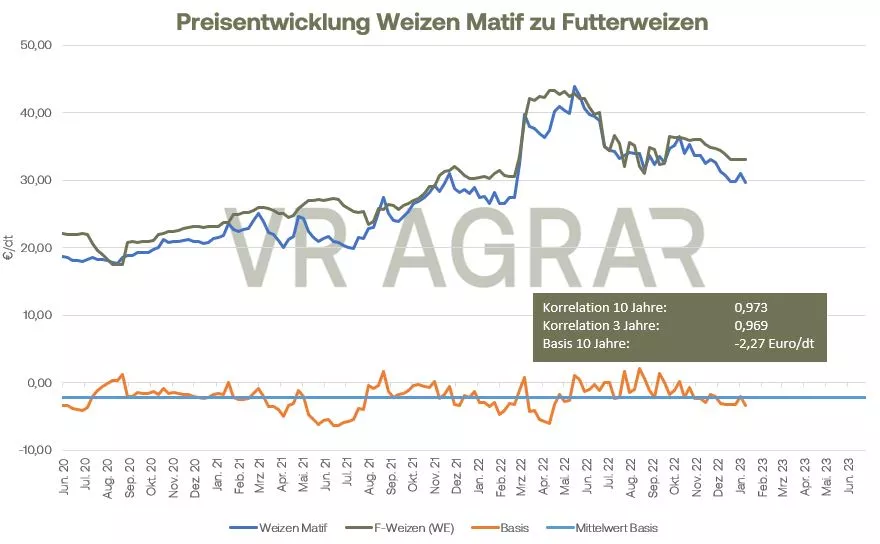

While the prices for corn and wheat on the CBoT show at least sideways to rising, prices in Europe are still on a downward trend due to the great international competition. There is a lack of impetus in this country, so that prices here continue to show a weaker trend.