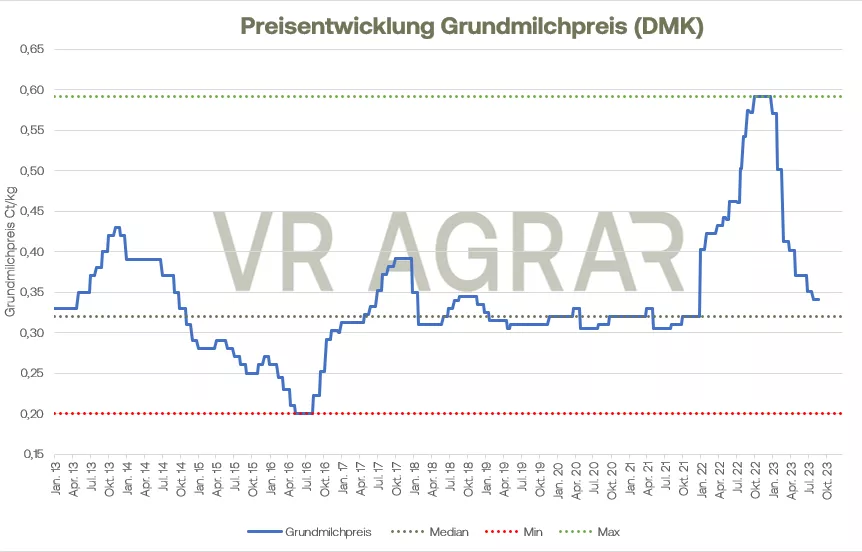

Compared to the previous week, around 1.9 percent less raw milk was delivered. This means that the usual seasonal trend has increased significantly. For the first time in over a year, the figure was below the same week last year, albeit only marginally by 0.1 percent. Overall, however, around 2.3 percent more milk was available to the dairies in the first 34 calendar weeks of this year than in the same period last year. The declining volume of milk and the declining components of the delivered quantities caused a tighter supply on the raw material markets. Skimmed milk concentrate increased noticeably and cream also became significantly more expensive. On the spot market, the federal average quotations also rose. For the 35th calendar week, the ife Institute gives a value of 39.9 cents/kg, which is 2.9 cents more. There was also brisk demand for molded butter at the beginning of September, which was above the usual seasonal level. The dairies are also noticing slightly firmer prices again. On the butter and cheese exchange in Kempten, the price was raised by 5 cents at the upper end of the trading range.Bockbutter's business continues to be quiet, with new business only occurring here and there. Nevertheless, the prices in Kempten were able to increase by 11 cents to 4.35 to 4.56 euros/kg at the upper end of the trading range. Export volumes continue to be disappointing, European goods continue to lack competitiveness, even though butter prices rose again in the Global Dairy Trade Tender in New Zealand for the first time in four sessions. There are slightly firmer trends on the EEX, especially for the early delivery dates. Recently, more contracts were traded again on the Leipzig stock exchange. Cheese continues to be in high demand. The high number of requests and inquiries continues with the turn of the month. In particular, sales to food retailers remain at a high level; large consumers, industry and restaurants are primarily using agreed quantities from existing contracts. There is also still a lot of business going on in southern European holiday regions, and there is also a further upturn in business in third countries. Overall, the input and output of the ripening warehouses are somewhat more balanced again.Overall, however, the stocks in the warehouses remain below average in terms of quantity and age for this time of year. The quotations in Hanover remained unchanged this week, in Kempten some increases were observed. The powder markets remain unchanged. Business development for skimmed milk powder has been quiet and demand has not picked up even with the end of the summer holidays in the last few federal states. In some cases, new contracts were concluded. There is also subdued demand from the Asian region; many exporters would have expected more from business in China in particular. Both existing goods and fresh quantities are currently offered. The trading range is therefore expanding, but yesterday's quotation went south by an average of 50 euros per ton. On the EEX, prices were able to strengthen slightly in the earlier dates despite lower turnover compared to the previous week. In the Global Dairy Trade Tender, prices for skimmed milk powder fell again, which further limited local competitiveness. There is hardly any change in whole milk powder .European industrial customers in particular show little need; manufacturers are primarily receiving inquiries for the end of the year and the beginning of 2024. When it comes to whey powder, however, there is strong demand for animal feed qualities. But demand for food grades was also somewhat more lively again, although trading volumes remain manageable. .

ZMP Live Expert Opinion

Although the holidays are over, the market doesn't want to start in full yet. Powder and block butter are still in demand, while molded butter and cheese are literally being torn from people's hands. Prices are stabilizing. Overall, there are signs of further sideways movement with a slight upward trend.