Short-term prospects on the milk market in 2015

The plummeting milk prices 2015 extends already over an unusually long period of time. In the spring was the big hope is that after overcoming the height of delivery in the early summer months to may including the seasonal decline in the months of June and July to offer relief could contribute to the northern hemisphere. So far has not a resounding success.

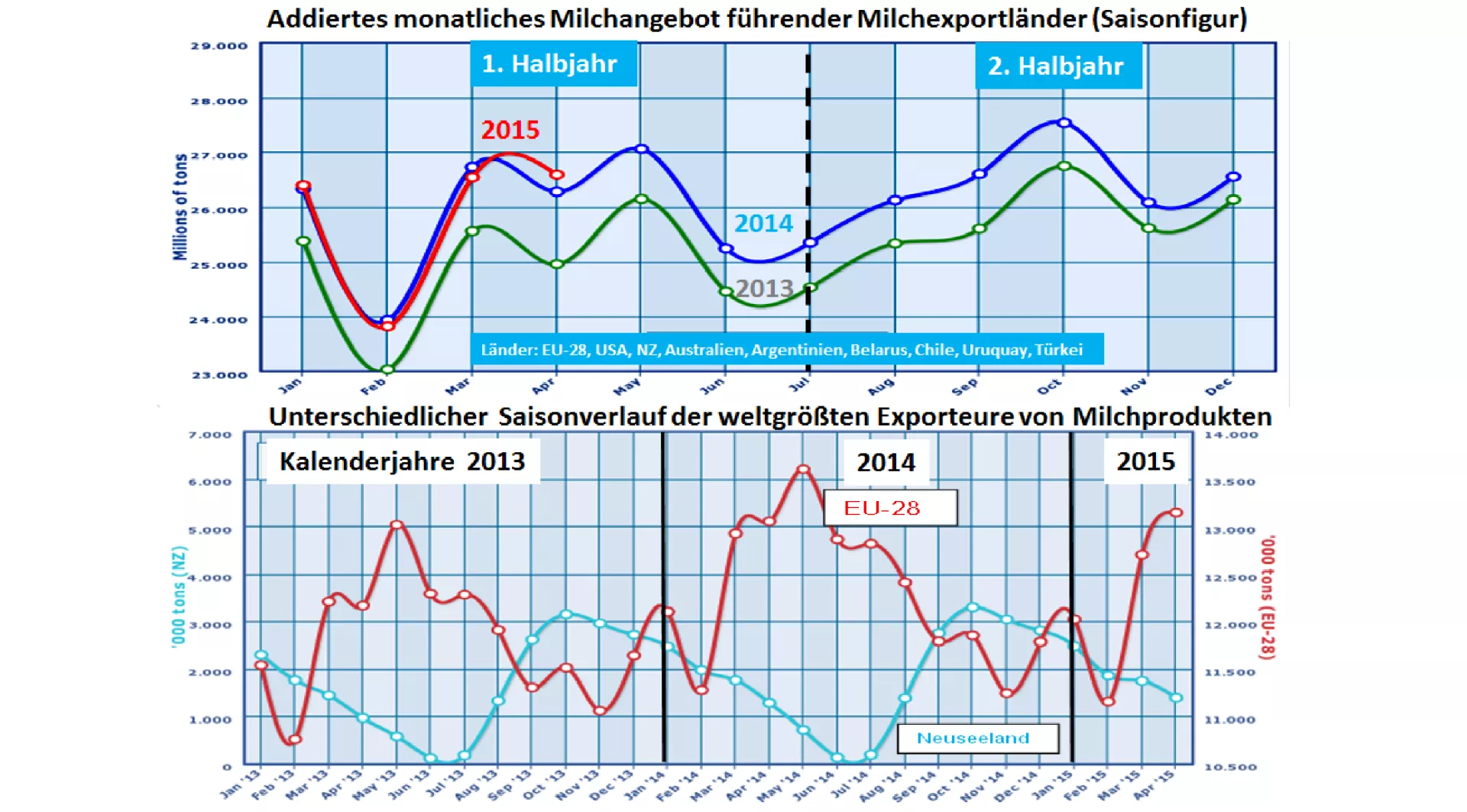

The typical course of the milk delivery under transfer of opposing developments on the northern and southern hemisphere major exporting countries shows in the first half of a delivery volume of the annual average. The exception is the month of February with its 28 days.

With beginning of June begins a 3-month period decreased delivery volumes with the low point in June. The main reasons are the production decline in the southern hemisphere due to dwindling generation of feed and the dry position of whole herds in the neighbourhood of zero. In the northern hemisphere the lactation curve of the cows is also down. But more is a feed-based milk production under Stallhaltungs conditions, the effect of this summer is lower.

While on the northern hemisphere which continuously decreases amount of milk delivery, the production from the month of August in the southern hemisphere countries rising vigorously to. The climax is reached in the Oct.

One netted both areas, it comes only in the months of Sept Oct to an autumn offer high, the supply curve has again in the remaining remaining months.

The basic course of this milk delivery can be observed every year. The compensation of amounts of via milk powder production and storage, cream freezing to the blending of soft summer with hard winter fat, as well as increased cheese production and ripening. The extent of fluctuations is different every year.

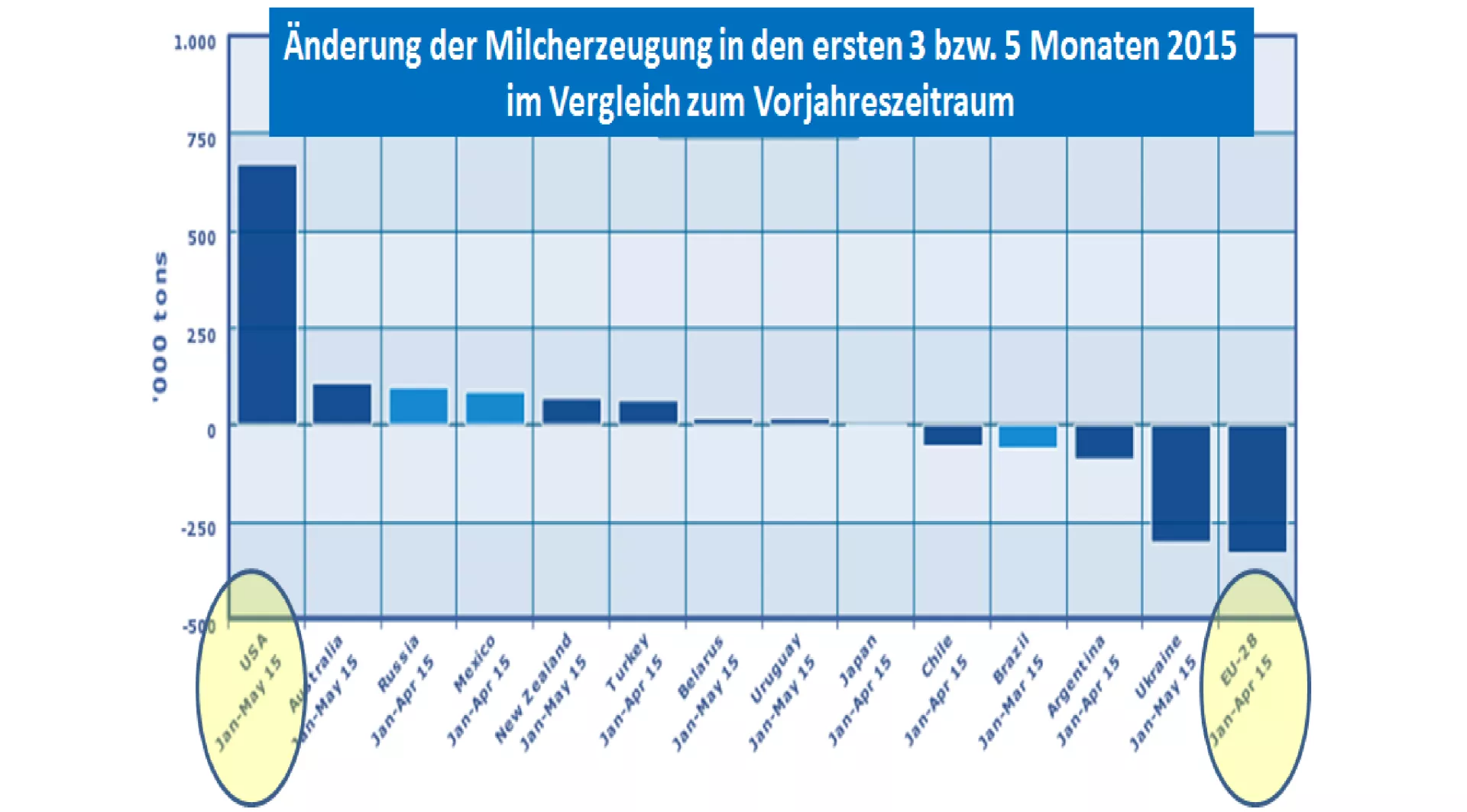

The added production quantities at world level to the high level of the previous year line moves in the present year 2015 have been in the first half of the year . The April figures were due to the high U.S. deliveries again about. The feared increase in supply for the expiry of the EU milk quota has remained so far. Low prices, falling cow numbers and the recent food shortages as a result of the rainfall deficits are likely to be the decisive factors.

Stop after the current assessment the food shortage for the autumn / winter period is in large parts of the EU. The grass growth and partly the maize stock look like little promising. The milk-feed price ratio does not necessarily animates to milk performance.

From the world's largest export region in New Zealand is known because the cow slaughter and Heifer rearing figures that the cow number for the first time after almost 2 decades was already reduced to 0.5%. The converted 25 ct / kg milk prices are no reason to increase milk production. El Niño year 2015/16 is known that possibly longer dry spells in the middle of the peak of milk production reduce the feed generation. Because it will hardly force feeding, the milk yield will fall. The first estimates suggest a decline in the New Zealand milk production by 1 million t or 5% off.

However, that deliver (via) ample rainfall in the United States a cheap basic food supply. While the European milk production has fallen below last year's level, is the US milk deliveries significantly above the production line by 2014. The United States stand at 3 to 5 point of exports of dairy products. The focus is skimmed-milk powder, while they are hardly on the milk powder market.

The prospects for the autumn/winter of 2015/16 tell of supply-side of developments quite entlastender a number. The great unknown is China's State-controlled import behavior. A modest increase in economic growth slows consumption. Chinese food supplies are explained to the State secret. The accumulated stocks of milk powder are yet how much, to ensure the security of supply still remains unclear.

On a return of Russian imports may following the recent decisions to continue the import bans not count.

The rapid increase of in milk prices in 2009 seems for the time being not to repeat itself. A slow, but stable price improvement is driven by justifiable prospects.