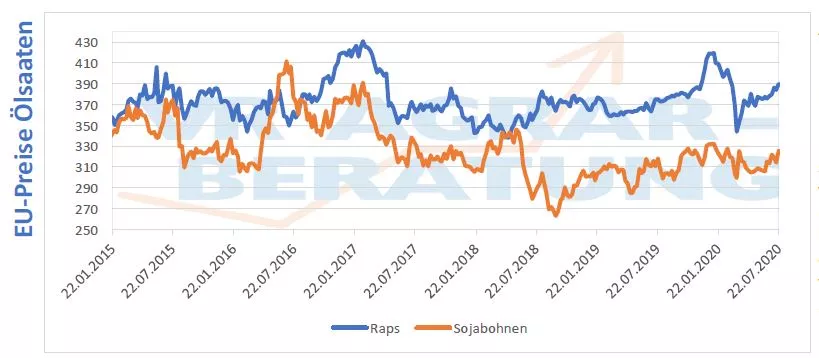

After the rap prices ended in the red area last week, the prices recovered during the trading week and recorded slight gains except for September. Support came above all from the downward revised harvest forecast for the entire EU harvest. The lowest harvest of 15.4 million t is now expected in 14 years. In France, harvesting work is in full swing. So far, 3.4 million tons have been threshed. Harvesting work is also progressing rapidly in Germany and Poland and is already well advanced regionally. Results to date show average hectare yields of 3.4 t and thus exceed the hectare yields from last year. At around 3.2 million tons, the harvest quantities in Germany will be significantly higher than in the previous year. The expansion of the area to 953,000 hectares is primarily responsible for this. Nevertheless, the traces of the drought can still be seen here and in many places the plants lacked water and insect damage contributed to the plant development. With the start of the stock exchange on Friday, the rap contracts are listed at a slight discount.

The soybean complex was in the green at the beginning of the new week and also ended the penultimate day of trading with profits. However, the new NASS report with the significantly improved plant populations and the optimal growth conditions continue to put prices under pressure. In addition, the expanded acreage in Brazil is fueling concerns that there may be an oversupply. The continuing political tensions between the USA and China had a limiting effect on the price increase. Support provided prices with good global demand. However, exports were smaller than expected and amounted to 260,000 t. In contrast, export bookings exceeded traders' expectations and were almost ten times higher than at the same time last year.

Good soybeans continue to grow

ZMP Live Expert Opinion

With regard to the advancing harvesting of rapeseed, average yields are emerging for Germany, but these cannot compensate for the under-harvest of the rest of the EU. A harvest pressure on the Matif is currently not discernible, but the further the harvest progresses, it will show which tendency the oilseed will take in principle. In the soybean complex, the good harvest prospects are putting pressure on prices. August is particularly important for plant development and will show whether the harvest forecasts are likely to prove true.

ZMP Market Report Compact

Latest news from the markets, in compact for you

15.

03.24

11:22

IGC estimates 2024/25 soybean crop

Market Report Compact

14.

03.24

14:32

DRV estimates the 2024 rapeseed harvest to be lower than last year

Market Report Compact

09.

03.24

12:34

USDA updates global oilseed market

Market Report Compact