USDA bulletin oilseed markets, rising crude oil prices - falling rates of euro

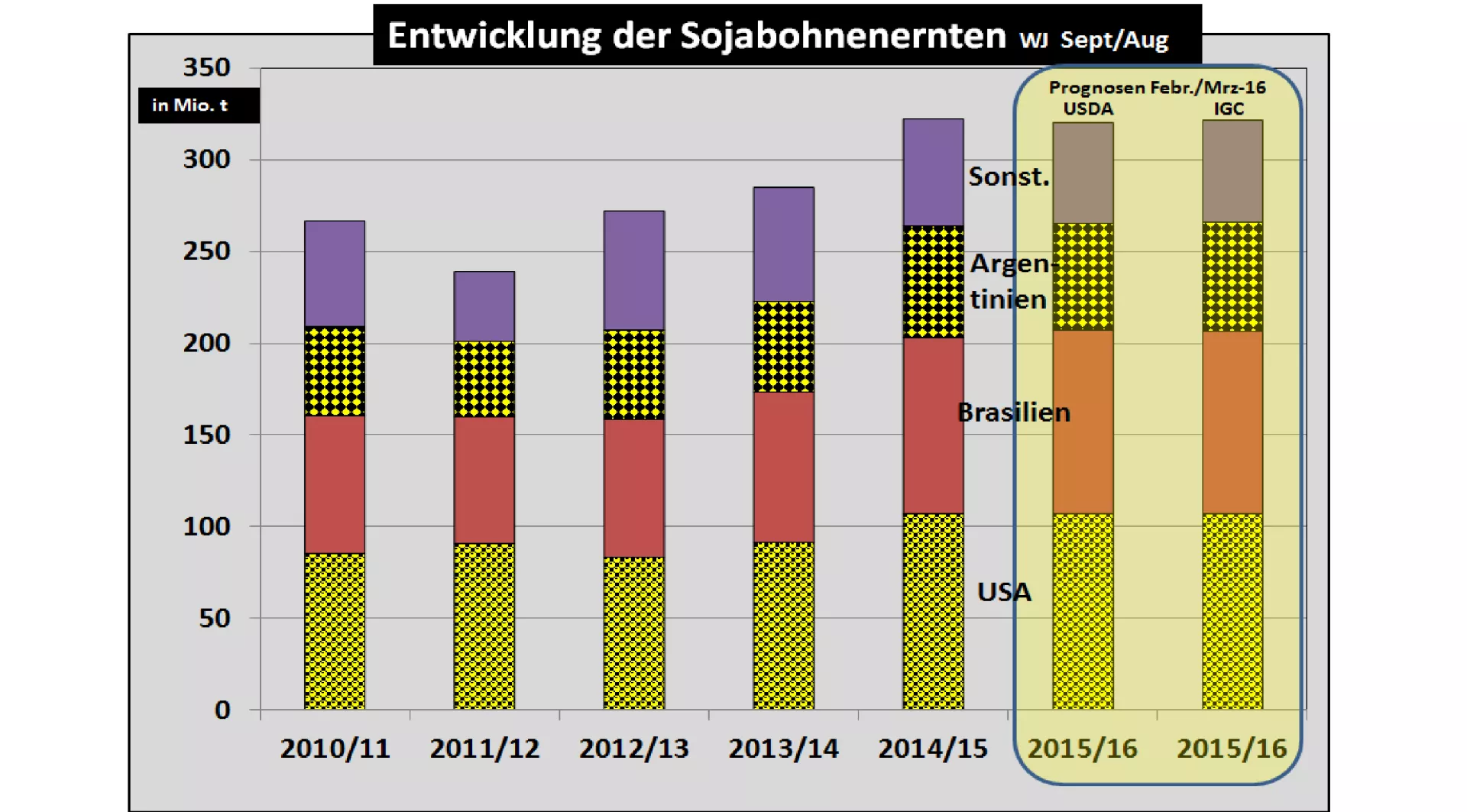

The global oilseed production has been corrected by the U.S. Department of agriculture (USDA) for the umpteenth time down. With 526,9 million metric tons, the result is around 8 million tonnes in the previous year by 2015/16. The soy market, which is estimated at only 320 million tonnes is instrumental in the development. In the case of the canola market, the world's scarce situation remains with a below-average harvest volume of 67.5 million tonnes.

The USDA estimates a rising to nearly 9 million tons increase in processing on the usage page . Contributes to this the soy bean with 16 million tonnes, while in other oilseeds the consumption quantities easily go back. Crucial contribution to the increase in the soybean sector comes to the countries Argentina and China together 10 million tonnes.

On the export side is Brazil with an increase of exports by 50 to 58 million tons in appearance. After the release of the currency and easing the export control the export volumes substantially increasing expectations for Argentina, meet only to a small part. The USDA is only by an increase of 1 million tonnes of beans, 4 million tons for the soybean meal and 0.5 million tonnes in the soybean oil.

On the import side is dominated by the Chinese imports with an increased estimate to 82 million. t soy beans. The number from China not entirely achieve 83 million tonnes. After all, this means an annual increase of 4 million tonnes, which corresponds to the multi-annual average.

The closing stock at the oilseeds will go back according to the calculations of the USDA, but remain still at a comparatively high level.

The palm oil market is estimated on the production side to last year's level. In the two major production regions of Indonesia and Malaysia with a share of over 80%, the dryness of the El Niño weather has prevented a rise in output. Palm oil exports from these countries remain narrowly on same line. The closing stock in Malaysia shall be reduced significantly.

The recent development of the rising crude oil prices and the falling euro exchange rate (EU rate is 0 %!) is the rape and soybean meal prices reflected in.)

An escalating price increase is expected when the rape. Higher crude oil prices take the pressure off of the rapeseed oil prices and more expensive due to the euro rate increasing EU rapeseed imports raise the domestic price once again.

The period of 2 months of 540 on $613 / t higher palm oil prices the courses support in the field of vegetable oils. The more or less stable soybean oil prices to the tune of $660 per t further development could dampen a little.

A clearly defined price travel shows in the soy complex down. The current listings with tentative course improvements prove more stable side.

ZMP Live Expert Opinion

Several signs suggest that the previously continuous drop of in oilseed prices has bottomed out of a lower level. However, a rapid upward movement in the face of high amounts of soy is not expected to. A certain stabilization on slightly elevated level could be the direction. But: the crude oil and euro rates stay as stable?