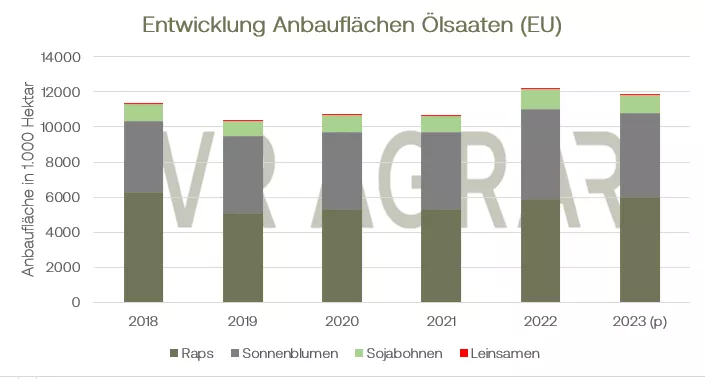

Oilseed rape regained some ground this week and this week bounced back significantly from losses earlier in the month, albeit far from fully recouping losses. Noted the front month of May on March 1st. still at EUR 528.50 per tonne, it was EUR 466.75 per tonne by the closing bell on March 30th. At the start of trading on Friday, green signs are showing again. Little rapeseed is still being traded on the spot markets, but prices in Hamburg and Straubingen, for example, but also on the Mittelland Canal, increased by more than 40 euros in a week-on-week comparison. In the "Short Term Outlook" published yesterday for the agricultural markets this year, the EU Commission is assuming a significant increase in oilseed production overall. A record production of 33.6 million tons is expected. The commission believes that the sunflower harvest in particular should increase significantly and increase by a significant 18 percent to 10.9 million tons compared to the previous year. It should be noted, however, that this assumes a normal growth season with appropriate weather conditions. In the previous week, the grain trade association Coceral had already forecast an increase in EU oilseed production.The European association expects rapeseed production of 19.86 million tons, slightly more than in the previous year, for the 2023 sunflower harvest Coreal expects a quantity of 11.23 million tons compared to 9.34 million tons in the previous year. According to both the EU Commission and Coreal, the European soybean harvest should increase. According to data from the Federal Office for Agriculture, the processing of oilseeds in Germany fell in the first half of the current marketing year. Around 5% less rapeseed was processed in the oil mills. Other oilseeds also fell significantly compared to the first half of the 2021/22 season. By March 26, 2023 (39th calendar week of the current marketing year), 6.18 million tons of rapeseed were imported into the EU-27. That is 2.28 million tons more than in the same calendar week of the previous year and the overall result of the previous financial year has already been exceeded. In particular, the good delivery capacity of the Ukraine plays into the figures here, but recently more volumes have come from Australia after the harvest there has ended. The Canadian market participants are also happy about good export figures.Canola was up this week, although yesterday saw a slight correction on the ICE Winnipeg scoreboard. The soybean market showed around the mark growth on a weekly basis. Overall, however, the soy complex remains volatile. The majority of market participants were satisfied with the latest US export figures and, as has been the case since Christmas, news from Argentina has caused ups and downs at the CBoT again and again. For the next few days, very heavy rainfall has been reported for the most important growing areas in Argentina. The grain exchange in Rosario has therefore already declared the drought in the South American country to be over. The grain exchange in Buenos Aires left its production forecast at 25 million tons unchanged from the previous week. If this forecast is correct, the harvest would be halved compared to the original production expectation. Today, Friday, the US Department of Agriculture will publish renewed estimates of acreage in the US. The market analysts assume that the soybean acreage will increase slightly compared to the last estimate as well as compared to the previous year.The soy complex received fundamental support from the calming financial markets. Crude oil was also able to gain significantly in these last trading days, especially at the beginning of the week, and thus gave soybeans support. Soybean meal at the CBoT also gained slightly over the course of the week. At the closing bell on Thursday, the leading May date closed at $459.90/short ton. Last week on Thursday the settlement was still at 451.60 US dollars ton. On the local cash markets, soybean meal generally developed slightly weaker, but the prices did not point in a completely uniform direction. Rapeseed meal is quoted unchanged in Hamburg for the week, on the Lower Rhine rapeseed meal prices went slightly south.

ZMP Live Expert Opinion

Rapeseed was able to overcome the strong downward trend and grow again, despite the good prospects for the 2023 European harvest and the still very high oilseed imports into the EU. We will know in the coming week how extensive the announced precipitation will actually be in Argentina. However, these rain showers will probably do little to change the country's fundamentally gloomy production prospects. The oilseed markets continue to promise volatility but also tension.