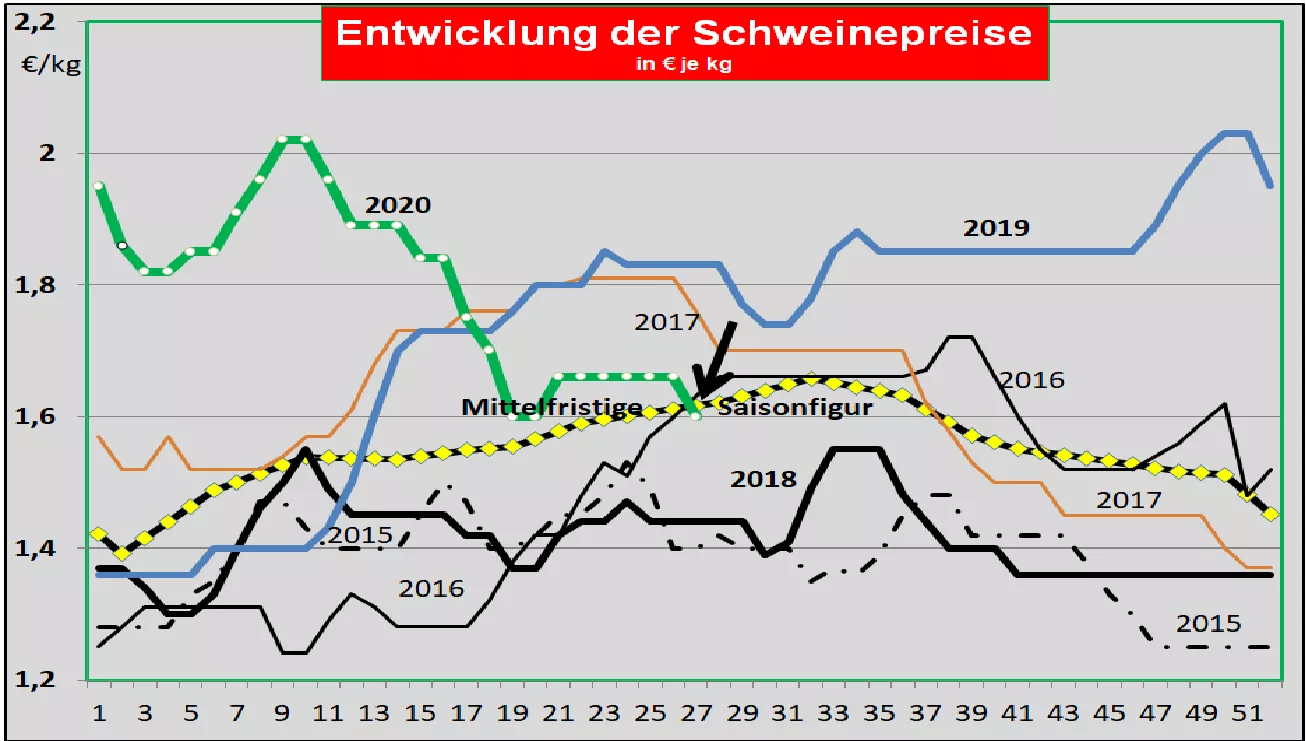

Pork market: Tönnies slaughterhouse still too - 80,000 pigs on hold Germany: The number of slaughter in the previous week fell to 784,765 mainly due to limited slaughter capacity. The slaughter weights remained at 97.0 kg. When reselling the sections to food retailers, processors and for export, the prices remained unchanged on average over the past week. Only the neck was rated +2 ct / kg higher. The V prices have been several weeks below the average compared to the average resale price of the sections. Pre-registrations for the current week, at 263,120, are 14% higher than in the previous weeks. These can include deferred and early games. The V-price for the 27./28. KW 2020 is set lower at € 1.60 / kg (-6 ct / kg). The range extends from 1.58 to 1.66 € / kg.The third country business suffers from the Chinese import ban on pork from several German and European suppliers. One should not lose sight of the ASP danger. Market and price development in selected competing countries: Denmark has lowered pig prices by 4 ct / kg for the current week. A further drop in prices is expected for the coming week. In Belgium , the lack of live exports to Germany cause sales problems. The prices were reduced by -4 ct / kg. Netherlands: Uncertainty is great given the Tönnies slaughterhouse closure. Depending on how affected the slaughterhouses were, the price was reduced from zero to -14 ct / kg. A well-balanced market is reported in France . The carcass weights have dropped by 3 kg in the past few weeks. Demand remains moderate.Prices remain stable, mostly stable. A brisk demand is reported in Italy , which is favored by the increasing number of holidaymakers. At the same time, the domestic supply is relatively small due to the lack of quantities and falling slaughter weights. Imports from Germany are also low. The prices continue to rise. In Spain , the supply is low due to small quantities and falling slaughter weights. The tourism-related growing demand cannot be met in every case. The export volumes with a focus on China were reset by cancellations. However, the living quotes show further upward tendencies. In the United States , producer prices are around € 0.56 / kg. According to the latest cattle counts, the number of pigs ready for slaughter is 7% above the previous year. The backwater is said to affect 1 million animals. On the other hand, the inventories in the cold stores and department stores are at 75% of the previous year's levels. The replenishment from the fine cutting is missing.The China business benefits from the primarily roughly disassembled sections. In Brazil , the converted prices fell to € 0.99 / kg. The decisive factor was the sharp decline in the Brazilian currency. Restrictions caused by the Covid 19 pandemic, particularly in the southern provinces, are said to have been removed. Not least, exports benefit from the weak real. China: Prices have recovered to € 5.35 / kg on average. Production is expected to be an additional 7.5% lower this year. After the Covid pandemic has been overcome, demand will rise again. Other types of meat and protein carriers such as fish and milk only partially compensate for the deficit in pork. Imports will peak this year. The U.S. Department of Agriculture is not expecting self-sufficiency to increase again until 2021.

ZMP Live Expert Opinion

With the increasing duration of the reduced slaughter capacities due to corona, the bottleneck in the life business increases with the consequence of increasing price pressure. In contrast, the meat shops remain stable. In view of a seasonally low supply, but growing demand, if there is a return to larger slaughter capacities, there is a reasonable expectation of stable to rising prices again.