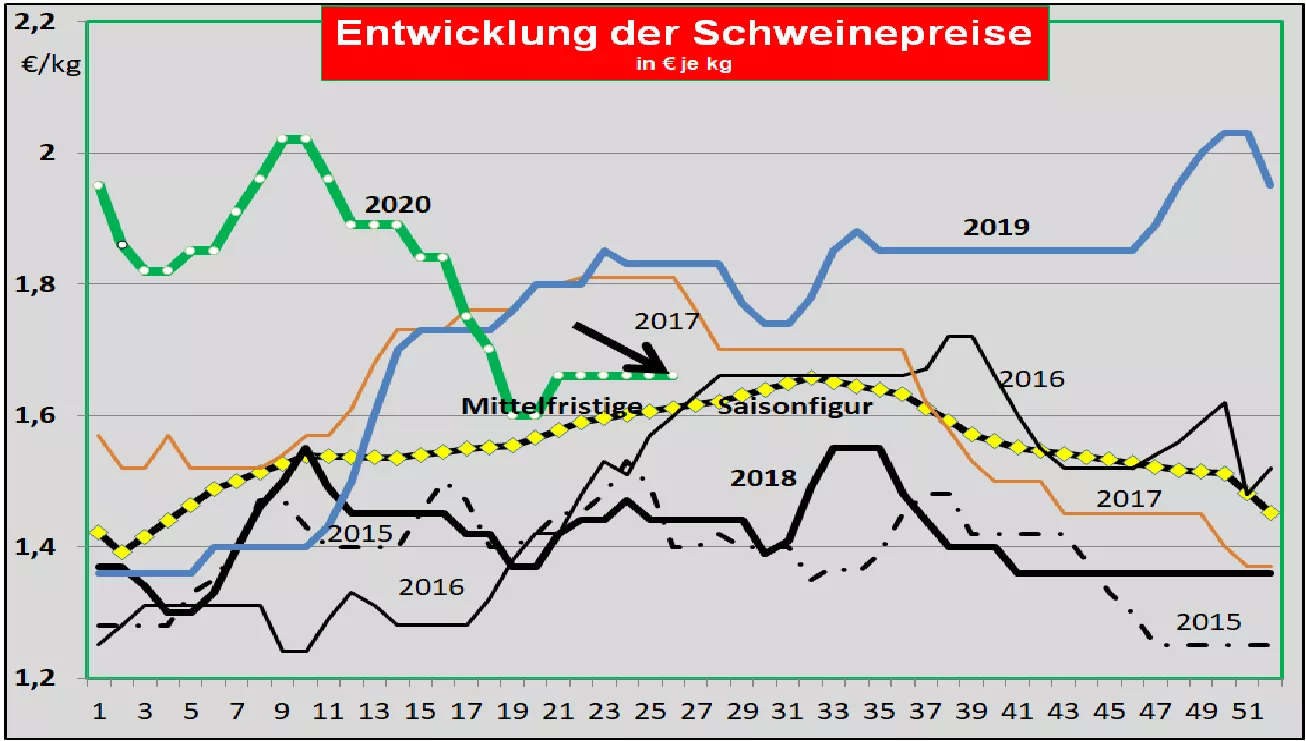

Pork market: Tönnies slaughterhouse closed for the time being. Germany: The number of slaughters in the previous week remained at a seasonally low average of 848,116. The slaughter weights remained at 97.0 kg. When the parts were resold to food retailers, processors and for export, the prices were increased on average by 2 ct / kg in the last week. Cutlet (+4 ct / kg), shoulder and neck were rated higher by +2 ct / kg. An attractive grill heel is noticeable. Pre-registrations for the current week are 5% higher at 238,800. The initially 2-week closure of the Tönnies slaughterhouse in the Gütersloh district affects approx. 140,000 pigs a week. In principle, redistribution to other slaughterhouses is possible, but costs. The uncertain duration of the closure creates uncertainty. The V price for the 26th / 27th KW 2020 will remain unchanged at € 1.66 / kg .It is still open whether this price can be maintained under the given circumstances. The third country business is suffering from the Chinese import ban on pork from supplier Tönnies. The ASP danger remains. Domestic pigs are affected in Poland. Market and price development in selected competing countries: Denmark has kept pig prices unchanged for the current week. Stable prices are also expected for the coming week. In Belgium , the lack of live exports to Germany cause sales problems. The prices range from unchanged to yielding. Netherlands: Uncertainty is great given the Tönnies slaughterhouse closure. Nevertheless, prices are expected to remain largely stable. The German effects are hardly noticeable in France .The increasing demand for barbecues ensures brisk sales. Falling slaughter weights ensure a well cleared market. Prices remain stable with a slight upward trend. The offer from Italy and abroad is declining in Italy . At the same time, demand is increasing. Rising tourist numbers are boosting sales. The prices continue to rise. In Spain T he live offer goes back noticeably less slaughter rate and lower slaughter weights. Demand is picking up rapidly. The export volumes with a focus on China have stalled. The living quotes show further upward tendencies. In the United States , average producer prices fell further to € 0.55 / kg . The pent-up live offer puts the limited slaughter capacity in distress. On the other hand, the inventories in the cold stores and department stores are at 75% of the previous year's levels. The replenishment from the fine cutting is missing.The China business benefits from the primarily roughly disassembled sections. In Brazil , the converted prices rose to 1.05. The strong exchange rate was largely responsible for this. Disabilities from the Covid 19 pandemic are particularly prevalent in the southern provinces. However, export prices are under pressure from US competition and Chinese prices are no longer so high. China: Prices have recovered to an average of € 5.12 / kg . After the Covid pandemic has been overcome, demand will rise again. Other types of meat and protein carriers such as fish and milk only partially compensate for the deficit in pork. Imports will peak this year. The U.S. Department of Agriculture expects sufficient self-sufficiency in 2029. The most recent analysis by the U.S. Department of Agriculture (USDA) on current and future developments in the pork sector assumes that pork production will recover by 2021 after the slump in the second quarter of 2020.However, the pig prices should remain below the line of the equivalent of 1 € / kg. Exports to China should only increase moderately.

ZMP Live Expert Opinion

So far, little pressure from the closure of the Tönnies slaughterhouse; Uncertainty arises from the uncertain length of time the slaughterhouse is closed.