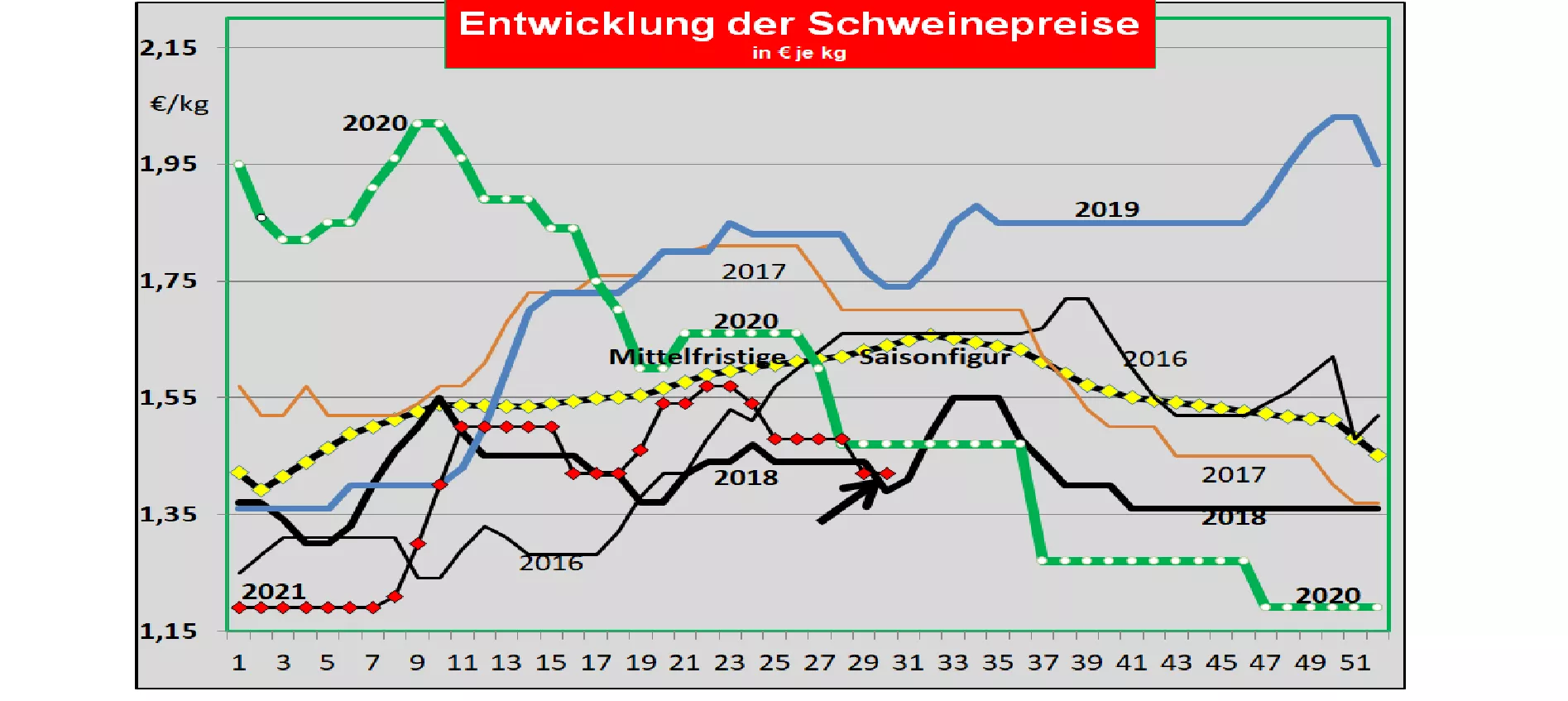

Germany: prices narrowed to 1.42 € / kg without a margin - live supply somewhat larger The weekly slaughter numbers rose again to 801,086 (previous week 784,896 ), as did the slaughter weights with 96.3 kg (+0.2 kg). The pre-registrations have increased with 243,000 pigs (previous week 210,700), but remain at a level that is far below average. When reselling the pieces to food retailers, processors and for export, the average prices were reduced by a further -4 ct / kg. The ham alone gave way by -5 ct / kg. In the last 5 weeks, the decrease in the price of the cuts totaled - 22 ct / kg . At the ISN auction on Tuesday, July 20th came with an offer of 1.685 pigs a price of 1.44 € / kg (-3 ct / kg for the pre-auction). There was a protrusion of 38% The V-price for the period from July 22nd. until July 28th , 2021 will remain unchanged at 1.42 € / kg The range was reduced to 1.42 to 1.42 € / kg. As of July 20, 2021, 1,619 wild boars infected with ASF have been officially confirmed in Brandenburg and Saxony. Domestic pigs are affected for the first time. The pigs that tested positive come from an organic sow farm with 200 animals in the Spree-Neisse district and two small farms with 2 or 4 pigs in the Märkisch-Oderland district. The farms are located near the Polish border in existing restricted areas (see attached map). Market and price development in selected competing countries: In Denmark the prices are in the 29thKW 2021 has been reduced between 5 to 6 ct / kg . Exports of meat and pigs for slaughter have declined. In Belgium the prices in KW 29 remained unchanged at the low level of 1.25 € / kg. If domestic sales are balanced, exports remain unsatisfactory. Netherlands: In the majority of the slaughterhouses were reduced by 5 ct / kg in the 29th week. In France , prices in Brittany fell by -3 ct / kg to just under € 1.35 / kg . Due to the holiday, the number of slaughtered pigs fell to 307,771 pigs, but with a slaughter weight of 94.8 kg. In Italy , the prices were increased by +1 ct / kg in the 29th week. There are signs of stabilization at a low level. In Spain the prices were again reduced by -5 ct / kg in the 29th week.The price drop in one month adds up to around 20 ct / kg and is the equivalent of less than 1.80 € / kg. In the USA , prices in IOWA have fallen to € 2.06 / kg . The quotes for the new front month of Aug on the Chicago Stock Exchange fall to 1.95 € / kg . The supply from ongoing slaughter increases and is sufficient for the grill demand . For the autumn / winter months, the forward rates are below € 1.60 / kg. In terms of exports, the decline in deliveries to China is offset by increasing exports to Mexico, Japan, the Philippines and South America. Brazil: After a previous decline, producer prices have stabilized further at € 1.39 / kg. The decisive factor are the increases in domestic currency.The supply, which is no longer so urgent, is sufficient for subdued domestic demand and subdued exports. China: The latest prices have risen again to the equivalent of € 2.77 / kg. For Sep-2021 , futures prices of € 3.30 / kg are already being traded on the Dalian Stock Exchange. The rebuilding of the pig population is proceeding more slowly than planned. High piglet and feed prices put the brakes on. Conclusion: slightly increasing slaughter numbers and advance registrations gave sufficient reason to fix producer prices at a low level in the difficult meat sales situation. Sales in the meat business remain difficult, more in the north than in the south. ASP in domestic pigs creates uncertainty.

ZMP Live Expert Opinion

A persistent live supply at a low level is not enough to alleviate the supply pressure for meat in the EU internal market. The reduced exports from China, Denmark and Holland are leading to higher quantities of meat in this country and putting prices under pressure. The ASF cases in domestic pigs unnecessarily lead to uncertainty.