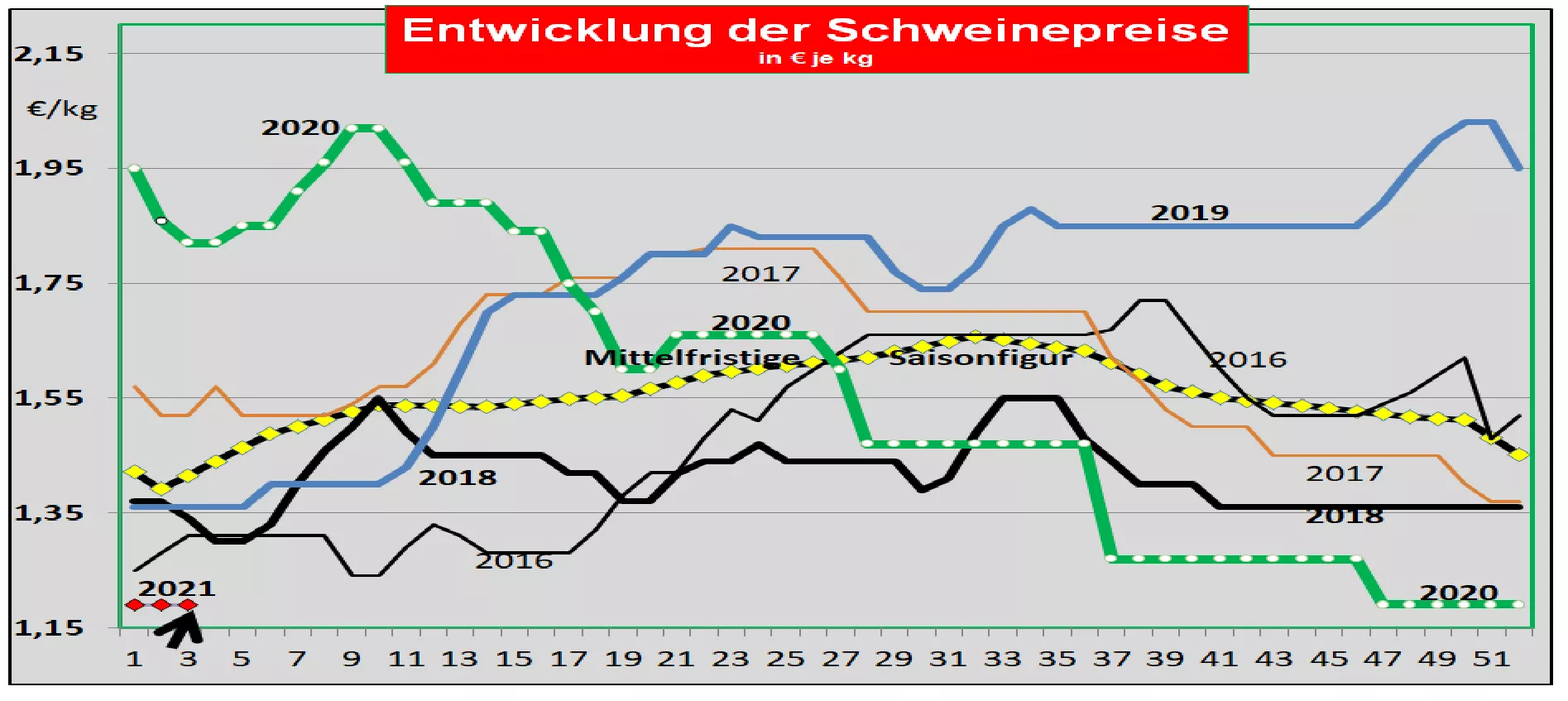

Germany: producer prices unchanged. - Supply backlog remains high The weekly battle figures were 674,041 excluding East Germany. The slaughter weights have increased to 100 kg. The pre-registrations are 372,000 (previous week 376,100) and continue to signal a supply backlog. When reselling the pieces to food retailers, processors and for export, the average prices were set back by -1 ct / kg; in particular the chop and neck have been lowered; the remaining sections remained unchanged. After the holidays, precious parts are less in demand. The V price for the period from January 14th until January 20, 2021 will remain unchanged at 1.19 € / kg. As of January 12, 2021, 495 wild boars infected with ASF have been officially confirmed in Brandenburg and Saxony. The find in Berlin has not been confirmed as an ASP.Market and price development in selected competing countries : In Denmark the prices were kept unchanged in week 2, 2021; all slaughterhouses are working again. In Belgium , prices will remain unchanged at a low level. The overhangs have not yet been removed. Netherlands : Prices are to be increased by 1 ct / kg in the 3rd week. In France , prices in Brittany remain stable at 1.20 € / kg. Battle numbers are still high. The slaughter weights have risen to 98.1 kg. In Italy , the prices remained unchanged at the equivalent of € 1.42 / kg. The market situation has eased. The live supply is sometimes scarce. Ham market has a need. Price increases are no longer excluded. In Spain the quotations remain unchanged at the converted 1.46 € / kg. The slaughterhouses quickly accept the live offer.However, exports with a focus on China ensure sufficient sales. Domestic sales stalled, not least because of the snowfall. In the USA , producer prices in IOWA rose again to € 0.93 / kg. The battle numbers remain high, but the weights are falling again. The front month of February 2021 is traded on the Chicago Stock Exchange at a stable 1.24 € / kg. Brazil : Producer prices have stabilized at € 1.50 / kg. The stronger exchange rate contributed to this. In addition, there are again increasing export revenues in the Chinese business. China: The average prices have again increased significantly with the equivalent of € 5.79 / kg. Demand is increasing due to preparations for the Chinese New Year celebrations on Feb 12, 2021. The increasing in-house generation still delivers too little. Growing import figures only barely cover the shortfall. Significantly lower prices are expected for the later course of the year. Conclusion: The supply backlog in this country has not yet been reduced.Domestic sales remain weak in some countries for the time being, while others are showing a clear recovery. The further prospects point to relaxation in the battle numbers. First small price increases are no longer excluded.

ZMP Live Expert Opinion

The sales situation is usually very sluggish after the holidays. Even more so under Covid and ASP conditions. The prices show hardly any movement. The V price has been unchanged for months. But in some EU countries such as Spain, Italy and Denmark there is movement in the market and pricing. There are first rays of hope for relaxation on the supply side. Slight price increases are no longer excluded.