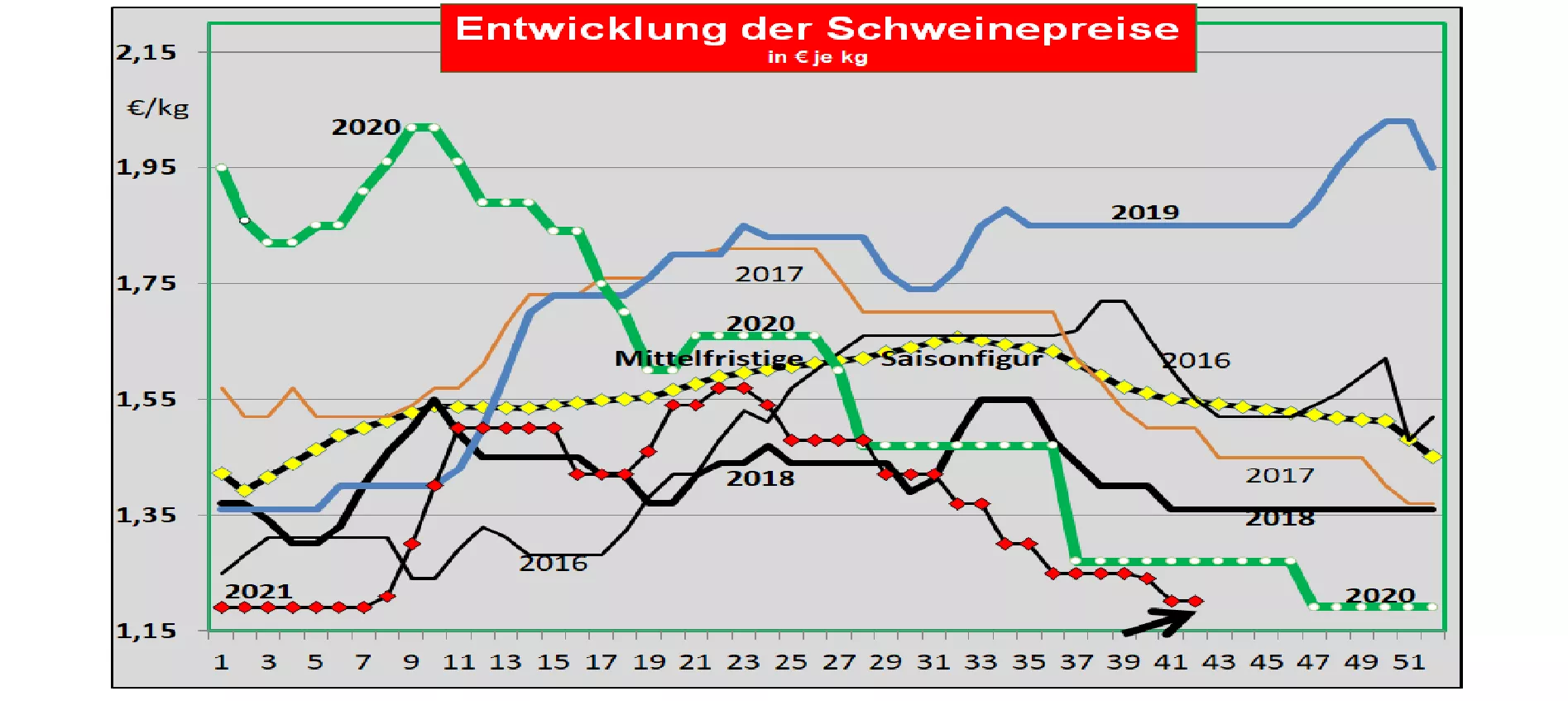

Germany: V- price unchanged at 1.20 € / kg - ranges from 1.20 - 1.25 € / kg. The weekly slaughter figures are 836,323. ( Previous week 836.908) fell insignificantly, the slaughter weights have increased further to 97.3 kg. Games are partially pushed. The pre-registrations have increased again with 298,100 pigs (previous week 286,400 ), the tendency for seasonally high live offers in autumn remains for the time being. When reselling the pieces to food retailers, processors and for export, the average prices were reduced by a further -4 ct / kg . The ham gave -6 ct / kg and the neck by -8 ct / kg. The food retailer's advertising campaigns do not have a positive price effect.At the ISN auction on Tuesday, October 12th a price of 1.23 € / kg came about with an offer of 730 pigs. There was an overhang of 22% The V price is for the period from October 14th. until October 21, 2021 remained unchanged at 1.20 € / kg; the range from 1.20 to 1.25 € / kg as well. As of Oct. In 2021, 2,370 wild boars infected with ASF were officially confirmed in Brandenburg and Saxony. There are no new cases of infected domestic pigs. Market and price development in selected competing countries: In Denmark the prices have been reduced by -4 ct / kg in the 41st week of 2021 . The sales problems in the EU internal market and in third-country business are putting pressure on prices.In Belgium the prices in week 41 have been lowered by a further -2 ct / kg. T he prices are significantly below 1 € / kg. In the Netherlands , prices have remained unchanged in week 41 after the previous cut. In France / Brittany the prices were reduced by -2 ct / kg to 1.22 € / kg . The number of slaughtered pigs continued to rise to 376,285 pigs. Cheap imported goods from EU countries are pushing prices. In Italy , after a short stabilization phase, the prices were lowered by a further -3.8 ct / kg in the 41st week. The end of the holiday season and cheap imported goods lead to price pressure. In Spain the prices were again reduced by -3.5 ct / kg in week 41. The prices are converted to below € 1.40 / kg . Increasing slaughter volumes meet declining sales volumes at home and abroad.Inventories continue to rise. In the USA / IOWA , prices have fallen further to € 1.33 / kg due to current increases in supply. The listings on the Chicago Stock Exchange have fallen to 1.71 € / kg. The reduced inventory levels and low cold store stocks mean that prices are moderate. Brazil: Producer prices have stabilized on average at € 1.47 / kg. The throttled business in China remains the decisive price support. China: The latest prices have stabilized at € 2.28 / kg. For Nov-2021 , futures prices, which have risen again, will be traded on the Dalian stock exchange with € 2.23 / kg . For 2022, the number of battles is expected to decline again. On the Dalian stock exchange, the September 2022 date is already again with approx.3 € / kg traded. Conclusion: Persistently high slaughter numbers, slaughter weights and advance registrations as well as high stocks of cold stores push producer prices down if the sales situation continues. The meat sales did not start despite the price reduction last week. The lack of third country sales leads to strong supply pressure in the EU internal market.

ZMP Live Expert Opinion

The lack of third country exports and the limited demand for meat in the EU internal market continue to depress producer prices. The market situation is exacerbated by the usual seasonal increase in live supply. Advertising measures by the food retailer and price reductions for the cuts remain without a noticeable increase in sales. Limited hopes are directed towards the pre-Christmas business and a decline in the live supply due to the reduced number of piglets months ago.