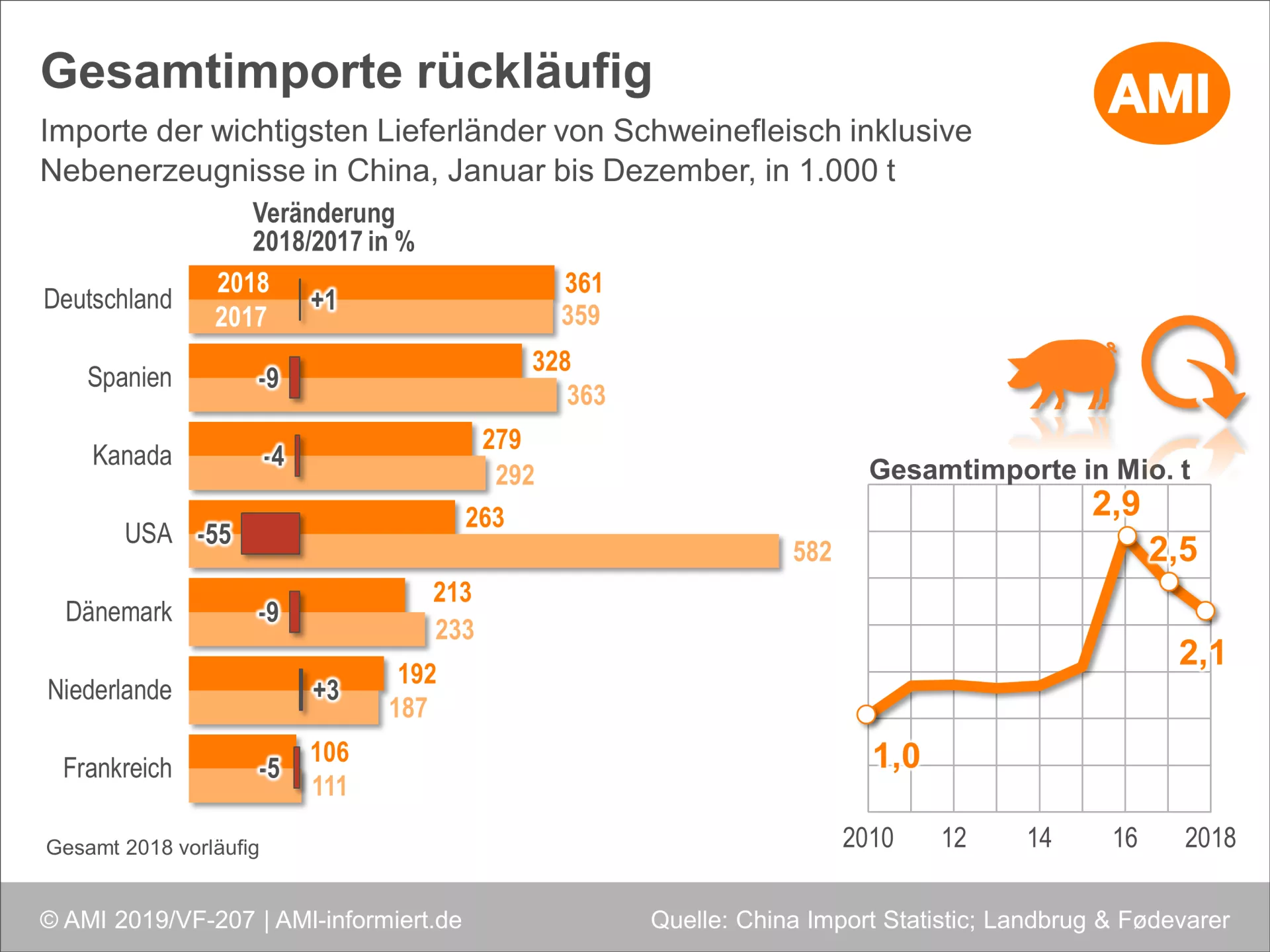

(AMI) After a difficult year in 2017, shipments of pork from Germany to China picked up again slightly in 2018. At the same time, the import requirement for classic by-products was much lower. At 946,000 t, the country of the center ordered more than a fifth less by-products than in the previous year. Correspondingly, total imports also declined; among the five most important supplier countries only Germany was able to keep its exports stable. So it is not surprising that currently meat exporters deplore price pressure in the trade of by-products to China. Whether there is a consensual solution in the trade dispute between the US and China can not yet be said, as the negotiations drag on into March. First signs indicate a relaxation. The African swine fever is spreading unchecked in China. Market analysts report that China's total pig population decreased by 11% (- 38.3 million) in December 2018. The reasons are the lack of profitability and stricter environmental regulations. The herd of sows was downed in December by 700,000 animals to now 29.7 million pieces. This reduction rate alone is as large as the total sow stock in Poland.Within the past 12 months, the rate of degradation among sows was 4.5 million. At the end of January 2019, pig prices in China once again fell sharply (-8 Ct / kg liveweight in just one week). Many marketers in the EU are in the starting blocks and hope that the export engine China starts again. Currently, there is still no sign of this, as China still has a large oversupply due to the strong reduction in pig herds.

ZMP Live Expert Opinion

At the beginning of the new year, German foreign trade is not getting off to a good start, and the meat market generally has no impetus. At least in the near future, it will not change much. In the spring, however, international trade will start to pick up again, and China will then again be an important buyer. At least if Germany continues to remain ASP-free.