Lower canola crops in the EU and the Ukraine

In the EU, the rapeseed acreage in Germany is 4.5 per cent in the UK by 5% and in France by around 1% lower to apply. Total to 6.5 million hectares of rapeseed area in the EU be has been ordered. However, the last word is not spoken yet, because the low winter hardiness of plants as a result of the previously warm weather could have at a surprise frosts in the Feb or March 2015 further damage. Also the usage ban on Neonicotinoids is being blamed for the decrease in the acreage.

Shrink in the Ukraine may 2015 the rape area to harvest . The IGC expects a decline of 5 percent to 890,000 ha. Also accounted for 20 percent of weakly developed areas have reported Bonituren in the Ukraine in mid-January. A year ago this proportion was only at about 5 percent. For the EU supply of Ukrainian rapeseed cultivation is of great importance, because the Ukraine exported most of the canola crop towards Western Europe.

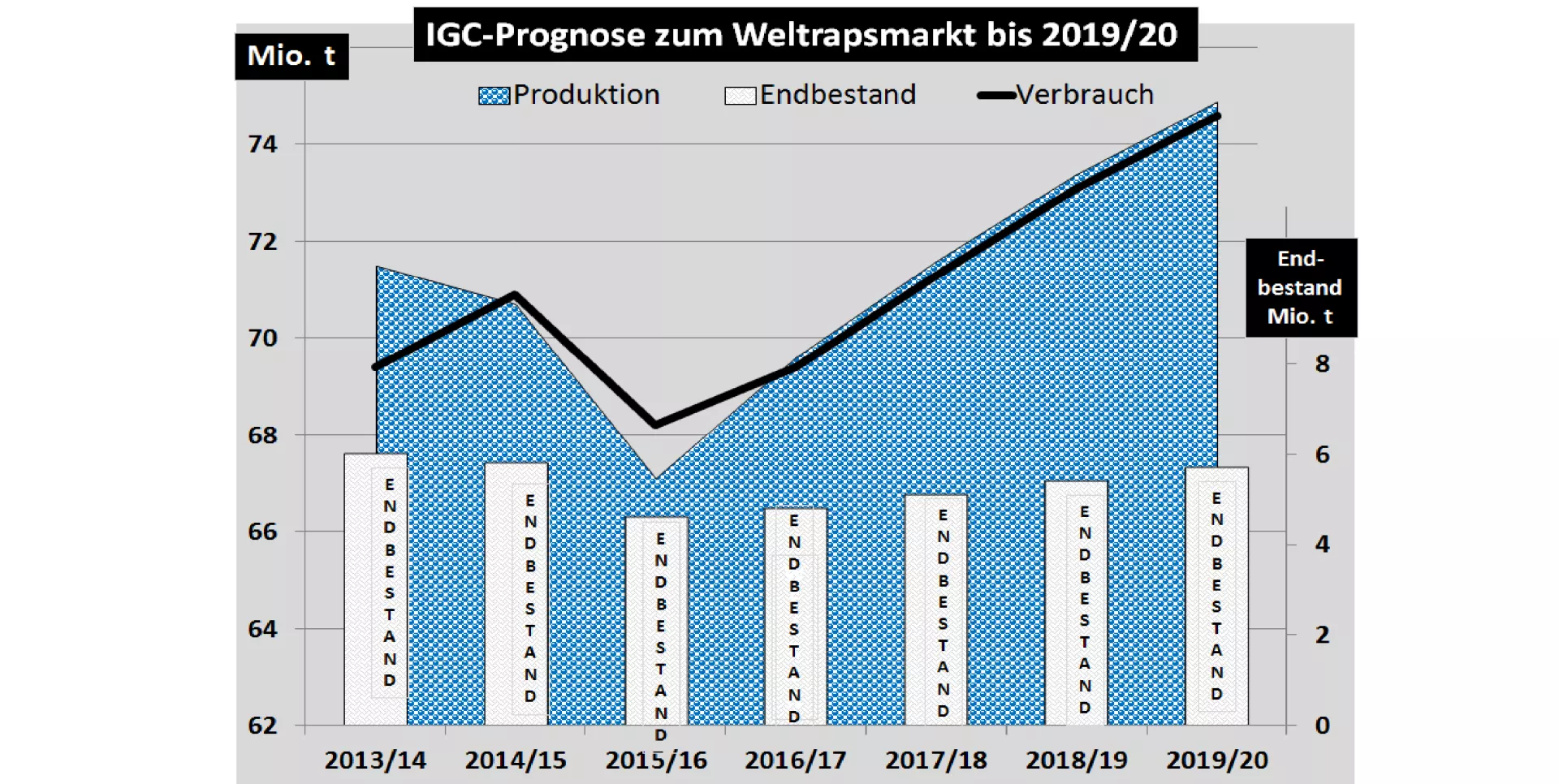

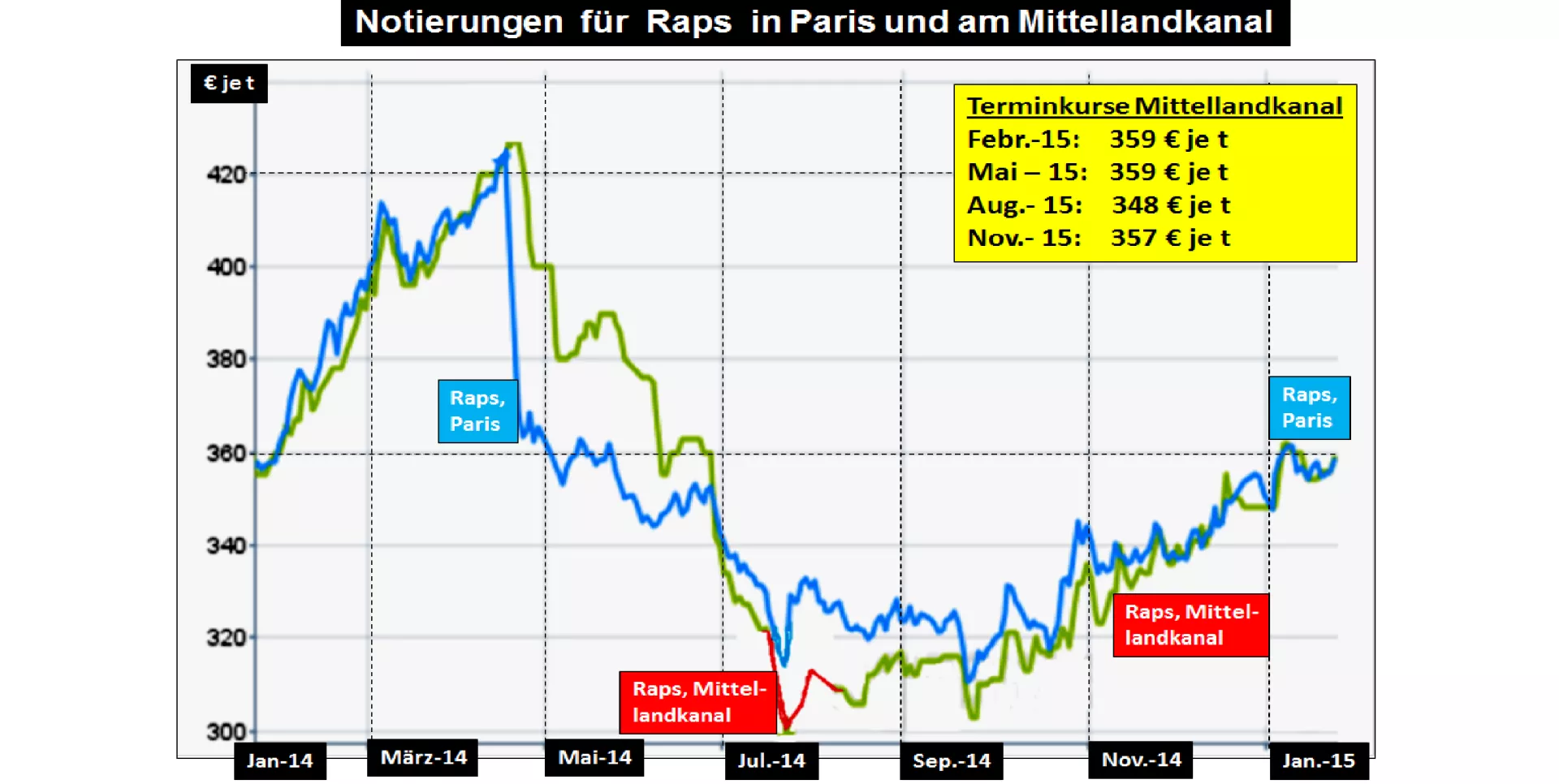

The canola harvest 2014/15 is over 24 million tonnes (previous year 21.5 million tonnes) estimated. Consumption should be about 25 million tonnes. The import demand will be smaller, but have to import expensive due to the weak euro exchange rate. It keeps the rates of rape despite stiff competition from the crude oil storage and the low-cost market leaders palm oil and soybean oil at a comparatively high level. Knapp available sunflower oil this year provides also a strong demand for rapeseed oil in the food sector.

For the coming year a lower rapeseed crop is expected to not only because of the reduced acreage , but also for the reason that a is not expected to repeat the record income due to the favourable weather conditions. Should fail the offers from the Ukraine small as expected and the purchasing power of the euro will not significantly improve canola prices at a stable level will remain. The expected high soy offers in the course of the year 2015 are, however, keep the rapeseed quotes in chess.

Still the question remains open after the flood-damaged oil palm plantations in Malaysia. The current yields are significantly lower than average. However, stocks are still sufficiently high. Move the palm oil prices for the remainder of the year just above the $600 per t brand and are so far removed from previous values between 700 and $800 per t.