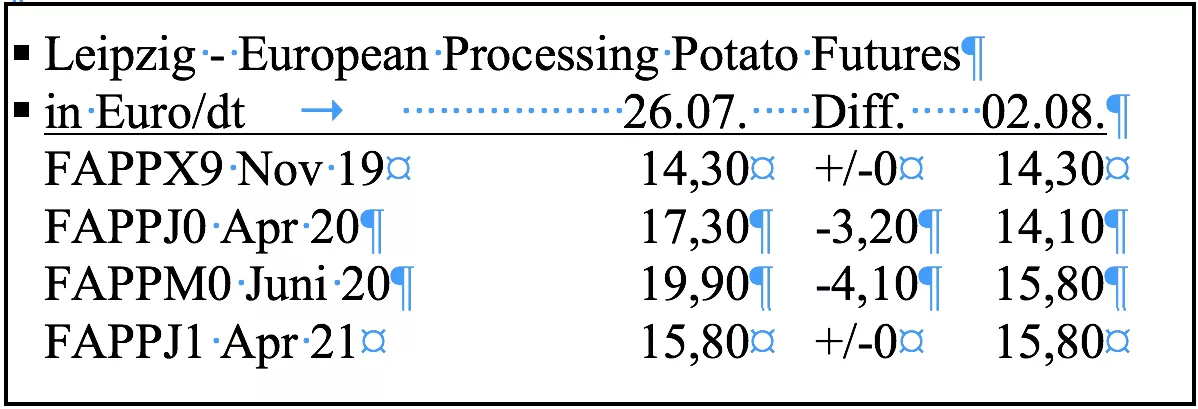

From the Rhineland too, good yields are reported from potatoes that could be irrigated. However, as the marketing of the early frit raw material has progressed far, the situation in this country is not as dramatic as that of the Belgians. It is said that the price corrections there are probably too violent, especially since the yields and varieties of the main crop by no means high yields can be expected. Where it has not rained, even total failures. The Belgapom are known to be very volatile with their quotations. The week before, fry had been bought from the British Isle because the expensive contract potatoes from Bordeaux were not enough to fill a supply gap between old and new crops. Meanwhile, the British deliver their early frit crop to Poland, where there are also supply shortages. Overall, prices for consumer potatoes in Europe can hold their own relatively well. The seasonal discounts are limited almost everywhere. Belgium is an exception with its quotation for frit raw material.As there is only an oversupply in Belgium this season during the harvest, the price corrections for the Belgian cash market are understandable. The farmers there want to quickly clear their potato fields to recreate vegetables and cabbage. This uncoordinated offer has led to prices of 3 € / dt in years when a good harvest is expected. By contrast, the 15 € / dt of today are veritable high prices. The current supply also exceeds demand, because the new potato acreage has been significantly expanded. However, irrigation bans in West and East Flanders have also increased the drought risk in Belgium. The Belgian main crop already shows significant signs of maturity. It can be concluded that high yields are unlikely. The heatwaves in June and July also increased the potato stocks in Germany, France and Holland. Irrigation measures were only used for cooling and maintaining health. The clearing of the area as well as the marketing of the new potatoes are already well advanced, not only here. Now, the fear is again, if there is again volunteers, which would damage the crop quality.But no one thinks of early maturing, because the calibers are generally much too small. The AMI therefore speaks of a robust market situation. This certainly applies to the ware potato market, where the packing stations have already been able to secure the high price level for the next few weeks. Producer prices of 45-50 € / dt are not hindering the sale to private households, it is rather the midsummer weather, which leads to drastic losses in sales. In Germany, sales of table potatoes dropped by as much as 14.2% in June compared to June 2018. For a year, the potatoes lose 4.1% of the buyer's favor. On the futures market in Leipzig, the prices of the April 20 contract for processed potatoes last followed the events on the Belgian cash market. With very decent daily turnover, prices fell the most traded maturity since reaching the previous contract high of € 21.1 / dt on July 23 daily. These were already the harbingers of the better possibilities for sledding and the higher willingness to deliver in Belgium. Today, the contract low was 13.7 € / dt and thus only a good euro over the previous Kotrakt low, which was traded on June 17, before the second heat wave.The volatility of potato maturity is particularly high this year. This may also be due to the fact that the contract stock of just over 5,000 lots has not reached the same level as in previous years. This in turn suggests that some market participants are still waiting for their optimal price. For fry factories prices of 15 € / dt would not be a bad course; After all, you pay such prices in preliminary contracts. Only with the difference that one is not sure, whether such offers come from the farmers this year

ZMP Live Expert Opinion

This week, the prices for early frit raw material in Belgium fell to only 15-18 € / dt. This was confirmed today in the Belgapom quotation, which was set at 15 € / dt. In Belgium, the yields of new potatoes are high, stocks are now ready for harvest and the possibilities for grubbing are good. The supply now exceeds demand and prices collapse. In the last two weeks for 20 € / dt were quoted, now it is five euros per 100 kg less. A sharp cut.