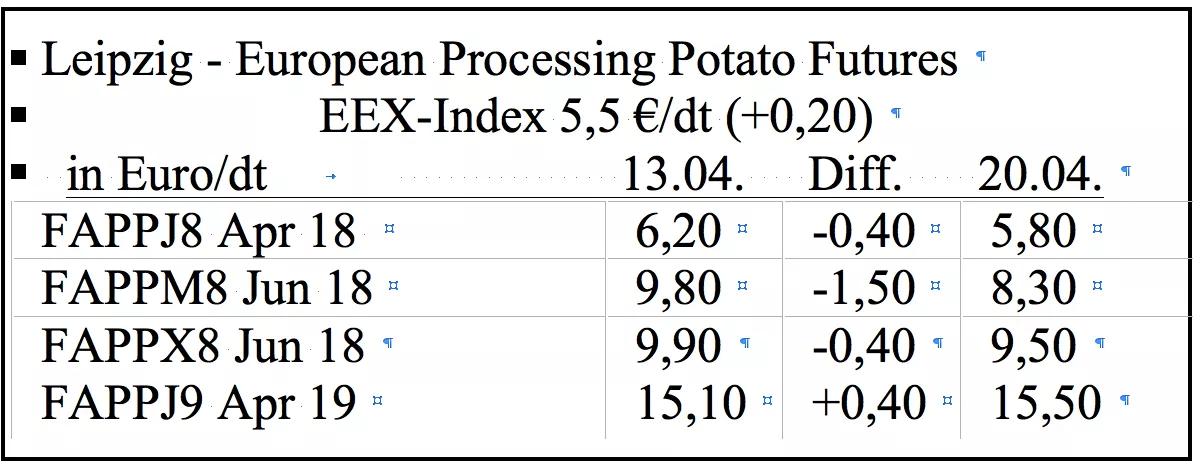

The French producer organization UNPT, the Flemish group ABS and potato producers in Wallonia (FWA) have now set up an interregional project aimed at identifying alternatives for the sale of excess quantities. In a first step, the project aims to support the opinion-forming process of potato growers by providing a forecast of significant excess quantities already at the beginning of each marketing period. In a second step, opportunities for sales in alternative usage directions and the conditions for it are to be offered. The project focuses on different areas, such as utilization as feed, processing into potato starch, biogas or industrial composting. In the end, it is now important that enough farmers from the region participate in the project. It started in January, is funded by Regional Economic Development Aid Fund and ends in early July 2019. "This idea has been thought of for years and dropped again and again. The system can only work if all farmers are involved and can be required to deliver and dispose of oversupply.But that would be equivalent to an expropriation and that would be contestable. The idea-makers in France and Belgium are just looking this year with envy on Holland and Germany, where there are starch factories, which, if there is enough supply, like to start their plants again in the spring to drive a special campaign. Although the proceeds for the potatoes usually only bring in as much as one has to pay for freight, the measure always has a market-supporting effect. The dichotomy of the EU potato market is currently particularly evident in the individual components of the EEX Potato Index. While the prices for processed potatoes in Germany and Holland are around 7 € / dt this week, only 4 € / dt are recorded in Belgium and France. This may also be due to the fact that there the variety Bintje still has a big market significance and this year also stands out due to many quality problems. But it is still offered and prevents the increase in prices of preferred varieties. In the meantime, Challenger, which often tends to darken, has joined the hard-to-sell varieties. Under these circumstances, one can hardly hope for higher prices.Meanwhile, Dutch and German farmers have been disposing of their problem lots for months in the feed trough or biogas plants and now in large quantities at the starch factory. But this process started early; actually already in the autumn, when it was clear that the potato market in the EU has a quantity problem this year. Market transparency is therefore not lacking. So, if France and Belgium also had starch factories that might be able to absorb surplus potato markets, they would not need projects that would be financed with public money. The fact that market participants can not hope for an automatism for cost-covering prices, despite the "emergency nail starch factory", is shown by the example of Poland, where last year saw such a big harvest that despite special shifts in the factories could not prevent loss-making producer prices. At the futures exchange in the coming week the contract April-18 ends its trade. The settlement price for the remaining 5,000 lots is estimated by me in a range of 5.3 to 5.7 € / dt.Meanwhile, in the June-18 maturity with 1750 lots has built up a sizeable stock. The prices fluctuated extremely strong in the last week. Some market participants expect that from mid-May on again a marketing pressure builds up. Last week's 10-euro mark has once again gone a long way.

ZMP Live Expert Opinion

In Central and Western Europe, more and more profitable potato varieties are grown year after year, which increasingly lead to overproduction and drive prices down. In the last ten years, there have already been three campaigns with a very high surplus of potatoes and low producer prices.