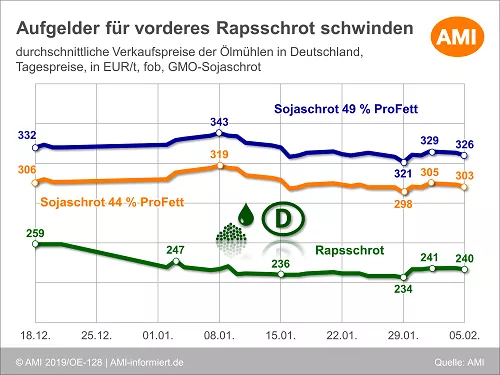

(AMI) - It's the old game, compound feed manufacturers buy manageable quantities with short delivery times. The longer-term contract business is neglected, because it pays off either way. This is also reflected in the claims, which have no price change until October. Currently 44er soybean meal for delivery from February to October is priced at 295 EUR / t from Hamburg and 48er at 316 EUR / t. So many buyers wait, if with the arrival of the first ships from Brazil something in the prices changes. As a result of the small harvest, more rapeseed is imported, around 3% more than in 2017/18, and almost three times as much in terms of meal. This was mainly due to the scarce supply of rapeseed meal that many processors had to switch to foreign goods. In addition, GMO-free feed continues to show increasing demand for use in dairy cattle feed. In this country, the supply on the front positions has not increased in price despite increasing processing of rapeseed. It can still be enforced over the following months. However, these are disappearing, with the exception of Mannheim, where 10 EUR / t of fees are still required.Mills in the north and west calculate at 2-3 EUR / t. In East Germany, however, nothing is felt, here February and March delivery are price identical. The demand for rapeseed meal, in spite of the surcharges, is also focused on the front delivery positions. Again, buyers do not want to be bound longer term, except on the basis of a completed compound feed business.

ZMP Live Expert Opinion

(AMI) - On the oil meal market, most shoppers do not want to commit themselves longer term and buy, if any, front-end goods for short-term needs. Everyone is waiting for the release of new USDA numbers; The trade conflict between the US and China remains a major source of uncertainty.