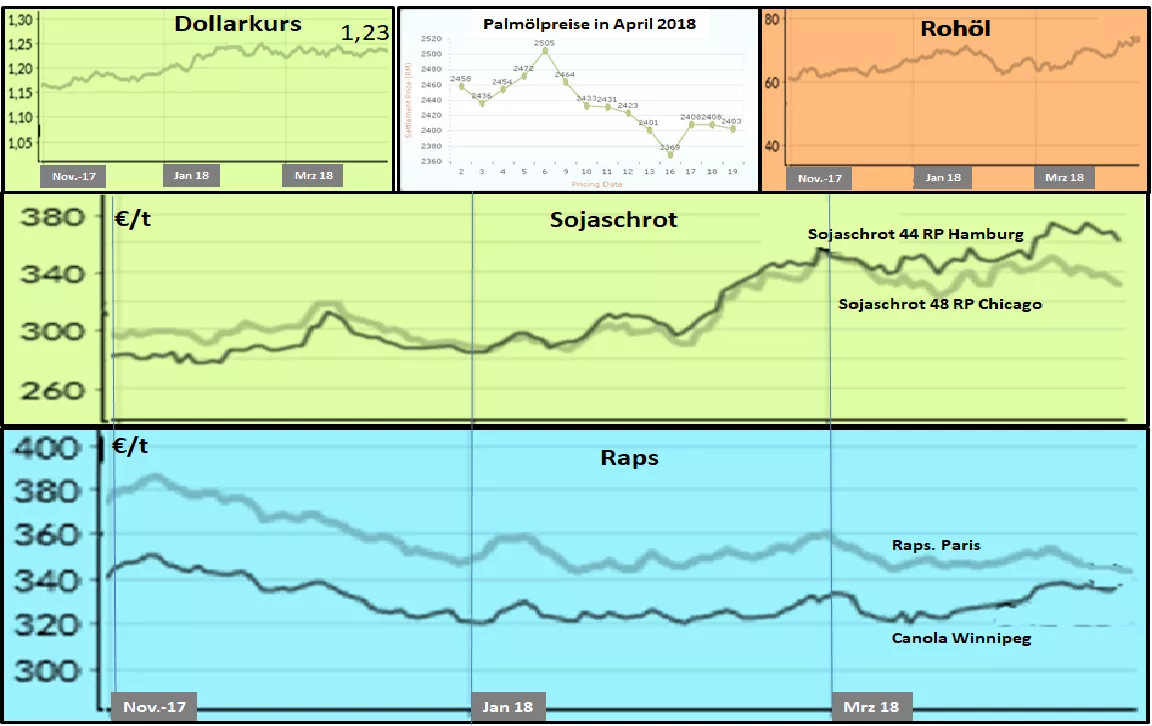

Soybean sinking after a brief surge - stable canola prices - low rapeseed prices The simmering trade tensions between the USA and China keep markets in a fragile state . At the moment, however, a slightly price-reducing phase is reigning. The external factors crude oil and the dollar exchange rate in the oilseeds market currently only play a minor role. The focus is on the ongoing soybean harvest in Argentina, the US export business with soya and developments in the rapeseed market. The Argentine soya crop is progressing rapidly. Almost half of the land should be harvested. Due to the threshing results, the harvest forecast is set even lower.The Argentine Ministry of Agriculture estimates the result only at 37.5 million t. Originally 56 million t were expected. The USDA had recently estimated 40 million t. This is offset by an almost completed record harvest in Brazil of a preliminary estimated 118 million tonnes (previous year 114 million tonnes), which is pushing for market in the coming weeks and months. Surprise is the current high US soybean sales , which are at the top of expectations. Should already be hamster purchases in the game before the punitive tariffs take effect?The prices for Canola in Winnipeg have risen despite the opposite trend in the soybean sector. One of the deciding factors is the weak Canadian dollar exchange rate, the transport-related delivery difficulties and the weather-related delays in this year's sowing. Next week, the Canadian Bureau of Statistics will publish the rape acreage. Expectations are ambiguous: on the one hand an expansion of the area is predicted, on the other hand the current weather conditions prevent a timely sowing. The rape courses in Paris remain under pressure. The quotations fall on the line of 340 € / t. Increasingly, the oil mills reduce the processing. The main reason is the EU's customs-friendly imports of biodiesel. Biodiesel is now traded much cheaper than mineral diesel. According to the latest estimate of the Raiffeisenverband (DRV), the German rapeseed harvest should be 8.3% better than the previous year's weak result of only 4.3 million tonnes. With the exception of Schleswig-Holstein, rates of increase up to double digits are projected. In Schleswig-Holstein are approx. 26% less land has been ordered primarily in the march due to adverse weather conditions. In addition, the average yield on the remaining Geestflächen should be smaller. In Mecklenburg-Western Pomerania, too, an area almost 10% smaller has been ordered, but is almost compensated by the higher expected area yields.In France, a rapeseed crop of 5.3 million tonnes is expected on average. In Poland , however, it is assumed that the crop will be reduced by 20%. According to estimates by the EU-COM, a result of around 22 million tonnes is to be achieved in the internal market .

ZMP Live Expert Opinion

The oilseeds market remains unstable. Crop failures on the one hand face bumper crops on the other. Above all, the sword of Damocles depends on the simmering trade tensions between China and the USA. In the rape sector, EU biodiesel imports are weighing on the price outlook. In the near future, in addition to trade disputes, soybeans in the US will become the dominant topic.