Since the beginning of the month, rapeseed prices on the local cash markets and on the Euronext/Matif exchange in Paris have fallen significantly. The most traded February contract closed on November 1st at a closing price of EUR 670 per tonne, but yesterday it fell below the EUR 600 per tonne of rapeseed. With the start of trading on Friday, however, the contracts have climbed back above the EUR 600 mark on all dates traded so far, but the contracts have continued to lose value over the week. The extension of the grain agreement, which also includes rapeseed deliveries, put pressure on prices. Although there has been repeated speculation over the past few weeks that the agreement could end, the majority of market participants believed in the future of the deal. It was announced yesterday that Ukraine and Russia, with the participation of the United Nations and Turkey, have reached an agreement on a 120-day extension. Meanwhile, European rapeseed imports are very dynamic. Up to November 13, 2.61 million tons of rapeseed were imported in the current marketing year. Ukraine has again become the largest supplier of the European Union. Around 2/3 of the quantities come from the country on the Black Sea.Australia increases around ¼ of the imported quantities. The EU Commission announced yesterday that it intends to provide 1 billion euros for the so-called "solidarity corridor". This is intended to improve the infrastructure with roads and rails from Ukraine to European ports in order to reduce dependence on the existing grain corridor. As part of the EuroTier 2022 that is currently taking place in Hanover, the Association of the Oilseed Processing Industry in Germany announced that rapeseed processing will probably be 800,000 tons less this year. In particular, the weaker harvest last year and the failure of Ukraine in the first half of 2022 contribute to this assessment. The German-Ukrainian Agricultural Policy Dialogue announced on Wednesday that winter rape sowing in Ukraine could be completed. The area under cultivation is currently said to be around 1 million hectares. For Germany, a prospective acreage of between 1.10 and 1.13 million hectares was recently forecast. If so, that would be one of the largest acreage areas in recent years. Soybeans have also indicated prices on the CBoT, although they are again green before the trading day.Soybean meal and soybean oil have also recently come under selling pressure. The reasons for this are diverse. On the one hand, crude oil prices have continued to fall recently, dragging oilseeds and vegetable oils down with them. The Chinese government has announced that it wants to relax some of the corona measures and thus fundamentally improve the export prospects for US soybeans, but the number of infections is currently relatively high again and many cities have been sealed off again, which weighs on the mood again. The soybean harvest in the USA is on target and domestic logistics have also improved as the Mississippi has more water after rains in October and November and ships can be loaded higher. On the other hand, the US export figures have recently been disappointing and are still lagging behind those of the previous year. In Argentina, the drought continues to hamper soybean planting. The grain exchange in Buenos Aires warned yesterday that there would be a significant reduction in the area under cultivation if heavy rainfall did not fall soon.Although precipitation is currently expected for the northern growing regions, it is unlikely to counteract the massive consequences of the drought. According to the grain exchange, only 12 percent of the planned acreage of 16.7 million hectares has been cultivated. Things are different in neighboring Brazil. Here, very heavy rainfall promotes plant growth significantly.

ZMP Live Expert Opinion

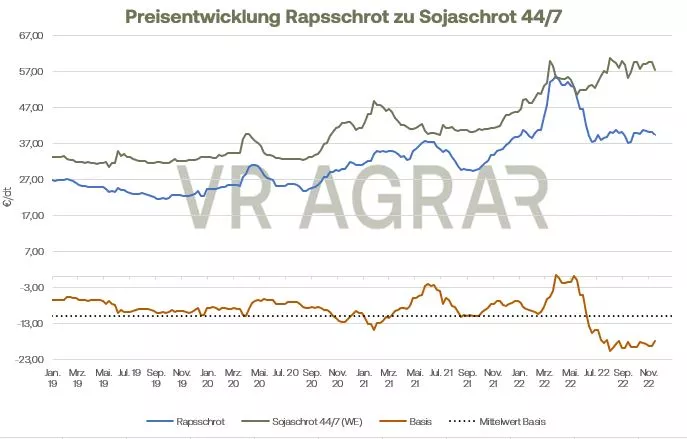

The oilseed markets are under pressure overall. The US soybean harvest, which is almost over, the good prospects for Brazil and the significantly improved global supply of rapeseed are putting pressure on the prices for oilseeds and oilseeds. This is clearly reflected not only on the stock exchange but also on the cash markets. Although the drought in Argentina is limiting prices, the bottom line is that the sales pressure for rapeseed and soybeans is unlikely to change much in the near future.