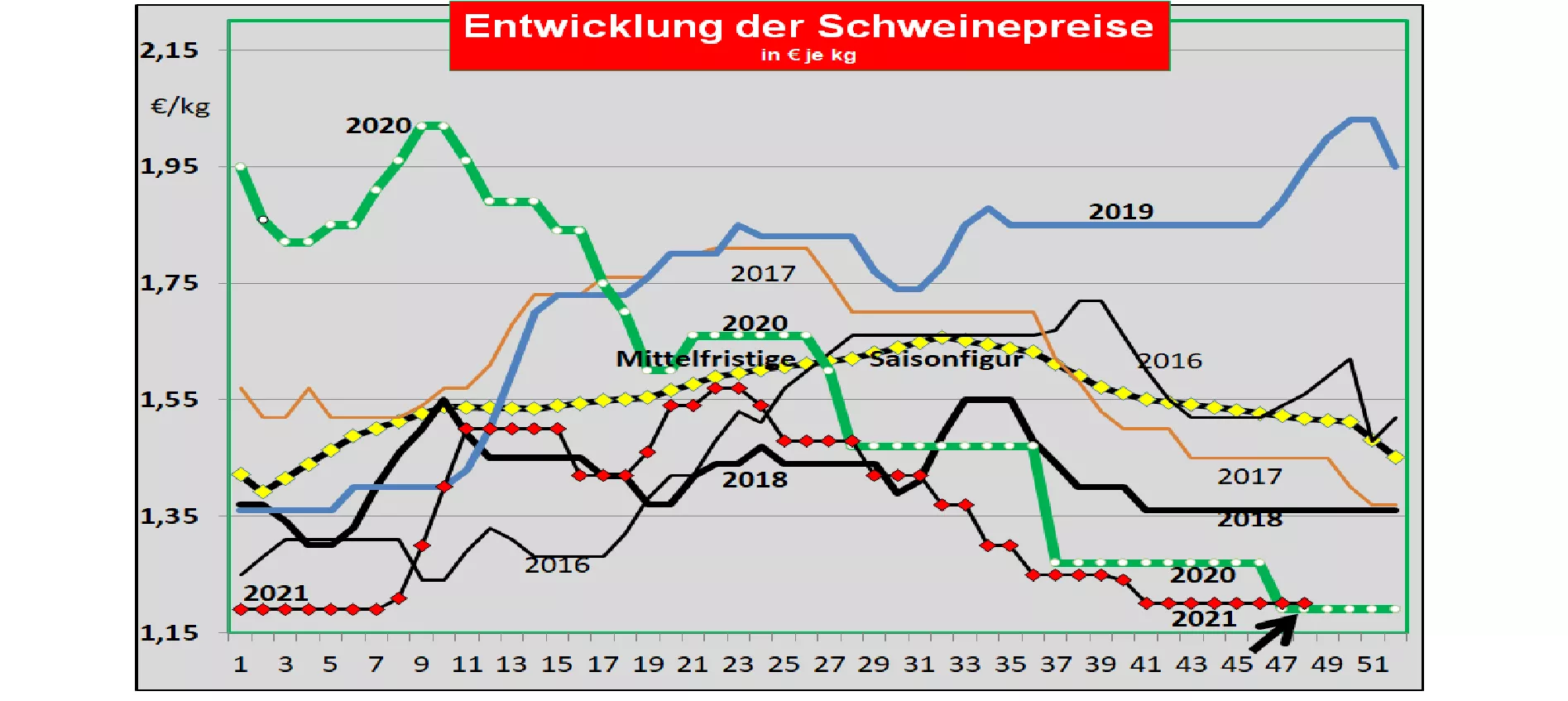

Germany: V price unchanged at 1.20 € / kg - ASP case so far without consequences The weekly slaughter numbers have tended to fall with 836,759 (previous week 847,994), the slaughter weights are also at 97.7 kg . The pre-registrations have decreased significantly with 291,800 pigs (previous week 304,700). This heralds a declining live supply due to the reduced number of piglet stalls. When reselling the pieces to food retailers, processors and for export, the average prices were raised from 1.67 to 1.71 in the last 3 weeks . The chop, shoulder and neck were the supportive pieces. The Christmas business brings the first impulses.At the ISN auction on Tuesday, November 23rd. a price of 1.24 € / kg came about with an offer of 1,100 pigs. A supernatant of 58% remained. The V price is for the period from November 25th. until 01.12.2021 remained unchanged at 1.20 € / kg; the range from 1.20 to 1.25 € / kg as well. As of Nov. In 2021, 2,791 wild boars infected with ASF were officially confirmed in Brandenburg and Saxony. The ASF case near Rostock does not show any negative market effects for the time being, but the cause of the introduction is still not known. Market and price development in selected competing countries: In Denmark the prices in the 47th week 2021 have been increased by an insignificant 0.4 ct / kg to 1.13 € / kg. The delivery of pigs for slaughter is regulated.In Belgium the prices in week 47 remained unchanged at the previous level of less than € 1 / kg . The previously narrow sales leeway has eased when it comes to exports. In the Netherlands the prices in week 47 also remained unchanged . In France / Brittany , the previous prices have increased slightly to € 1.237 / kg. In Italy , the prices in week 47 were +0.2 ct / kg higher. The pre-Christmas business is getting the market moving. In Spain the prices in week 47 were kept unchanged at the level of 1.15 € / kg. The sharp price decline that has persisted since July has come to a halt. Rising prices in China open the prospect of higher export revenues, but orders are still missing.In the USA / IOWA , prices have fallen further to € 1.09 / kg due to increasing numbers and weights of slaughter. However, the December 21 listing on the Chicago Stock Exchange has stabilized at 1.45 € / kg. The reduction in the number of pigs determined after the cattle count will ensure prices will rise again in the coming year to 1.65 € / kg (Apr.-2022) Brazil: The average producer prices continued to rise to 1.44 € / kg despite the weaker REAL. Rising export revenues in the Chinese business support the price increases. There are also hopes for duty-free Russian import quotas of 100,000 tons of pork and 200,000 tons of beef in the first half of 2022. Russia has lifted the import ban for Brazil, but not for the EU!China: The latest prices have risen to € 3.17 / kg with the support of a higher exchange rate. The price increase within 6 weeks is over € 1 / kg . For the January 2022 date , futures prices of € 3.12 / kg will be traded on the Dalian stock exchange. Conclusion: There are signs of an easing of the sales situation in the EU internal market across the board. The inadequate third country sales keep price developments in the EU internal market within narrow limits. With the exception of Spain, the battle numbers are tending to decline. There is some movement in the meat market as a result of the Christmas business. Several signs point to further relief in the pre-Christmas business.

ZMP Live Expert Opinion

The current battle figures are still high, but the pre-registrations signal future declines in the live supply. The previous reduced piglet stalls are slowly becoming noticeable. Rising partial prices indicate that Christmas business is picking up. Third country exports are still insufficient. The increased pig prices in China give hope for an improvement.