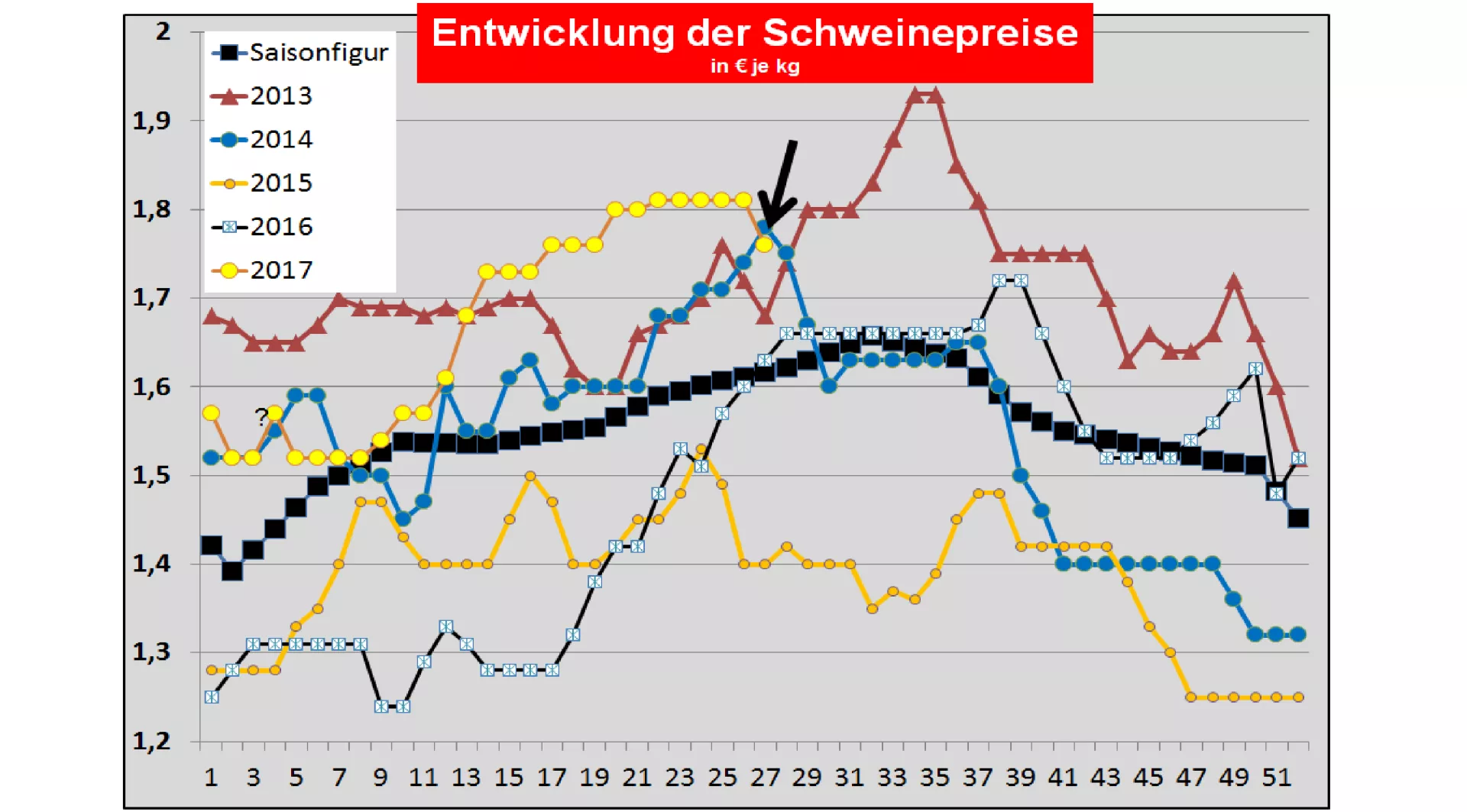

Pig prices for 27./28. KW-2017 The ISN internet listings on Tues, 04.07.2017 delivered an average result of 1.80 € / kg with a margin of 1.79 -1.80 € / kg. The offer was 3,385 pigs. There remained supernate of 79%! General Market and Price Development: Pork sales have now reached their limits. The domestic market and third-country sales remain weak. The slaughterings are very different from region to region. In Spain, pigs are scarce for the coming holiday season.In Italy the tourist demand contributes to greater sales opportunities. Austria also benefits from the holiday season. In France, the supply-demand ratio is balanced. In the USA, pig prices continue to rise as a result of the grilling season and the booming export to Mexico. Brazilian Pig prices remain on the downhill. In China, prices have now caught at 2.40 € / kg. The Chinese importers remain cautious. Chinese consumers are changing their consumption habits to the detriment of pork. Denmark: Danish pork prices were raised in the 27thKW-17 remained unchanged . The slaughter numbers are -7.3% below the previous year's level. For the coming 28th KW-2017 , the prices will be reduced by -4 ct / kg . In France / Brittany was The listing (06.07.) Is maintained. The reported slaughter figures for the whole of France are included 358784 (Previous week 365,387 last week 365,864) pieces continue in the lower midfield. The Dutch slaughtering companies in .KW between 0 and -4 ct / kg paid. In the 28th KW 2017. , , , , Ct / kg can be paid.(Addendum follows) Belgium: Pig prices were paid unchanged in the 27th KW . The quotations of slaughterhouses are to be KW 2017 ....... Ct / kg.(Supplement follows) Germany : The slaughter numbers reach 961,963 (Previous week 983,714 last week 984,597). For the coming period from Thursday 06.07. Until Wednesday 12.07. (26./27. KW-17) the association price was 1.76 € per kg respectivelyIndex point decreased by 5 ct / kg. The range ranges from 1.75 to 1.78 € / kg. The announced delivery volumes for the coming week are again lower at 215,263 (previous week 220,300 previous week 218,228 22). The fattening pigs' basic fare in Austria was introduced for the 26th / KW Unchanged .For the 27./28. KW the basic travel is only -2 ct / kg Can be lowered. The pork prices in Spain were published on Thu, 29.06. Increased by +1.0 ct / kg.In (Upper) Italy are pig prices on 05.07. In Modena at +1.3 ct / kg , at Di in Reggio +1.5 ct / kg and Cremona by +0 ct / kg . The slaughter numbers are 36.397 (previous week 40.928 last week 41.253 41.561) in the lower one Midfield. In Poland , pork prices at 57% MFL of 1.75 € / kg were recorded on 23.06.2017 .Outlook: The meat demand of the barbeque season has passed a first high point. The onset of vacation / holiday time slows demand here and shifts to the southern holiday countries. The live offer is sufficient for the need. The pre-registrations indicate that the number of abattoir slaughters is declining for the current week. The US prices are on 03.07. Remained at 1.71 € / kg .The exchange rates in Chicago for the delivery date June-17 have risen to 1.68 € / kg. The barbecue season and the booming third-country export to Mexico supported by a weak dollar are the most important price-drivers on a high supply. However, the slaughter weights give up at high temperatures 93 kg back.In the autumn months, prices between 1.35 and 1.40 € / kg are expected. China's pig sires have caught at the end of June at 2.40 € / kg for the time being. Increasingly It turns out that the Chinese consumers consume less pork, and for this they increasingly rely on vegetable side dishes. Vegetable sales rose by + 30% compared to the previous year, while pork demand remained low despite sharply lower prices.The Russian pig prices rose to 2,20 € / kg on 28.06.2017 . Brazilian pork prices are based on the average values in the Southwest region on 03.07. To 1.17 € / kg. The main reasons for this are seasonally low domestic prices. The real has remained constant.

ZMP Live Expert Opinion

The first wave of the seasonal high price phase is over. The influence of the holiday / vacation season started is noticeable: here with declining prices, in the south of the EU with rising prices. , The decline in third-country exports is exacerbating the sales problem. The livelihood is limited. According to the pre-registrations, the slaughter numbers could still be a little lower. Probably enough for a price stabilization.