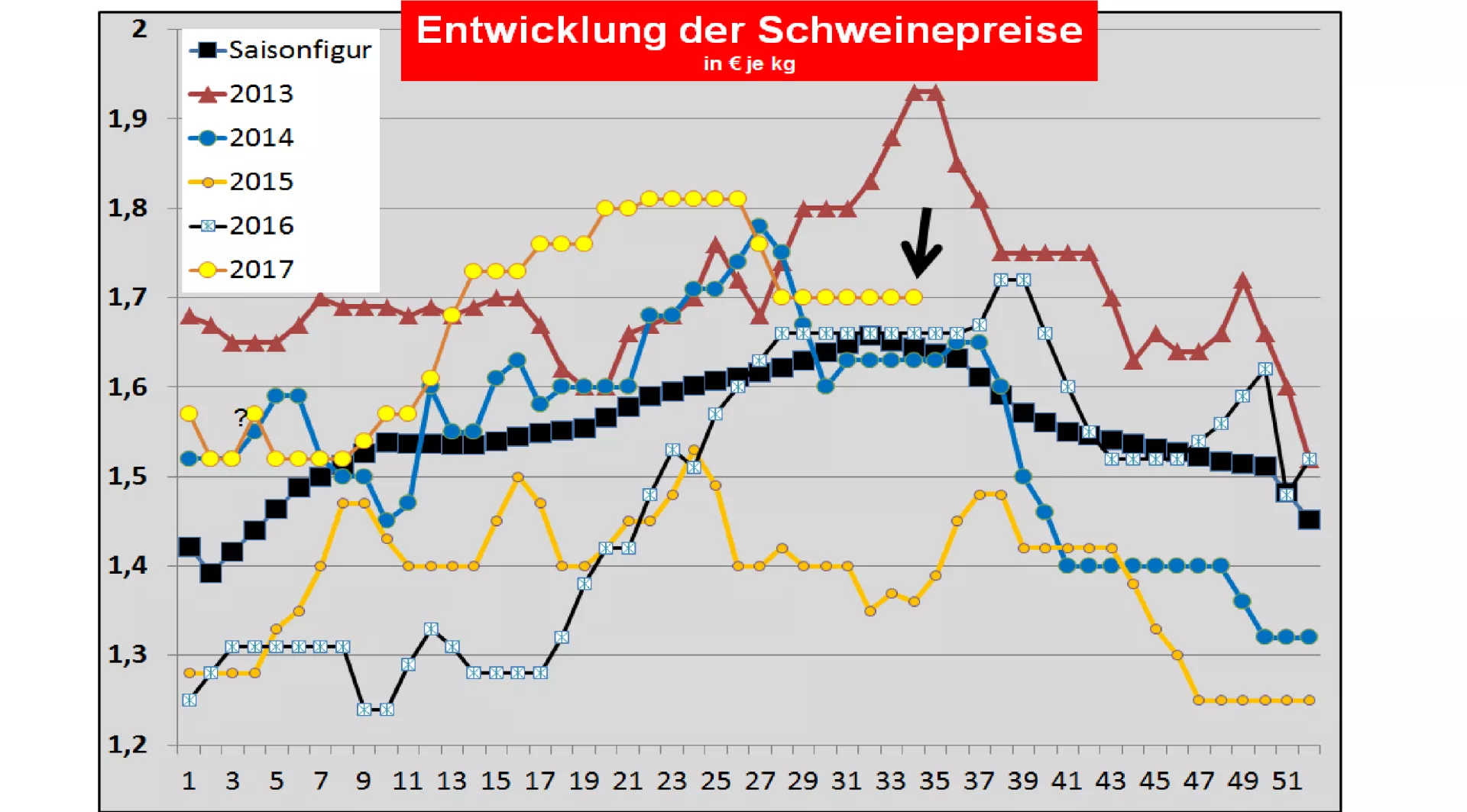

Pig prices for 34./35. KW-2017 The ISN website on Tues, 22 August 2017 provided an average profit of 1.75 € / kg for a range of 1.73 -1.76 € / kg. The offer was 2,695 pigs. There remained a supernova of 13.3%. General market and price trends: The sales business in the meat sector has improved slightly in some federal states, despite holidaying. The slaughter numbers and the battle weights remain below average. In Spain, the first weaknesses in maintaining the high price level are apparent. In Italy the prices of pigs are now noticeably lower. In France, the supply-to-demand ratio remains balanced with slightly declining prices, taking into account the holiday.In the US, there is a regular price slump Brazilian pig prices are also not up to date. Prices in China and Russia are picking up again in season. Denmark: Danish pork prices were published in the . KW-17 reduced by -2.7 ct / kg The slaughter numbers are -6.1% below the previous year's level. For the coming 35th KW-2017 , the prices will remain unchanged.In France / Brittany was The quotation (24.08.) U m -2.3 ct / kg is reduced . The reported slaughter figures for the whole of France are included 297,862 (previous week 360,958 last week 356,062) piece due to the holiday lower. The Dutch slaughter companies paid unchanged in the 34th KW . In the 35th KW 2017, , , , , Ct / kg can be paid.(Addendum follows) Belgium: Pig prices were maintained unchanged in the 34th KW . The quotations of the slaughter companies are for the 35th KW 2017 ....... Ct / kg.(Supplement follows) Germany : The slaughter numbers reach 965,887 (previous week 966,513 previous week 952,039) pieces. For the coming period from Thursday 24.08. Until Wednesday 30.08. (34th / 35th KW-17) , the association price was maintained at 1.70 € per kg or index point .The range ranges from 1.70 to 1.70 € / kg. The announced delivery volumes of the next week are slightly lower again at 224,400 (previous week 226,100 last week 217,500), but are still below average. The fattening pigs' basic fare in Austria was valid for the 33rd / KW remained unchanged. The pig supply falls measured with the end of the holiday period to the demand. For the 34th / KW should be retained. The pork prices in Spain were published on Thu, 17.08. By 0.1 ct / kg. In (Upper) Italy , pork prices on 21.08.In Modena at -1.9 ct / kg , at Di in Reggio -1.2 ct / kg and Cremona unchanged Have been paid. , The slaughter figures are included 34,519 (previous week 45,060 previous week 39,575) pieces due to holiday low.In Poland on 04.08.2017 pig prices at 57% MFL of 1.662 € / kg were quoted. Outlook: The hopes of an improved demand for meat remain low due to the holiday / holiday season. In the southern countries of the holiday, the prices return with an ending holiday period. The local pre-registrations continue to indicate little change in slaughter numbers for the current week. The US prices are at 21.08. In IOWA fell to € 1.34 / kg . The stock exchanges in Chicago for later delivery dates in late summer and autumn Indicate a markedly downward tendency. In the autumn months prices are expected to reach 1.20 € / kg.The dollar, which is no longer quite so weak, is less powerful To the export business. The slaughter weights are again over 93 kg. China's pig pens Have joined 2,45 € / kg have on 16.08. For the time being. We expect a more friendly business in the coming months, but the big moment is not to be expected. Chinese pork imports continue to be very restrained.The Russian pork prices have risen to € 2.03 / kg on 16.08.2017 . The ruble remained largely unchanged. The increase in domestic supply leads to a self-sufficiency rate of 95%. The current pork demand is at the same level as 3 years ago. In the foreseeable future, Russian pigmeat exports will become necessary for market relief. Brazilian pork prices are based on the average values in the southwest region on 21.08.stopped at 1.37 € / kg. decreasing Domestic prices and a weak real contributed to the result.

ZMP Live Expert Opinion

By and large, the supply / demand ratio in the EU is balanced. In the south, holiday seasonal fluctuations are observed. In the north, one hopes for better sales conditions after the holiday season. The live offer keeps itself in moderate course. Price hikes remain subdued for the time being. In the international arena, prices are declining in the USA and Brazil, while Russia and China are currently experiencing slight price recovery. The renewed strengthening of the euro is slowing export prospects.