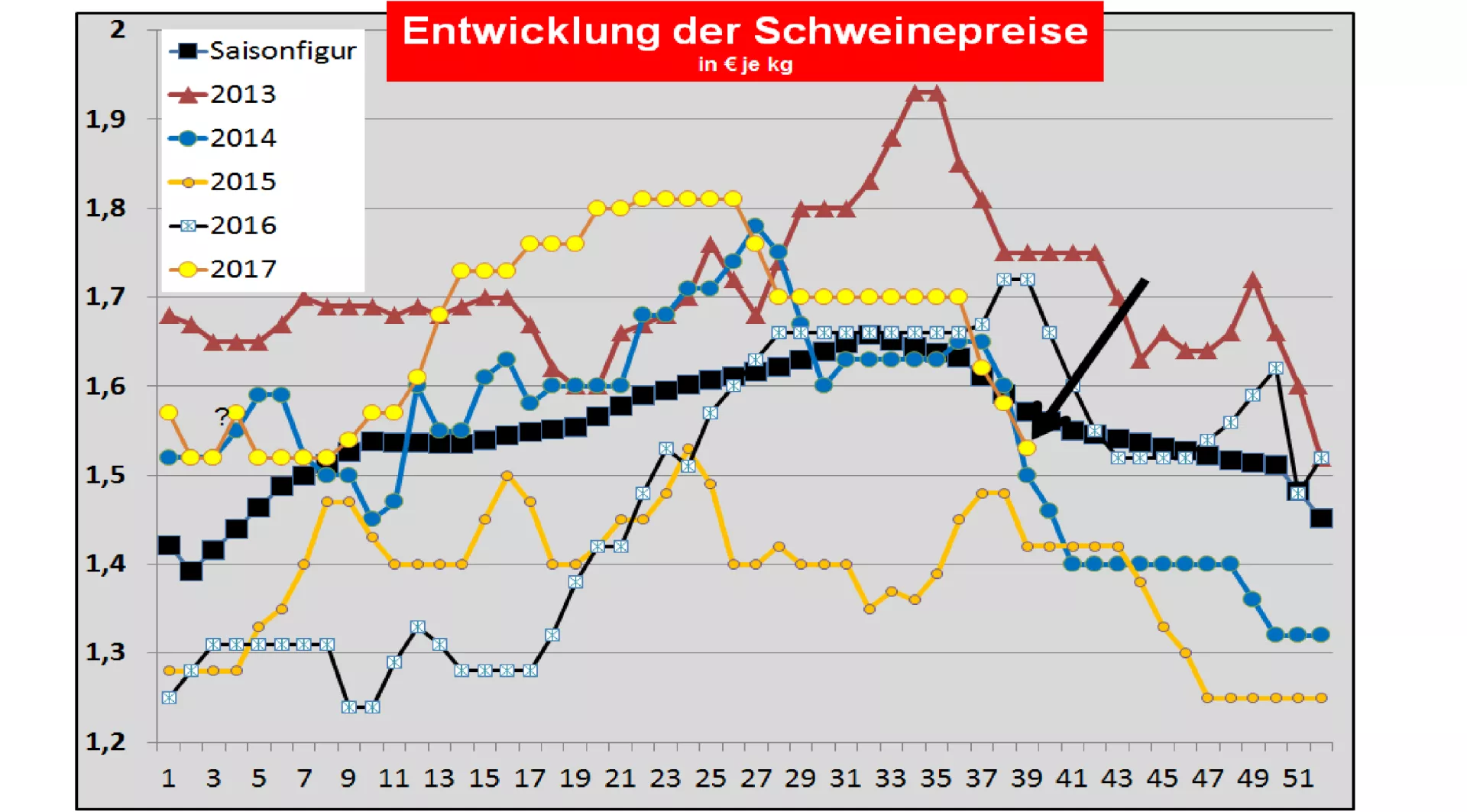

Pig prices for 39./40. KW-2017 The ISN Internet webcast on Tue, 26.09.2017 provided an average result of 1.56 € / kg with a margin of 1.555 -1.565 € / kg. The offer was 2,400 pigs. There remained a supremacy of 62.5%. General market and price trends: Increasing slaughter rates in almost all regions of the EU put pig prices under ongoing pressure. Even Italy is not exempt. In Germany, the price cut is now 18 ct / kg. In France have a marked impact on prices. In the USA, prices have fallen from 1.50 € / kg to less than 0.9 € / kg within 7 weeks. Brazilian pork prices have only been able to hold their own. Prices in China are continuing, in Russia, there is a marked setback, presumably due to the AKP. Denmark: Danish pork prices were published in the 39 . KW.-17 was reduced by 2.7 ct / kg. The slaughter numbers are -6.0% below the previous year's level. For the coming 40th KW-2017 the prices are lowered by a further -4 ct / kg . In France / Brittany was the listing (27.09.) u m further - 0.4 ct / kg reduced . The reported slaughter figures for the whole of France are 367,670 (previous week 377,084 last week380,726) pieces on a high average level. The Dutch slaughtering companies in the 39.KW between -2 and -5 ct / kg less. In the 40th KW 2017. , , , , ct / kg can be paid.(Addendum follows) Belgium: Pig prices were reduced by -4 ct / kg in the 39th KW . The quotations of the slaughter companies are for the 40th KW 2017 ....... ct / kg. (Supplement follows) Germany : The slaughter numbers reach 1,030,988 (previous week 1.002.987 previous week 999.963) pieces. For the coming period from Thursday 28.09. until Wednesday 04.10. (39th / 40th KW-17) , the association price was reduced to € 1.53 per kg respectivelyIndex point again significantly reduced. The range ranges from 1.52 to 1.55 € / kg. The announced deliveries of the next week are included 241,500 (previous week 247,700 previous week 237,426) pieces considerably higher. Therefore slaughter numbers of well over the 1 million mark can be expected again and again. The fattening pigs' basic fare in Austria was valid for the 38th /KW is reduced by -4 ct / kg . For the 39th / KW should the base trip again by -4 ct / kg can be reduced.The pork prices in Spain were on Thurs, 21.09. by a further - 4.7 ct / kg. In (Upper) Italy are pig prices on 25.09.in Modena is -0.2 ct / kg , on Di in Reggio -0.3 ct / kg and Cremona -1 ct / kg lower. The slaughter numbers are 40.388 (previous week 39,498 last week39,498) still remain on a tight average. In Poland on 15.09.2017 pork prices at 57% MFL of 1.64 € / kg were quoted. Outlook: Increasing and foreseeable rising slaughter numbers in a majority of the EU Member States overload demand. For the coming months, an increasing supply of living space is expected. The 4.Quarter usually provides slaughter numbers that are significantly above the annual average. Demand remains subdued, and third-country business as well. International pork prices are at a low level. In the USA, the current pork prices are calculated at 0.90 € / kg. The US prices are on 26.09. in IOWA fell to 0,894 € / kg . Seasonally weakening (barbecue) demand, rising slaughter numbers and slaughter weights are on the march.The stock exchanges in Chicago for the later delivery dates in autumn indicate a persistently weak trend. The export business is only giving little relief. The fall / winter period in the US will fall back into critical price regions. China's pig pens have on 20.09.With 2,49 € / kg consolidated. In the coming months, sales are expected to rise without reaching the previous level again. EU exports to China / HK remain at a reduced level. The Russian pork prices on 27.09.2017 have fallen to converted 1.99 € / kg .The ruble has yielded again The current pork demand remains on similarly high Level as 3 years ago. African swine fever provides an export barrier of 2 to 3 years. Brazilian pork prices have risen on the basis of the average values in the southwest region on 18.09. strengthened to 1.34 € / kg.decreasing Domestic courses, a weak real and the cheap US competition are the decisive influencing factors.

ZMP Live Expert Opinion

Rising slaughter numbers and still high pre-registrations for a week with a missing battle day (3rd Oct in Germany) have again pocketed the pig pens. Demand remains cautious. In the surrounding areas of production there are falling courses. This also applies globally.