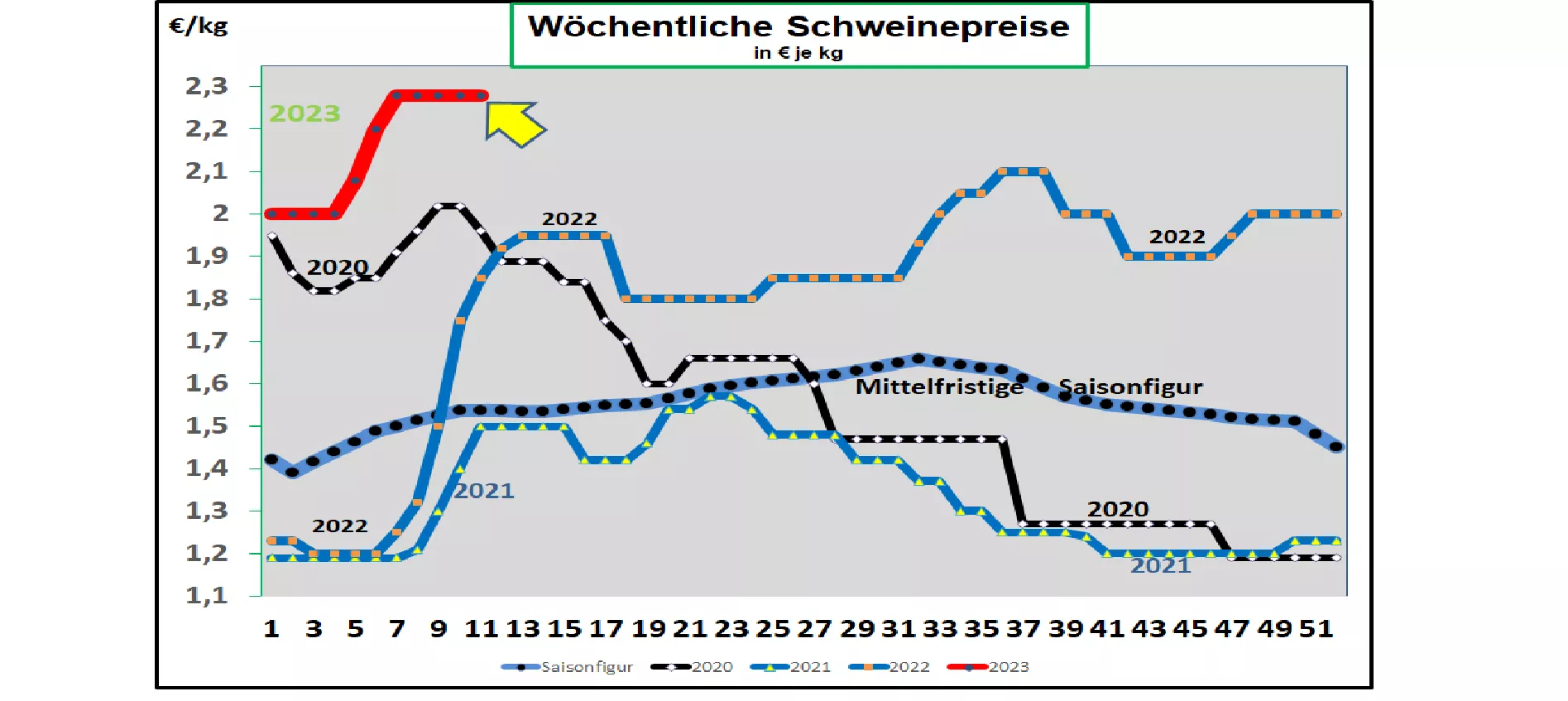

Germany: V price 2.28 €/kg (range 2.28 – 2.33 €/kg) - unchanged The weekly slaughter figures have fallen slightly again to 738,728 pigs ( previous week 746,679 ), but remain far below average values over several years; the slaughter weights have decreased somewhat to 97.2 kg . With 235,000 pigs (previous week 238,000 ), the pre-registrations remain well below the average of previous years. At the ISN auction on Tue, Mar 14In 2023, an average price of €2.38/kg (+2 cents/kg) was achieved in a range from €2.355 to €2.395/kg. The V price for the period from March 16, 2023 to March 22, 2023 remained at €2.28/kg; the range is from 2.28 to 2.33 €/kg. ASF : As of March 10, 2023, 5,152 wild boar infected with ASF have been officially confirmed in Brandenburg, Saxony and Mecklenburg. In the month of Febr.23 alone, 150 cases were reported. In the Neisse-Spree area, the infection pressure from the east and south of the area is increasing with the risk of further spread in the north. Market and price development in selected competitor countries: In Denmark , the prices in the 11th week of 2023 were again kept unchanged at a comparable calculated €1.80/kg . The high Danish export dependency to third countries limits the price scope.In Belgium, the prices in the 11th week of 2023 remained unchanged at €2.16/kg for the umpteenth time. Pigs are scarce, but meat sales remain limited. In the Netherlands , the prices in the 11th week of 2023 also remained at a comparable calculated €2.16/kg . In France/Brittany, prices have again been increased by the weekly maximum of +6 ct/kg to €2.371/kg . The slaughter figures are as low as 347,000 pigs. Slaughter weights have fallen slightly at 95.78 kg. In Italy, the listings in the 11th week of 2023 increased by a further 2 ct/kg . The supply remains too small for the demand. In Spain, the prices in the 11th week of 2023 were increased again by 5 ct/kg at a comparable €2.57/ kg. In addition to the (feed) cost pressure, high animal losses as a result of the PRRS epidemic ensure a scarce supply of live animals.Pigs are brought in from abroad. The Pig Association fears the introduction of ASF through the tall piglets. In the USA/IOWA, prices have remained at the equivalent of €1.62/kg . Battle numbers remain at reduced levels. However, the part prices support the listing level. For the front month Apr-2023, the futures prices on the stock exchange are €1.87/kg; for the summer months Brazil: The average producer prices have been reduced to 1.72 €/kg with REAL weakening again. The seasonal carnival effect is over. Nevertheless, the price level remains above average due to the cost-related reduced pig stock in the non-contractual farms. China: prices are beg. March 2023 slightly increased to the equivalent of €2.83/kg . The demand for meat is seasonally weak, as is usual. But the state conducts stock purchases to stabilize prices.On the Dalian Stock Exchange, May 2023 prices are already trading at the equivalent of €3.06/kg. For the July 2023 delivery, prices are back at €3.20/kg. The exchange rate has weakened. Conclusion: The persistently low slaughter numbers lead to a low meat supply. But the demand for meat is still so restrained that price increases can hardly be pushed through. Orientation towards a higher price level takes a certain amount of time to get used to. In any case, a fundamental price reduction is hardly justifiable. Livestock numbers across the EU tend to point to a further shortage of livestock.

ZMP Live Expert Opinion

The high pork price level that has been achieved is further supported by a low supply of live pigs. There is also a shortage in the southern EU countries and France, but this has led to rising prices. In the north of the EU, higher prices cannot be enforced due to the restrained sales situation. Higher supply quantities are not to be discerned in the foreseeable future due to the stock developments to date.