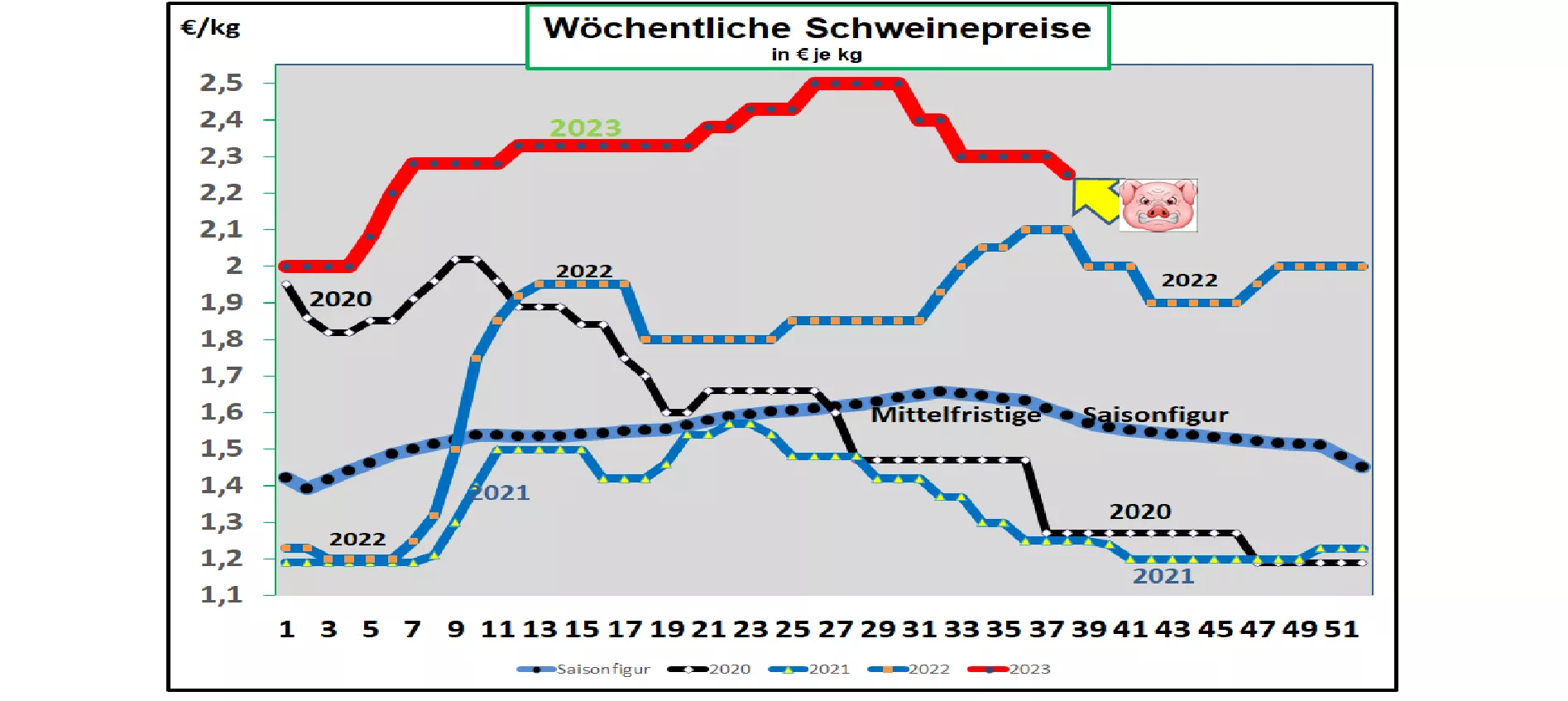

Germany: V- price 2.25 €/ kg (range 2.25 – 2.30 €/kg) The weekly slaughter numbers were higher again at 723,913 pigs ( previous week 717,612) , the slaughter weights only fell slightly at 97.2 kg . Pre-registrations remained at a comparatively high level at 267,300 pigs (previous week 267,900) . At the ISN auction on Tue. 19.09 2023 an average price of 2.33 €/kg . achieved in a range of 2.31 – 2.35 €/kg. The V price has been set at €2.25/kg in a range of €2.25 - €2.30/kg for the period from September 21, 2023 to September 27, 2023. ASF : As of September 8, 2023, 5,555 ASF-infected wild boars have been officially confirmed in Brandenburg, Saxony and Mecklenburg. In August 23 alone, 58 cases were confirmed in Brandenburg and Dresden. The first case has occurred in Sweden. Market and price development in selected competing countries: In Denmark , the comparable prices were reduced by -2 ct /kg to €1.89/kg in the 38th week of 2023. In Belgium the prices are in the 38th.Week 2023 remained unchanged with comparable calculated prices of €2.19/kg . In the Netherlands , prices will remain unchanged in the 38th week of 2023 at a comparable €2.17/kg . In France/Brittany prices are almost unchanged at €2.044/kg . Battle figures have fallen to 355,227; Slaughter weights are a reduced 95.13 kg. In Italy, the prices were increased slightly further by +1 ct/kg in the 38th week of 2023. Supply remains tight. The demand effect of the holiday season is still ongoing. In Spain, prices will be reduced by a further -3 ct/kg in the 38th week of 2023 to a comparable €2.43/ kg. Declining meat sales are forcing prices to be adjusted downwards. In the USA/IOWA, producer prices fell to 1.61 €/kg. The number of battles remains at a high level. The unit prices have recovered again. For Oct.-23 the stock market prices are at 1.71 €/kg. Brazil: Producer prices have increased again on average to €1.66/kg . Domestic demand has picked up somewhat again after the weak summer months. However, the live supply remains limited depending on the season. Export figures have picked up speed again. China: Prices have fallen again to €2.89/kg. Government stock purchases are suspended. Only for the consumption-intensive month of January 2024 is €2.96/kg expected again. However, the spring months of 2024 show weaker trends again. Conclusion: The number of battles stabilizes at over 420,000 per week. Pre-registrations also remain at an elevated level. The supply of meat continues to meet with subdued demand. The lower market range became the average value. A seasonally less tense supply situation in the upcoming autumn months with a slight increase in supply and weaker demand is becoming noticeable.

ZMP Live Expert Opinion

Given the subdued demand for meat, the only moderate increase in live supply in the form of increasing slaughter numbers and advance registrations was enough to push the average price down to the lower range of €2.25/kg. The upcoming season is usually characterized by increasing supply and at the same time restrained demand. That seems to be the case this year too.